Dubai's May 2026 market: 10,281 transactions worth AED 28.9B. Volumes cooling, prices sticky at AED 1,650/sqft. The full data, project leaderboards and what smart money is buying.

So, Dubai's real estate market in May 2026. It's officially entered what I'd call a period of healthy maturation. Or maybe just a much-needed recalibration. Breaking away from the crazy hyper-growth trends we've been used to, the month registered roughly 10,281 sales transactions. That's worth about AED 28.9 billion ($7.86 billion). Buyer behavior has definitely shifted toward end-user utility. Buyers actually have some negotiating leverage now, which is a nice change of pace.

I've been watching the market closely over the last few months. Honestly, it's fascinating to see how the landscape is shifting. The absolute frenzy we saw in 2023 and 2024? Yeah, that's settled down. Instead of speculators driving prices up overnight, we are seeing families. We're seeing long-term investors. And they are taking their time. They're negotiating harder, perhaps asking for better payment plans. Or they're just looking for properties that offer genuine lifestyle value, rather than just a quick flip. To be clear, this isn't a crash. Not even close. It feels more like a necessary deep breath after a very, very long sprint.

In this report, we're going to dive deep into the May 2026 data. This comes straight from the Dubai Land Department (DLD) and analyzed by DXB Interact. We'll explore the nuances of the primary and resale markets. We'll dissect the performance of the top areas. And, I think, we'll get a good look at the underlying trends shaping the future of Dubai property investment.

Overall Market Summary: Volume and Value Adjustments

The headline numbers for May 2026 definitely paint a picture of a market adjusting to new realities. We saw a total of 10,281 transactions across all property types. While this is still a pretty robust number globally, it does represent a 26.8% decrease month-on-month (MoM). And a 44.9% drop year-on-year (YoY).

Sales value followed a similar trajectory, totaling AED 28.9 billion. That's a 40.1% decline from the previous month, and a 56.7% decrease compared to May 2025. Interestingly, though, despite the drop in volume and overall value, the median price per square foot has remained remarkably resilient. It's standing at AED 1,650. This represents a slight 10% dip from April 2026, sure. But it is still up 3% year-on-year.

So, what does this actually mean for someone looking to buy property in Dubai right now? Well, I think it indicates that sellers of premium, well-located properties are holding firm on their pricing. They aren't panicking. The drop in overall sales value is likely driven by a decrease in the volume of those massive, ultra-high-net-worth transactions, rather than a widespread collapse in everyday property values. Buyers are absolutely still willing to pay a premium for quality. They are just far more selective about what that quality looks like.

May 2026 Key Performance Indicators

| Metric | May 2026 Value | MoM Change | YoY Change |

|---|---|---|---|

| Total Transactions | 10,281 | -26.8% | -44.9% |

| Total Sales Value | AED 28.9 Billion | -40.1% | -56.7% |

| Median Price / sqft | AED 1,650 | -10.0% | +3.0% |

Note: Data includes DLD direct sale transactions and DIFC sale transactions. Excludes mortgage registrations and gift transfers.

This article surfaces the market trends. The detailed Totality intelligence brief shows the specific projects smart money and institutional investors are positioning into right now — entry prices, payment structures, projected yields, and off-market access not visible on the DLD.

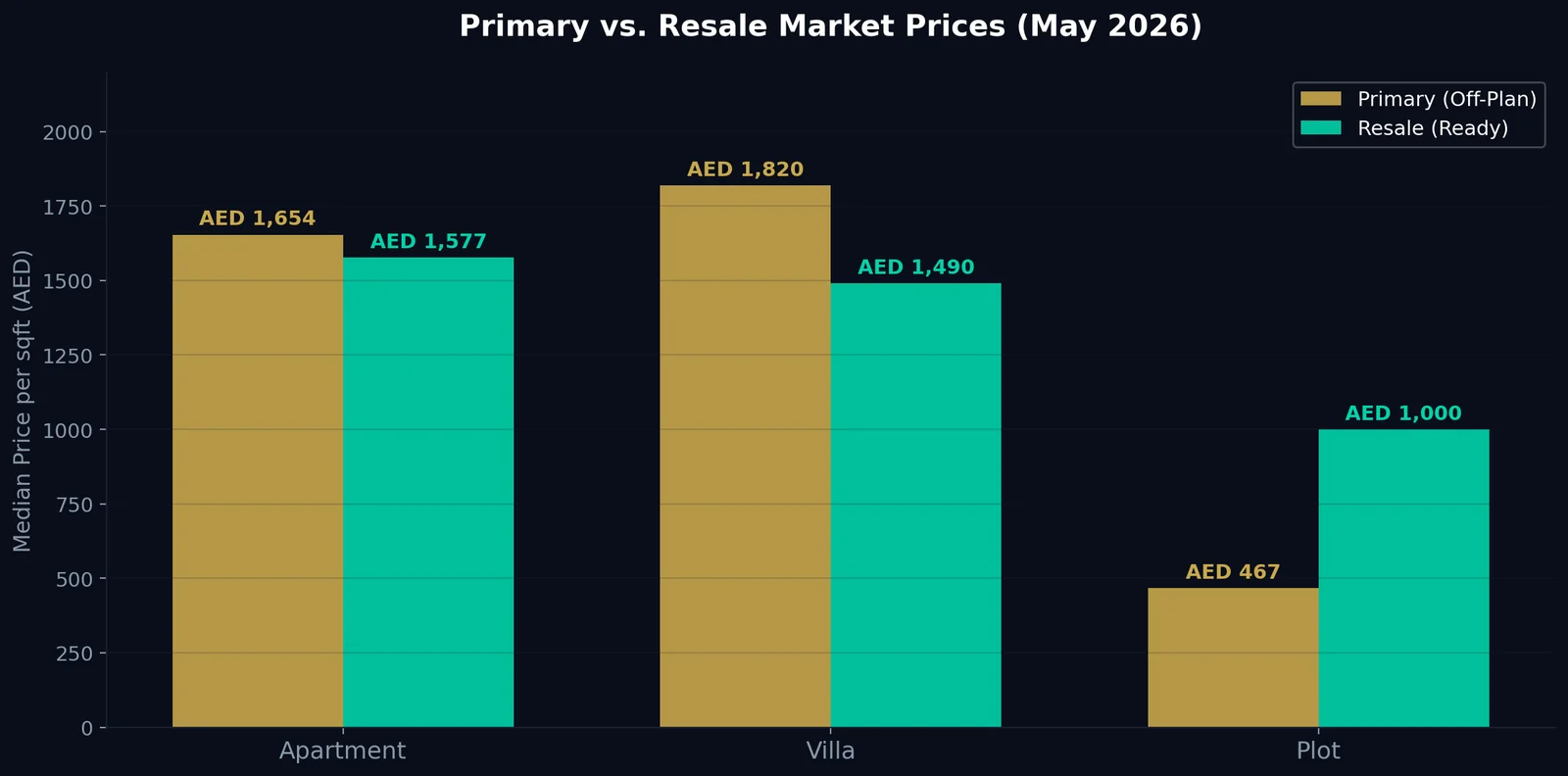

Primary Market Price Overview: Off-Plan Resilience

The primary market, which is basically off-plan properties sold directly by developers, continues to show mixed signals. Median prices per square foot for off-plan apartments stood at AED 1,654. That's an 8.8% decrease compared to 2025. Yet, if you zoom out, it remains a staggering 35.3% higher than the baseline set back in 2014.

Villas in the primary market? A completely different story. The median price per square foot for an off-plan villa hit AED 1,820. That represents a 21.1% increase from just last year. And an incredible 195% surge since 2014.

This divergence is really telling. The appetite for off-plan apartments might be cooling slightly, perhaps as buyers weigh the risks of future supply hitting the market. But the demand for spacious, newly built villas? Exceptionally strong. Families moving to Dubai are clearly prioritizing space. They want community amenities. Developers who can actually deliver high-quality villa projects on time are still commanding absolute premium prices. Sometimes I wonder if the apartment market will see a sharper correction soon. But then again, the continuous influx of new residents seems to provide a pretty solid floor for now.

Primary Market Median Prices

| Property Type | Median Price/sqft (AED) | Change vs. 2025 | Change vs. 2014 |

|---|---|---|---|

| Apartment | 1,654 | -8.8% | +35.3% |

| Villa | 1,820 | +21.1% | +195.0% |

| Plot | 467 | +1.1% | +63.1% |

Resale Market Price Overview: The Ready Property Advantage

Turning our attention to the resale, or secondary, market, we see a slightly different dynamic playing out. The median price per square foot for ready apartments is AED 1,577. That's a 3.6% increase from 2025, and 31.9% higher than in 2014.

Ready villas, however, saw a marginal dip. Nothing crazy, but the median price per square foot settled at AED 1,490. That's a tiny 0.5% decrease from 2025. Though, to be fair, it's still 106.5% higher than a decade ago. Plots in the resale market? They saw a massive 75.4% jump from 2025, reaching AED 1,000 per square foot.

The strength in ready apartment prices strongly suggests that end-users are driving this segment. People moving to Dubai for work want a place to live, and they want it immediately. They don't want to wait two or three years for an off-plan project to complete. Especially with rental yields remaining relatively high. This immediate utility is giving sellers in the secondary apartment market a very distinct advantage. On the flip side, the slight softening in ready villa prices might indicate that some sellers are finally willing to negotiate to close a deal. Especially if their property is a bit older and requires renovation.

Resale Market Median Prices

| Property Type | Median Price/sqft (AED) | Change vs. 2025 | Change vs. 2014 |

|---|---|---|---|

| Apartment | 1,577 | +3.6% | +31.9% |

| Villa | 1,490 | -0.5% | +106.5% |

| Plot | 1,000 | +75.4% | +141.5% |

As we move deeper into 2026, the contrast between the primary and resale markets will be crucial to monitor. The off-plan sector is heavily reliant on investor sentiment and developer reputation. The secondary market, on the other hand, is more closely tied to immediate demographic shifts. People actually moving here. People needing homes right now.

Rental Market Dynamics: Stability Amidst Growth

While sales volumes have definitely seen a contraction, the rental market tells a slightly different story. Honestly, it's an area I get asked about almost daily. Tenants are desperately looking for some relief. Meanwhile, landlords are trying to maximize yields before any potential market softening actually hits.

In May 2026, the average annual rent for an apartment held perfectly steady at AED 70,000. That's a 0% change compared to April 2026. This stability is a very welcome sign for tenants who have faced relentless increases over the past few years. Villa rentals, however, showed a slight contraction. They dropped 5.4% month-on-month to an average of AED 175,000 annually.

The most shocking figure, though? That would be in the commercial sector. Commercial rents absolutely skyrocketed by an astonishing 272.5% compared to April, reaching an average of AED 74,500. This massive jump suggests a sudden influx of new businesses setting up shop. Or, perhaps, a few very large, high-value commercial leases just skewed the monthly average. Either way, it's a clear indicator that Dubai's appeal as a global business hub remains untarnished, even if the residential sales market is taking a bit of a breather.

Dubai Rental Prices (Annual)

| Property Type | Average Annual Rent | Change vs. April 2026 |

|---|---|---|

| Apartment | AED 70,000 | 0.0% |

| Villa | AED 175,000 | -5.4% |

| Commercial | AED 74,500 | +272.5% |

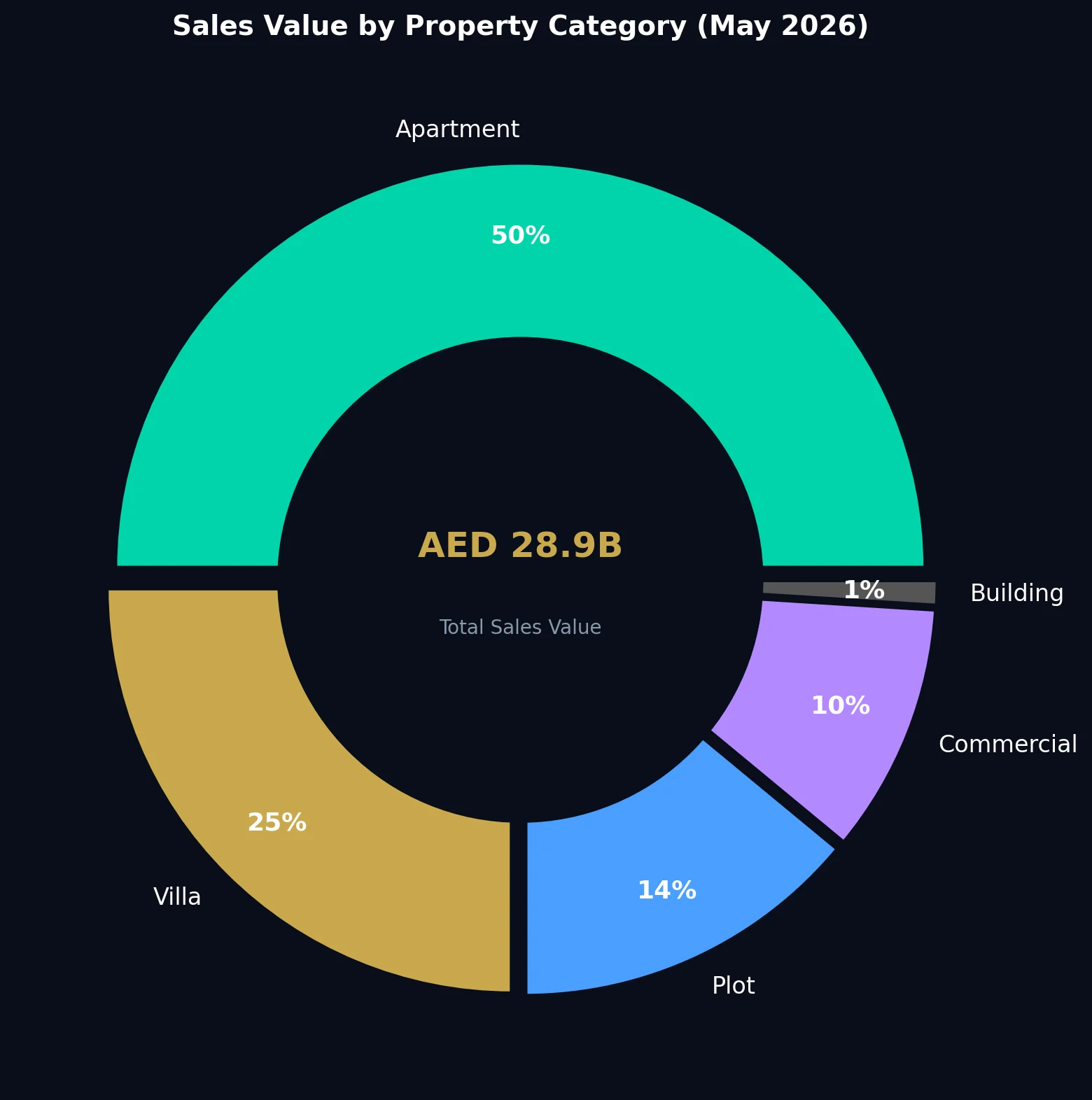

Where is the Money Going? Sales Value by Category

When we break down the AED 28.9 billion in sales value, the dominance of the apartment sector is pretty clear. Exactly half, 50%, of all money spent on Dubai real estate in May 2026 went straight into apartments.

Villas captured 25% of the total sales value. That is actually impressive given their lower transaction volume, and it really highlights their higher individual price points. Plots accounted for 14%, and commercial properties made up the remaining 10%.

This breakdown makes a lot of sense. Apartments are the lifeblood of Dubai's property market. They appeal to young professionals, small families, and investors looking for liquid assets with strong rental yields. The 14% share for plots is also noteworthy, I think. It shows that developers, and wealthy individuals, are still actively acquiring land for future custom builds. They are betting on the long-term trajectory of the city, and putting their money where their mouth is.

Top 5 Performing Areas: The Shift Southward

If you want to know where the real action is right now, you have to look at the transaction volumes by area. The "Top 5" list for May 2026 reveals a really fascinating trend. It's the continued rise of Dubai South and its surrounding communities.

1 | Dubai South |

2 | Wadi Al Safa 3 |

3 | Wadi Al Safa 5 |

4 | Al Barsha South Fourth |

5 | Jabal Ali First |

Notice what's missing here? The usual suspects. Places like Dubai Marina, Downtown Dubai, or Palm Jumeirah aren't leading the volume charts anymore. Instead, buyers are flocking to Dubai South and the Wadi Al Safa corridors. Why? It comes down to affordability and future infrastructure. With the ongoing expansion of Al Maktoum International Airport, and the broader development of the southern corridor, buyers are clearly positioning themselves ahead of the curve. I honestly believe that in five years, we'll look back at today's prices in Dubai South and realize what an absolute bargain they were.

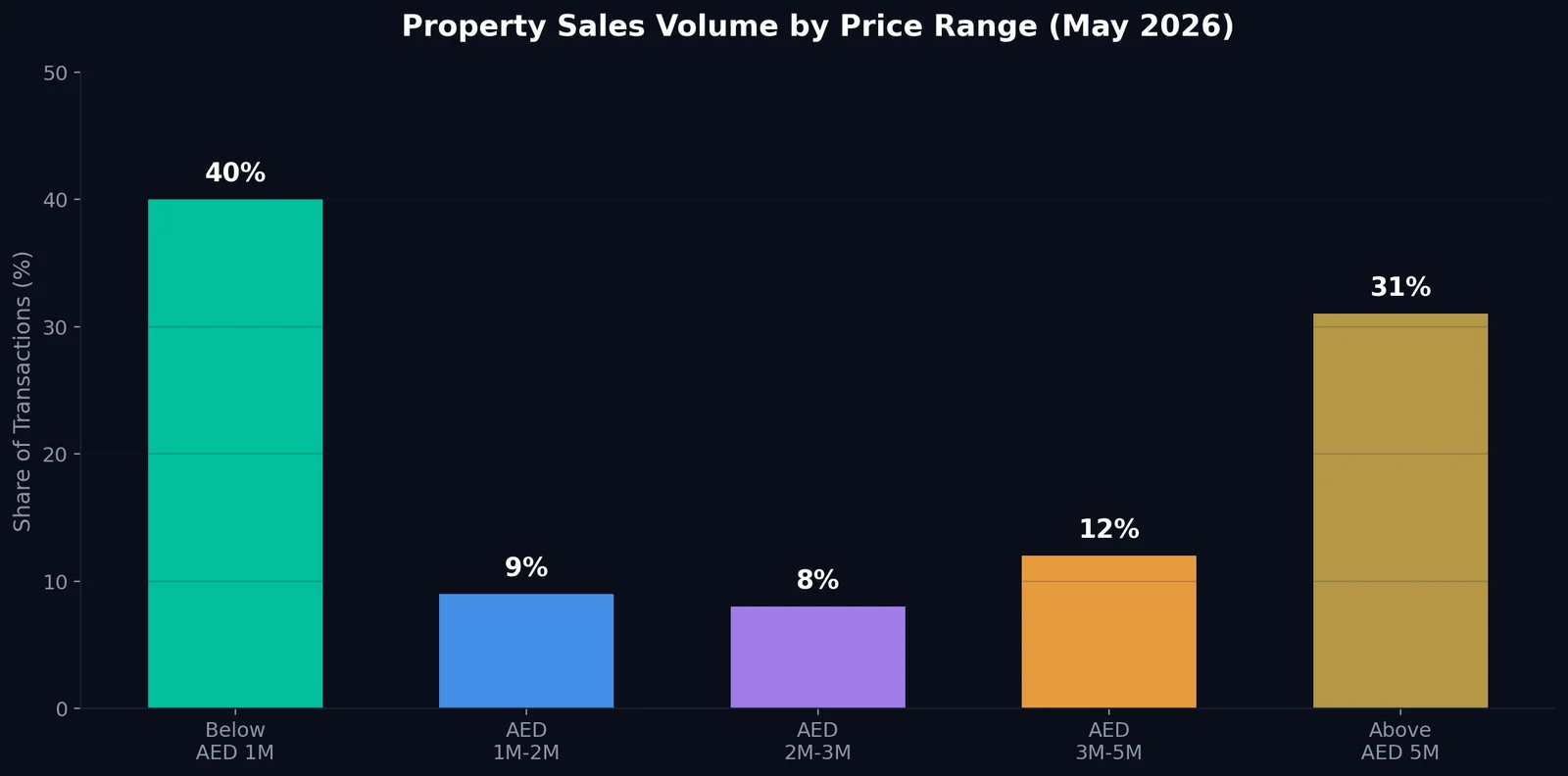

Property Sales Volume by Price Range: The Missing Middle?

Another critical metric is how much people are actually spending per transaction. The data shows a market that is heavily weighted toward the affordable and luxury ends. It leaves us with a somewhat hollowed-out middle.

A massive 40% of all transactions in May 2026 were for properties priced below AED 1 million. This is your entry-level investor and first-time buyer segment. They are primarily targeting studios and 1-bedroom apartments in emerging areas.

On the other end of the spectrum, 31% of transactions were for properties priced at more than AED 5 million. This really highlights the enduring appeal of Dubai's luxury sector. High-net-worth individuals are still parking significant capital in premium villas and branded residences.

The middle tiers, from AED 1M to 5M, accounted for only 29% of the market combined. That's 9% for AED 1M-2M, 8% for AED 2M-3M, and 12% for AED 3M-5M. This polarization is definitely something to watch. It suggests that while Dubai remains attractive to the ultra-wealthy and entry-level buyers, the traditional "middle-class" upgrade market might be feeling the pinch of recent price appreciations. They are getting squeezed out.

Transaction Share by Price Range

| Price Range | Share of Transactions | ||

|---|---|---|---|

| Below AED 1 Million |

| ||

| AED 1M - 2M |

| ||

| AED 2M - 3M |

| ||

| AED 3M - 5M |

| ||

| More than AED 5 Million |

|

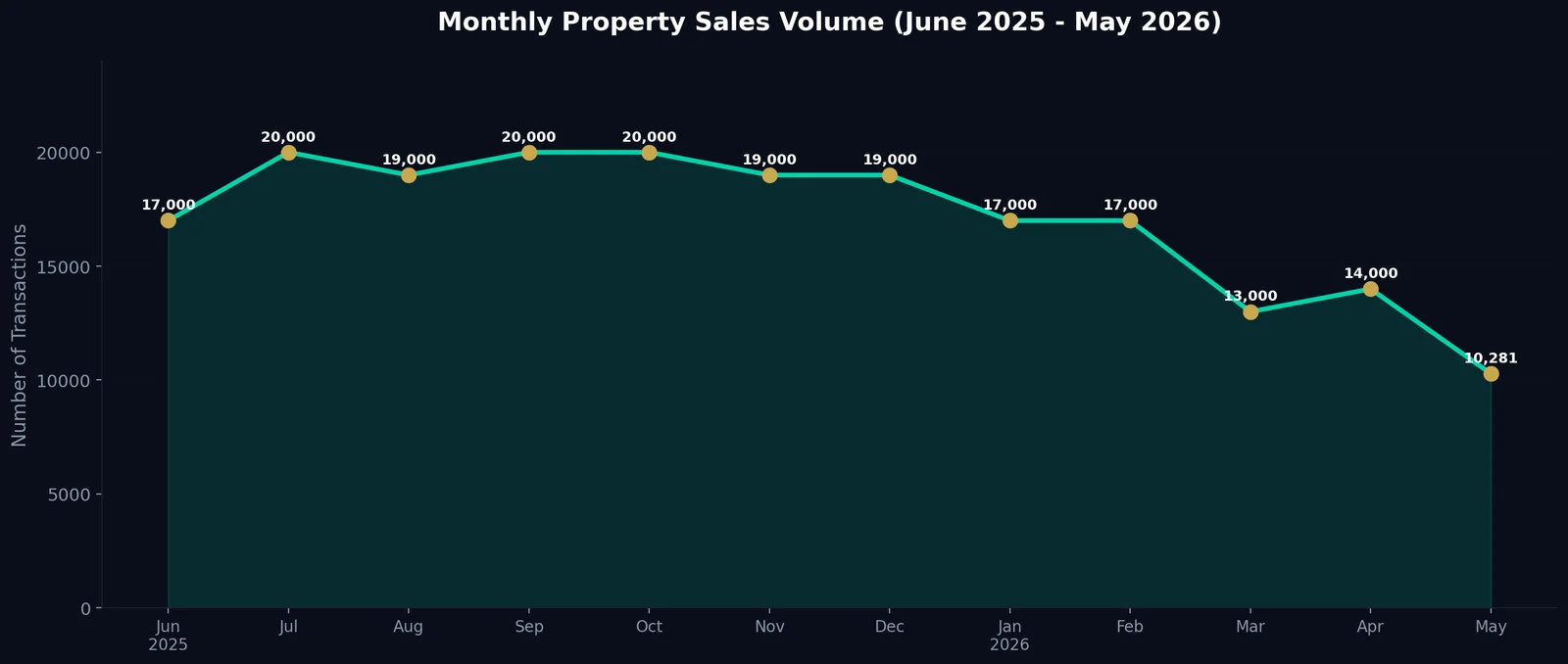

Monthly Property Sales Volume: Tracking the Trend

To understand the 10,281 transactions in May 2026, you really need context. Look at the preceding 12 months. The market had been running incredibly hot. I mean, consistently hovering around 19,000 to 20,000 transactions per month throughout the second half of 2025. That's a lot of deals closing.

Then, starting in early 2026, we began to see a taper. March dropped to 13,000. April saw a slight bump back to 14,000. And now May has settled at just over 10,000. That's quite a slide if you're just looking at the raw numbers.

Monthly Sales Volume · June 2025 to May 2026

| Month | Sales Volume |

|---|---|

| June 2025 | 17,000 |

| July 2025 | 20,000 |

| August 2025 | 19,000 |

| September 2025 | 20,000 |

| October 2025 | 20,000 |

| November 2025 | 19,000 |

| December 2025 | 19,000 |

| January 2026 | 17,000 |

| February 2026 | 17,000 |

| March 2026 | 13,000 |

| April 2026 | 14,000 |

| May 2026 | 10,281 |

Is this cause for panic? I don't think so. Look, the market simply couldn't sustain 20,000 transactions a month indefinitely. That pace was never going to last. What we're seeing now is a normalization phase. The current volume represents a healthier, more sustainable pace. It's driven more by genuine end-users than speculative flipping. Which, frankly, is what we want to see.

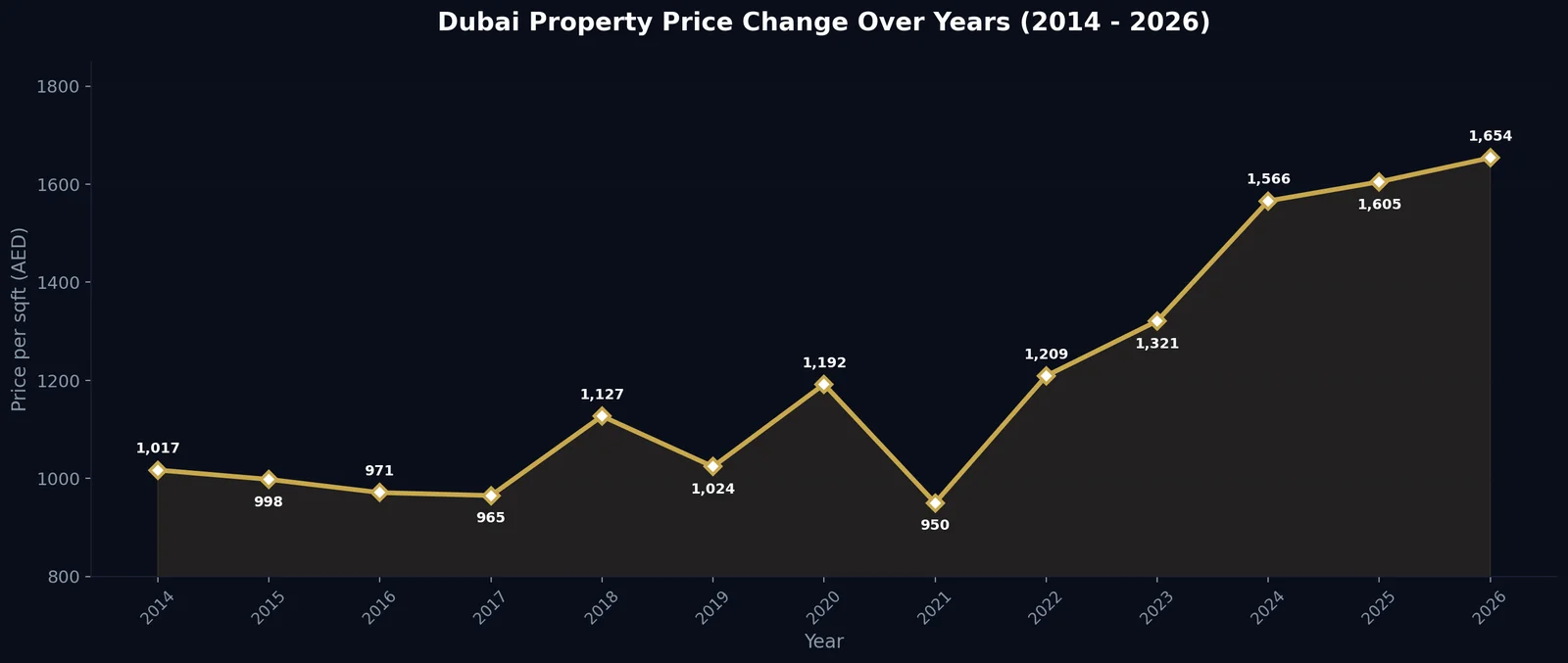

Historical Context: The Long-Term Trajectory of Dubai Property Prices

To truly understand where we are in May 2026, we really have to zoom out. I often tell clients that real estate is not a day-trading sport. It's about the long game. When we look at the historical price per square foot across all areas since 2014, the narrative of Dubai's maturation becomes pretty undeniable.

Back in 2014, the average price per square foot was AED 1,017. We saw a slow, agonizing slide down to a low of AED 950 in 2021, right during the pandemic recovery phase. Then, the boom began. 2022 hit AED 1,209. 2023 jumped to AED 1,321. And by 2024, we were at AED 1,566.

Today, in May 2026, we sit at AED 1,654. Yes, the transaction volume has dipped recently. But the capital appreciation locked in over the last five years is monumental. This isn't the fragile, highly leveraged market of 2008. Not at all. The regulatory environment, driven by RERA and the DLD, has forced a level of transparency and financial discipline that simply didn't exist before. The steady climb in the median price, even as volumes cool down, proves that the intrinsic value of Dubai real estate has permanently shifted upward.

Dubai Property Price Change (2014 - 2026)

| Year | Price per sqft (AED) |

|---|---|

| 2014 | 1,017 |

| 2015 | 998 |

| 2016 | 971 |

| 2017 | 965 |

| 2018 | 1,127 |

| 2019 | 1,024 |

| 2020 | 1,192 |

| 2021 | 950 |

| 2022 | 1,209 |

| 2023 | 1,321 |

| 2024 | 1,566 |

| 2025 | 1,605 |

| 2026 (May) | 1,654 |

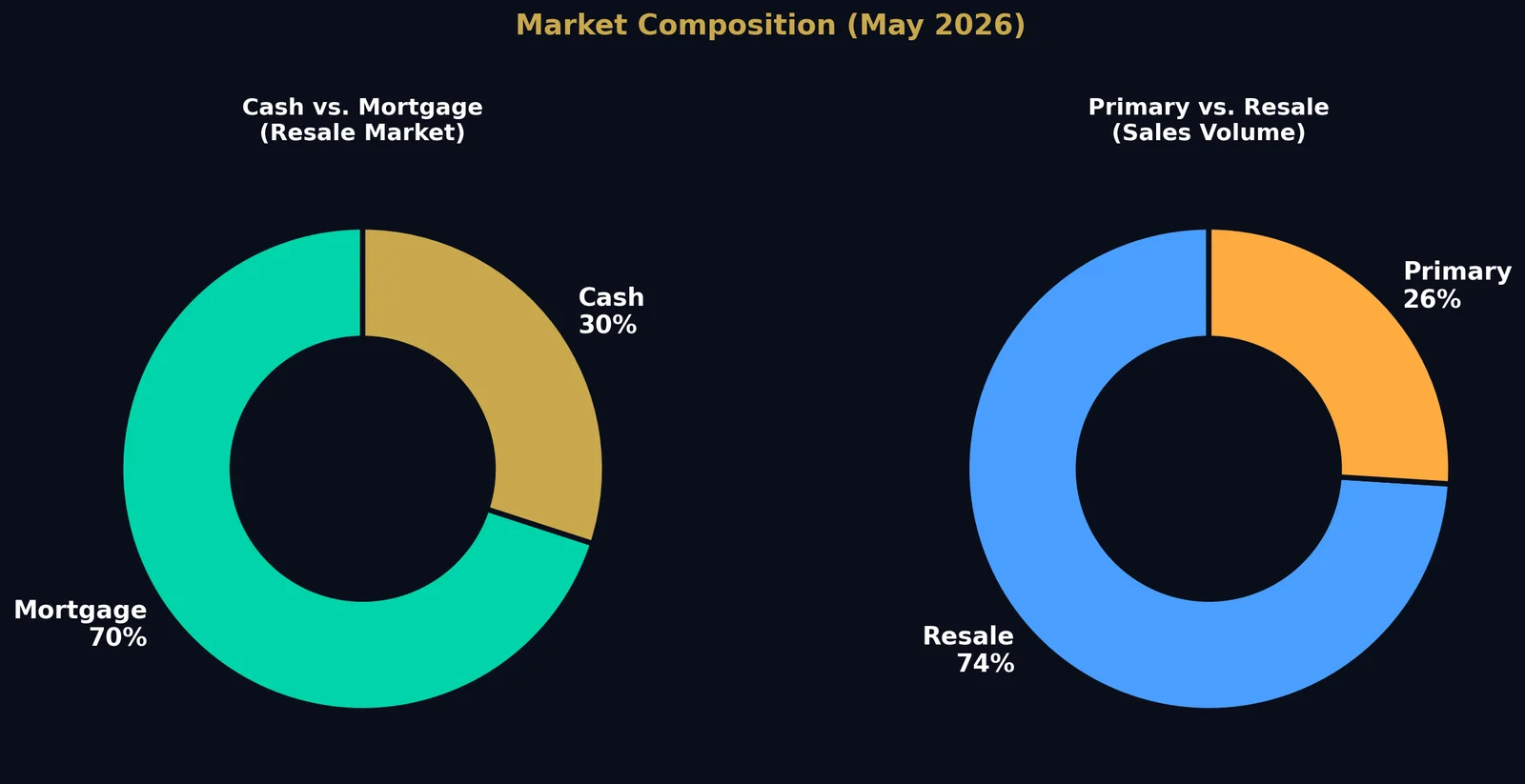

The Battle of the Markets: Primary vs. Resale

One of the most revealing metrics from May 2026 is the split between the primary (off-plan) and resale (secondary) markets. Right now, the resale market is absolutely dominating the volume. It accounts for 74% of all transactions. The primary market only captured 26%.

However, when you look at the total sales value, the gap narrows quite a bit. The resale market accounts for 64% of the value, while the primary market takes 36%.

So, what does this tell us? It means that while far fewer off-plan properties are being sold compared to ready properties, the off-plan properties that are selling are commanding significantly higher price points. Buyers in the primary market are likely targeting premium, ultra-luxury branded residences. Or massive waterfront villas that simply don't exist in the secondary market yet. Meanwhile, the bulk of everyday transactions, families buying their first home, or investors looking for immediate rental income, is happening in the resale space. I've noticed my own clients leaning heavily toward ready properties lately. The appeal of walking into a physical space, inspecting the finish, and getting the keys in 30 days is very strong right now. People want certainty.

Mortgage Market Deep Dive: The Shift to Financing

There's this persistent myth out there that Dubai is a purely cash-driven market. While cash certainly plays a massive role, especially at the ultra-luxury tier, the mortgage market is actually very robust and growing.

In May 2026, the total mortgage value reached AED 17.5 billion. That is a massive 21.3% increase month-on-month. And a 16.8% increase year-on-year. However, the number of mortgage transactions actually dropped to 2,573. That's down 36.9% MoM and 44.9% YoY.

Fewer mortgages, but a much higher total value. This means the average loan size has absolutely skyrocketed. People are borrowing more money to buy more expensive properties.

When we look at the overall payment split in the resale market, 70% of transactions were financed via mortgage, while 30% were cash. This 70/30 split is a hallmark of a mature, end-user-driven market. When speculators dominate, cash is king. When families and long-term residents dominate, mortgages take over. Honestly, it's a very healthy sign for the long-term stability of the city.

Cash vs. Mortgage Split (Resale Market)

| Payment Type | Share of Transactions | ||

|---|---|---|---|

| Mortgage |

| ||

| Cash |

|

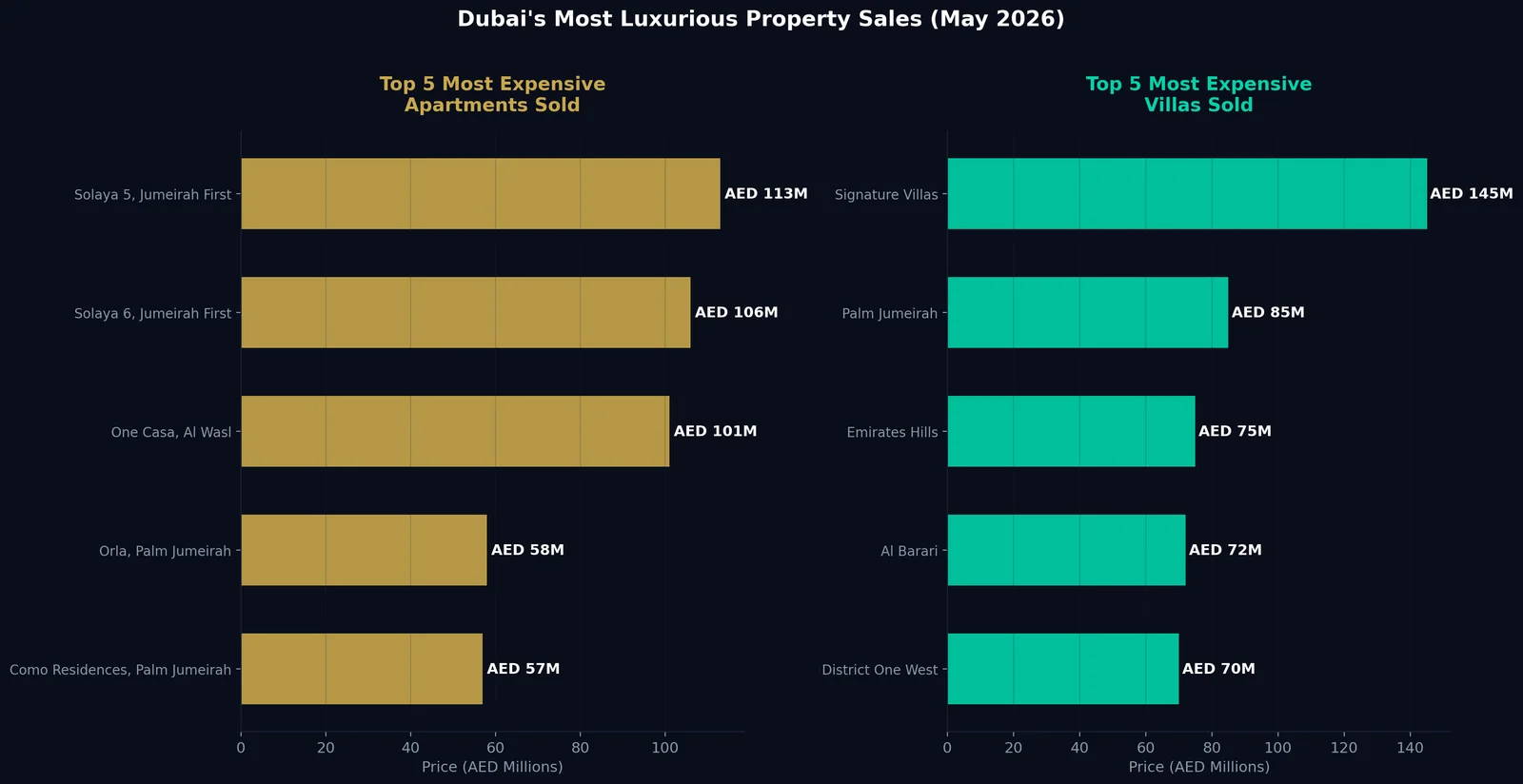

Dubai's Most Luxurious Property Sales: The Sky is the Limit

No Dubai real estate report is complete without looking at the absolute top tier of the market. And honestly, the city continues to attract the global elite in ways that still surprise me. The numbers from May 2026 are nothing short of breathtaking.

Top 5 Most Expensive Apartments Sold

The branded residence sector continues to push boundaries. Solaya at Jumeirah First absolutely dominated the apartment charts this month.

| Rank | Price (AED) | Project / Area |

|---|---|---|

| 1 | 113 Million | Solaya 5 at Jumeirah First |

| 2 | 106 Million | Solaya 6 at Jumeirah First |

| 3 | 101 Million | One Casa at Al Wasl |

| 4 | 58 Million | Orla By Omniyat at Palm Jumeirah |

| 5 | 57 Million | Como Residences at Palm Jumeirah |

I still find it incredible that an apartment can sell for AED 113 million. But when you look at the level of service, the architecture, and the sheer exclusivity of projects like Solaya or Orla, you realize you aren't just buying square footage. You are buying a piece of functional art.

Top 5 Most Expensive Villas Sold

The villa market saw even higher numbers. A Signature Villa took the top spot at a staggering AED 145 million. Let that sink in for a moment.

| Rank | Price (AED) | Project / Area |

|---|---|---|

| 1 | 145 Million | Signature Villas |

| 2 | 85 Million | Palm Jumeirah |

| 3 | 75 Million | Emirates Hills |

| 4 | 72 Million | Al Barari |

| 5 | 70 Million | District One West |

Notice the locations here. Palm Jumeirah and Emirates Hills remain the undisputed kings of Dubai luxury. No surprise there. But what's interesting is seeing Al Barari and District One West pulling in AED 70 million+ sales. That tells me the definition of prime real estate in Dubai is expanding. Buyers are willing to pay ultra-premium prices for inland communities now, as long as the lifestyle offering is unique enough. That wasn't always the case.

Most AED 70M+ transactions in Dubai never reach a public portal. The Totality advisory desk is connected directly to the inventory, the relationships, and the structures behind these closings — including current off-market opportunities in Solaya, Orla, Signature Villas, Emirates Hills and other prime communities.

Best Selling Projects: A Tale of Two Markets (and Four Leaderboards)

Alright, this is the part I find most interesting every month. Forget the averages and the medians for a second. Which actual projects are people buying into? Where is the real money flowing? The answer tells you more about buyer psychology than any price index ever could.

The Off-Plan Apartment Race: Binghatti's Dominance

Let me just put this out there. Binghatti Skyflame 1 recorded 442 transactions in a single month. Four hundred and forty-two. That is an extraordinary number for one building. AED 311.1 million in total value, with a median price of just AED 550,000. This is the sweet spot. The exact price point where a first-time investor from India, Pakistan, or the UK can get their foot in the door. Binghatti clearly understands this audience better than almost anyone else right now.

Skyflame 2 followed with 193 transactions at a nearly identical median of AED 565,000. Then Azizi Venice 14 (both Building F and Building A) pulled in 109 and 105 transactions respectively, at a slightly higher AED 650,000 median. And then there's Bond, which is interesting because its median price is just AED 201,000. That's micro-unit territory. 101 transactions at that price point tells you there's genuine demand for ultra-compact, ultra-affordable Dubai exposure.

| Project | Transactions | Total Value (AED) | Median Unit Price |

|---|---|---|---|

| Binghatti Skyflame 1 | 442 | 311.1M | AED 550K |

| Binghatti Skyflame 2 | 193 | 124.8M | AED 565K |

| Azizi Venice 14, Building F | 109 | 82.5M | AED 650K |

| Azizi Venice 14, Building A | 105 | 79.1M | AED 650K |

| Bond | 101 | 23.9M | AED 201K |

The Off-Plan Villa Race: Volume vs. Value (A Stark Contrast)

This is where it gets really interesting. Dubai Investment Park First led in sheer volume with 97 transactions. Makes sense. The median price there is AED 1.3 million, which is accessible for a villa. Lunaya came in second with 62 transactions and a much higher median of AED 6.9 million.

But here's the number that stopped me in my tracks. Palm Jebel Ali. Only 22 transactions. Twenty-two. And yet those 22 sales generated AED 815.7 million in total value. The median price per unit? AED 31.3 million. That's more total value than the top three projects combined, from a fraction of the transactions. If that doesn't tell you everything about the scarcity premium on waterfront land in Dubai, I don't know what does.

| Project | Transactions | Total Value (AED) | Median Unit Price |

|---|---|---|---|

| Dubai Investment Park First | 97 | 146.2M | AED 1.3M |

| Lunaya | 62 | 524.6M | AED 6.9M |

| Reportage Hills | 47 | 95.1M | AED 1.8M |

| Palm Jebel Ali | 22 | 815.7M | AED 31.3M |

| Wadi Al Safa 3 | 22 | 308.3M | AED 13.6M |

Ready Apartments: The End-User Picks

The resale apartment market is a completely different animal. No single project dominates. It's fragmented, spread out, and that actually makes sense. Because end-users don't all want the same thing. They're choosing based on commute, school proximity, lifestyle preference. It's personal.

Peninsula Four and District One Residences 26 tied at 31 transactions each. Sobha Hartland's Crest Grande is interesting here, pulling AED 62.9 million from just 22 sales, which gives it the highest median price in this category at AED 3 million. That's a premium ready product finding its buyer. Meanwhile, Ciel and Damac Maison Aykon City are serving the more price-conscious end-user at AED 756K and AED 720K medians respectively.

| Project | Transactions | Total Value (AED) | Median Unit Price |

|---|---|---|---|

| Peninsula Four | 31 | 59.1M | AED 1.9M |

| District One Residences 26 | 31 | 52.1M | AED 1.4M |

| Ciel | 24 | 21.7M | AED 756.5K |

| Sobha Hartland, Crest Grande | 22 | 62.9M | AED 3M |

| Damac Maison Aykon City | 21 | 19.1M | AED 720.4K |

Ready Villas: Scarcity in Action

Ready villas are always low-volume. Always. Nine transactions topped the chart for The Valley (Orania). Nine. That's the nature of this segment. People who own premium villas don't sell them casually. When they do, it's a considered decision.

What's notable here is the Damac Lagoons effect. Three separate Damac Lagoons clusters made the top five: Costa Brava 1, Nice 1, and Portofino. All hovering around AED 2.3M to 2.8M median prices. This tells me there's a very specific buyer profile being served here. Families who want the lagoon lifestyle, the European-themed aesthetic, and a price point that feels luxurious without being obscene. It's working.

| Project | Transactions | Total Value (AED) | Median Unit Price |

|---|---|---|---|

| The Valley, Orania | 9 | 25.9M | AED 2.7M |

| Damac Lagoons, Costa Brava 1 | 7 | 19.9M | AED 2.8M |

| Rukan 3 | 7 | 9M | AED 975K |

| Damac Lagoons, Nice 1 | 7 | 20.5M | AED 2.3M |

| Damac Lagoons, Portofino | 6 | 17.3M | AED 2.7M |

We track every project in this report at the unit level — current pricing, available payment plans, developer terms, projected yields, and resale velocity. Book a no-obligation 30-minute strategy call to review which opportunities match your capital, timeline, and risk profile.

Area Price Guide: Know Before You Buy

If you are actively looking to purchase right now, understanding the granular price differences by bedroom count across key areas is pretty vital. According to the May 2026 data, these are the eight zones I'd be closely monitoring for apartment sale prices:

1 | Business Bay The commercial heart of the city. Excellent for studio and 1-bed rental yields. |

2 | Downtown Dubai Premium pricing here, obviously. Driven by Burj Khalifa proximity and the whole "I live in Downtown" factor. |

3 | Dubai Marina The perennial favorite for expats. Strong secondary market activity. |

4 | Dubai Islands The rising star for waterfront luxury. Still relatively new, which means there's upside. |

5 | Palm Jumeirah The gold standard. Entry prices are steep, but so is the prestige. |

6 | Dubai Creek Harbour Emaar's masterpiece. Attracting families who want a quieter waterfront without the Palm price tag. |

7 | Dubai South The volume leader right now. Best for long-term capital appreciation if you're patient. |

8 | Jumeirah Village Circle (JVC) The undisputed king of middle-market affordability. Everyone starts here. |

For specific, up-to-the-minute pricing on studios through 4-bedroom apartments in these areas, I highly recommend checking the live feeds on DXB Interact.

Conclusion: A Market Catching Its Breath

So, what is the final verdict on the Dubai real estate market in May 2026?

If you just read the mainstream financial press, you might see headlines screaming about "plunging volumes" or "market corrections." But when you look at the actual data, the story is much more nuanced. Yes, transaction volumes are definitely down from the dizzying heights of late 2025. But prices? They have remained incredibly sticky.

What we are witnessing is a transition. From a speculative, hyper-growth phase into something more mature. More end-user-driven. Mortgages are replacing cash in the secondary market. Buyers are prioritizing ready properties over off-plan promises, unless the developer has a genuinely flawless track record. The luxury segment remains practically untouchable, as it always does. And emerging areas like Dubai South are absorbing the demand for affordable entry points.

For investors, the strategy simply must evolve. I can't stress this enough. The days of buying just any off-plan unit and flipping it for a 30% premium before handover? Those are largely behind us. Today, success in Dubai real estate requires careful area selection. A focus on rental yields. And a long-term holding mindset. The fundamentals of Dubai, its safety, tax environment, infrastructure, remain as strong as ever. The market isn't crashing. It's just growing up. And perhaps that's the best thing that could happen to it.

If you are considering entering the market, or if you need to re-evaluate your current portfolio in light of these new trends, reach out to us at Totality Real Estate. We navigate these numbers every single day. We'd be more than happy to help you find the right opportunity.