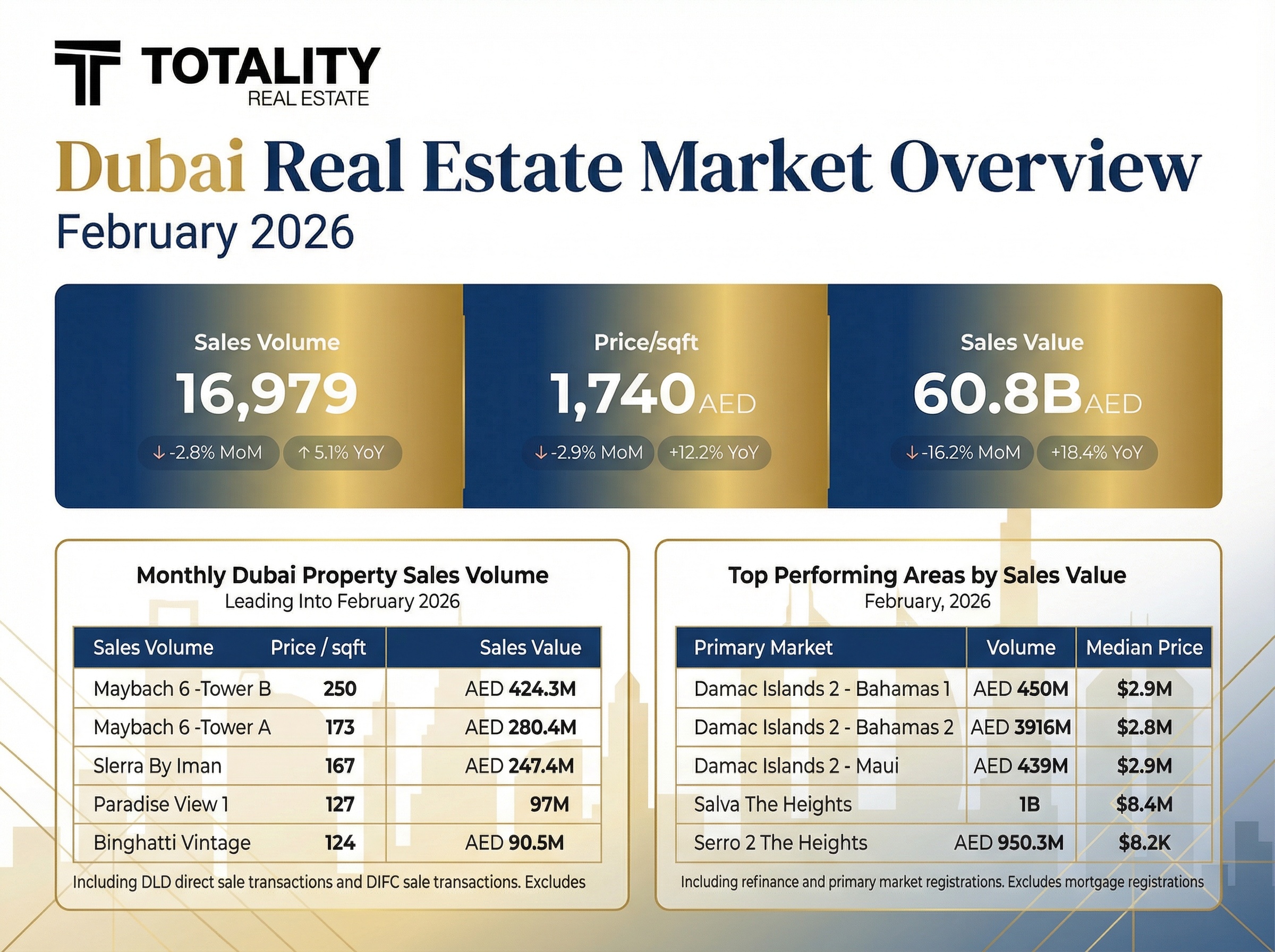

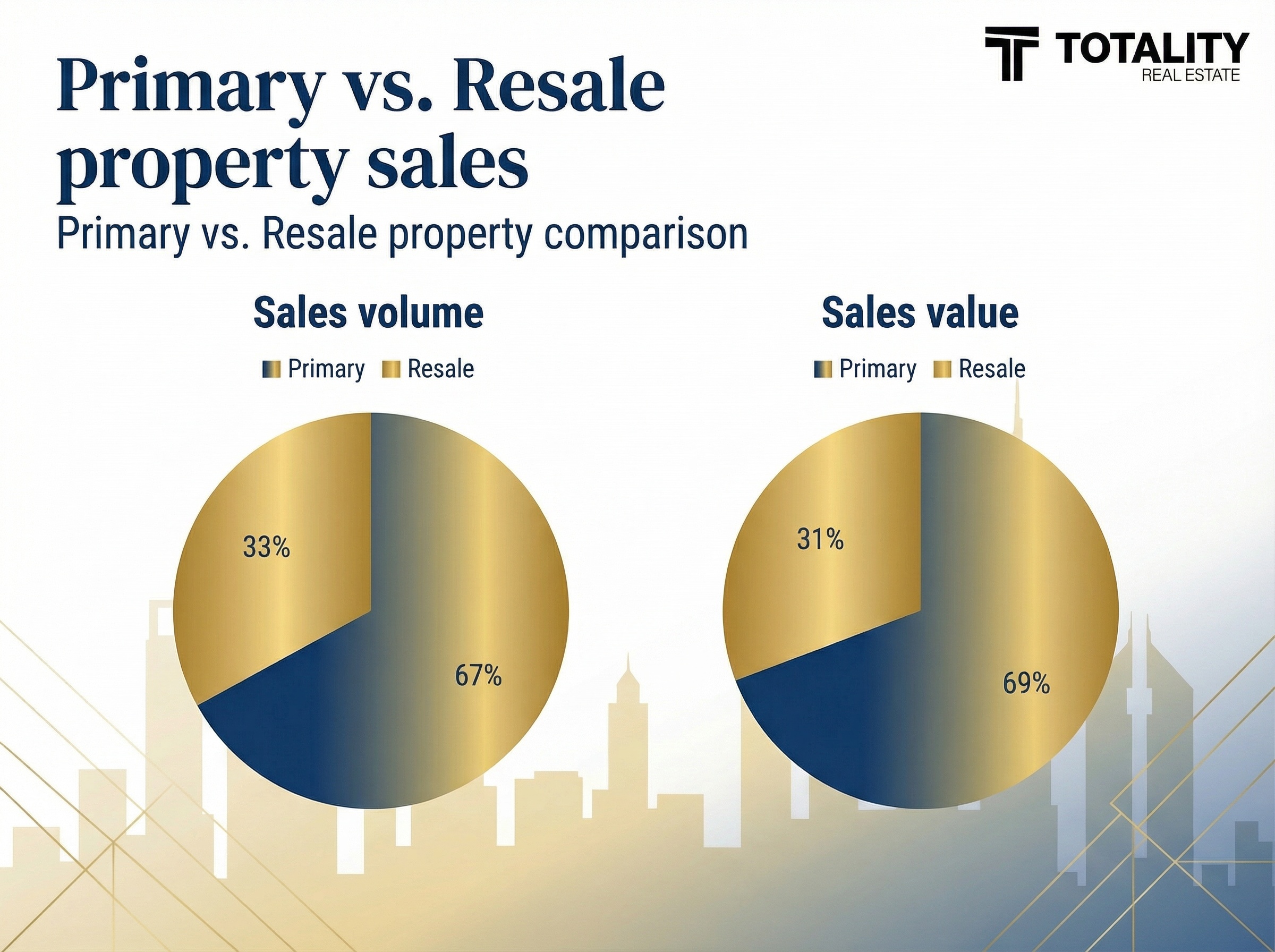

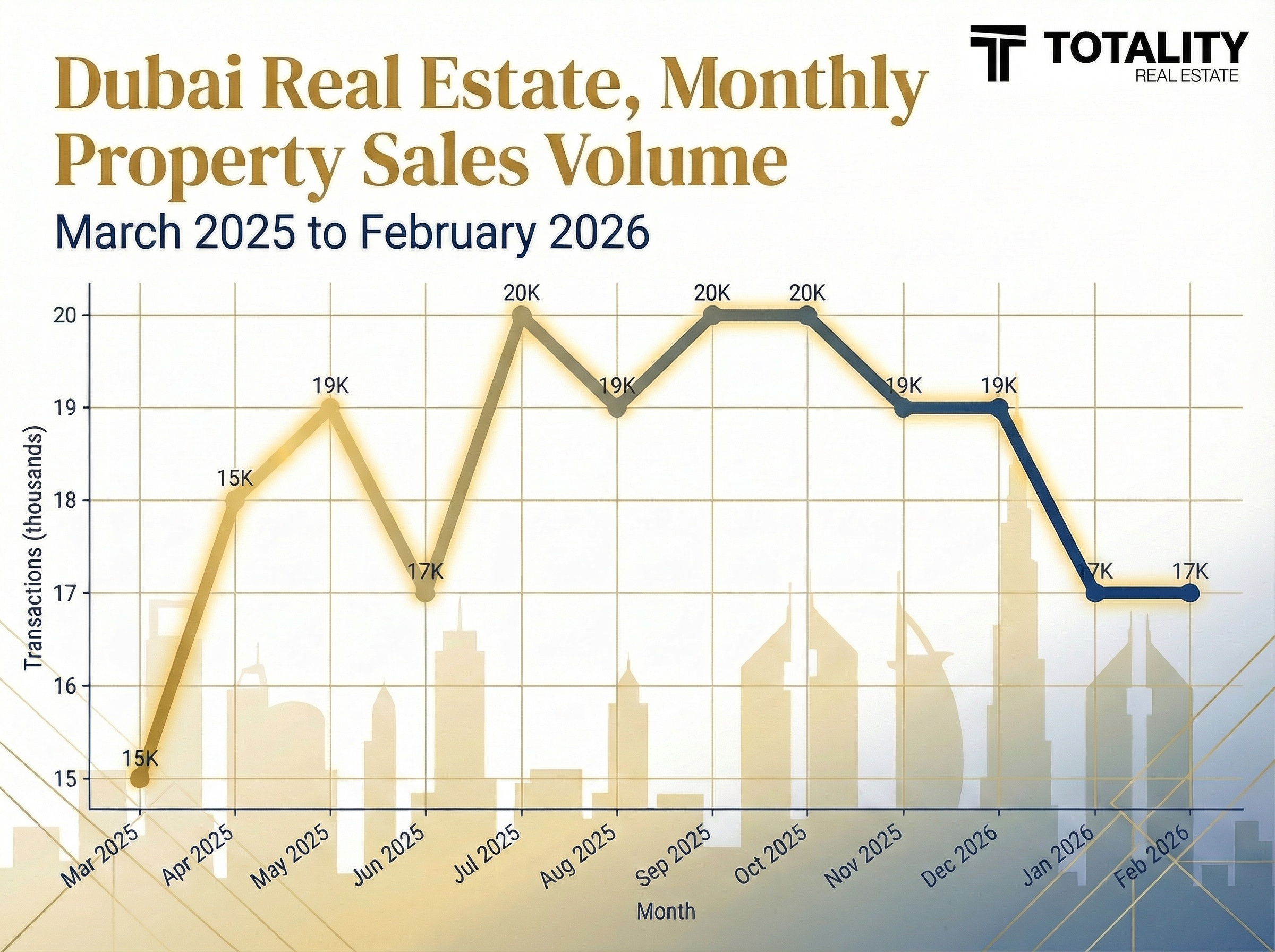

The Dubai real estate market in February 2026 kept moving at a level that still feels unusually high, even by Dubai standards. The market recorded 16,979 sales transactions worth AED 60.8 billion, with total sales value up 18.4% year on year. Off-plan remained the dominant force, accounting for 67% of sales volume and 69% of sales value, while demand concentrated heavily in areas such as Al Yelayiss 1, Al Yelayiss 5, Business Bay, Me’Aisem Second, and Dubai Islands. In other words, the market did cool a little from January, but only in the way a very hot market pauses to breathe. It did not really weaken.

And that distinction matters.

A lot of monthly Dubai property content tends to overreact to month-on-month dips, especially after a record January. I think that is a mistake, or at least an incomplete reading. February was softer than January on a few headline numbers, yes, but it still sat well above last year’s base. Sales volume slipped around 2.8% month on month , average price per square foot dipped 2.9% , and total sales value fell 16.2% from January, yet year-on-year growth stayed clearly positive. That looks much more like consolidation than reversal.

Key market highlights, February 2026

| Metric | February 2026 | MoM | YoY |

|---|---|---|---|

| Total transactions | 16,979 | -2.8% | +5.1% |

| Total sales value | AED 60.8B | -16.2% | +18.4% |

| Average price / sqft | AED 1,740 | -2.9% | +12.2% |

| Off-plan share of sales volume | 67% | - | - |

| Off-plan share of sales value | 69% | - | - |

| Mortgage transactions | 3,874 | -9.3% | +10.1% |

| Mortgage value | AED 16.4B | -49.1% | +14.3% |

February 2026 was strong, just not frantic

One thing that stands out, maybe more than it should, is how easy it is to forget what a normal month used to look like in Dubai. When you compare February 2026 with February in prior years, the change is striking. Public February-over-year charts show how much the market has scaled since 2022, both in transaction volume and value, and 2026 continues that higher plateau rather than falling away from it. Even more telling, the average price per square foot is sitting around AED 1,740, far above the roughly sub-AED 1,000 levels seen in several earlier February periods.

That does not mean every segment is running equally hard. It never really works that way.

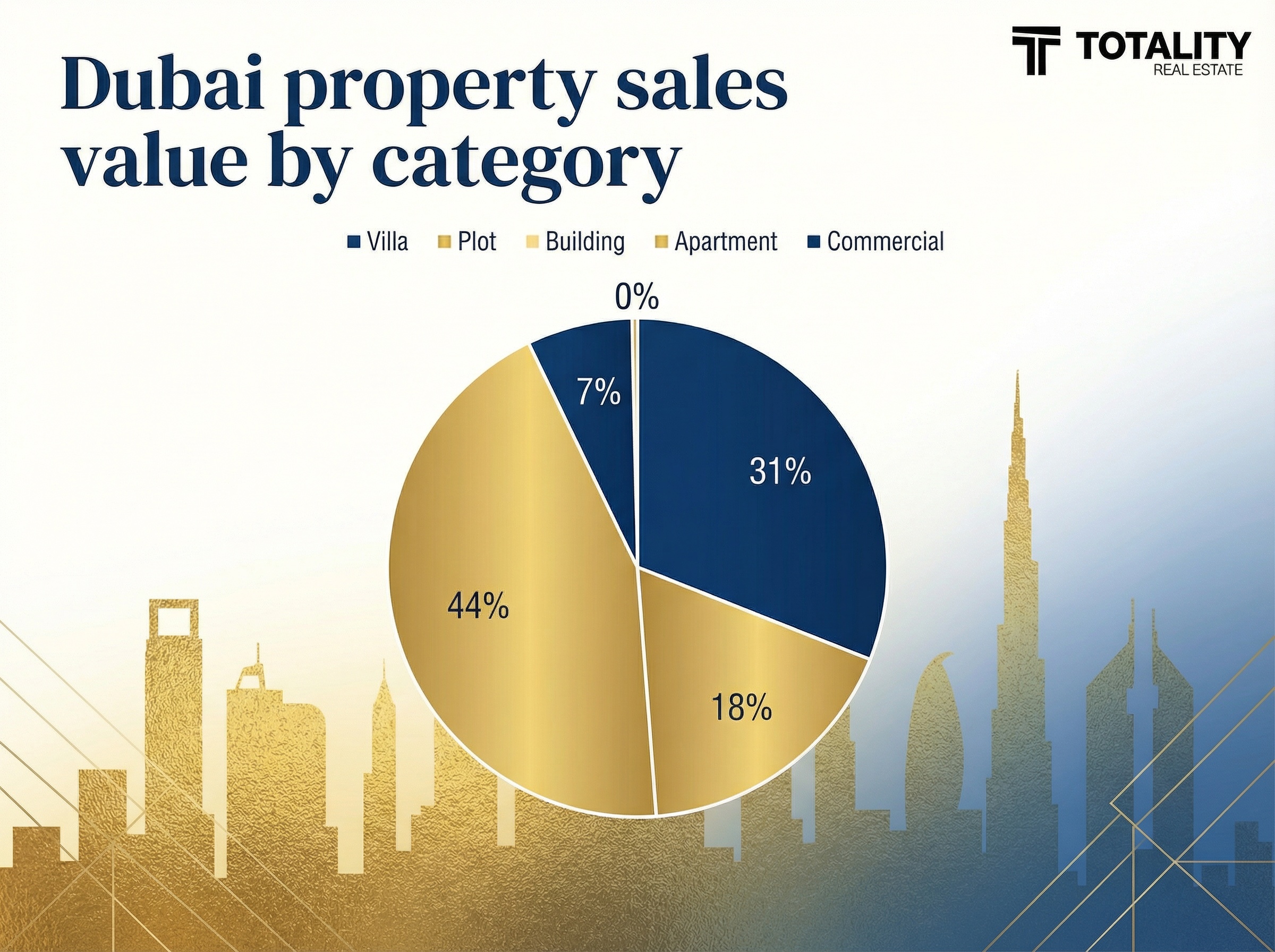

Apartments kept doing most of the heavy lifting, with 12,916 apartment transactions generating about AED 26.6 billion in sales value. Villas, meanwhile, recorded 2,802 deals worth AED 18.8 billion. Commercial was smaller in absolute size, but the year-on-year jump there was hard to ignore, with 804 transactions and a volume increase of 81.5% YoY. Plots also remained important in value terms, with 446 deals worth AED 11.2 billion. So yes, the apartment market is still the broad engine, but capital is not flowing into just one lane.

Off-plan still dominated, but that is not the whole story

The obvious headline is the off-plan share. Primary sales accounted for roughly 67% of total transaction volume and 69% of total sales value, which tells you where investor appetite still sits. Buyers are continuing to pay for future inventory, future infrastructure, future positioning. That is not new anymore, but it is still remarkable how durable that pattern has become.

Still, I would avoid writing this as though resale has become irrelevant, because it has not. The resale market represented about a third of transactions and a bit over AED 18.6 billion in value in one of the external February summaries. That is still a meaningful chunk of capital, and it matters even more because resale activity often reflects what buyers are willing to do with actual, delivered stock rather than projected delivery stories. In a way, it is the market testing itself in real time.

There is another detail here that often gets overlooked. In the resale segment, cash buyers made up roughly 69% of activity according to one of the February analyses, which suggests that a large part of the market is still being driven by liquidity, not just leverage. Personally, I think that matters a lot for market durability. It does not make Dubai immune to shocks, obviously not, but it does change the texture of demand.

Price trends, and where the market feels more nuanced

Average price per square foot reached AED 1,740 in February 2026. On paper, the month-on-month dip may look like a softening signal. But the year-on-year increase of 12.2% tells the more important story, which is that pricing is still moving upward over time, even if monthly pacing fluctuates. That pattern usually points to an active market with some short-term rotation rather than a market losing conviction.

Primary vs resale median prices

| Type | Primary market median price | Resale market median price |

|---|---|---|

| Apartment | AED 1.4M | AED 1.3M |

| Plot | AED 2.7M | AED 9.0M |

| Villa | AED 4.1M | AED 4.1M |

That apartment spread is interesting. It suggests primary still commands a premium narrative, but not an extreme one. Resale apartments at around AED 1.3M are still very much in the conversation, especially for buyers who prefer completed stock, immediate leasing, or clearer visibility on service charges and actual livability. Villas are even more interesting because the median sits at AED 4.1M in both primary and resale in your dataset. That is one of those small details that makes the market feel more balanced than the headlines imply.

Why demand still looks well supported

A big part of the backdrop is demographic, not just transactional. Dubai passed the 4 million resident mark in August 2025, according to reporting based on Dubai Statistics Centre data, and that population growth continues to feed both rental demand and end-user housing demand. It is not the only reason the market is strong, but it is one of the cleaner, less speculative reasons. More people, more households, more office demand, more schooling demand, more daily-life demand. That tends to show up in real estate sooner or later.

That is probably why the February mortgage numbers, while softer month on month, still matter. The market recorded 3,874 mortgage transactions worth AED 16.4 billion, which is not a trivial signal. Mortgage activity in Dubai is never the whole market, but it does help show that this is not purely an all-cash, investor-flip story. There is still end-user commitment in the system.

Top performing areas, where the money actually went

The top-performing locations in February 2026 tell a slightly more interesting story than the generic “prime areas stayed strong” summary you often see. Yes, prime districts were active, but the distribution of value shows that buyers were not concentrating in only the most traditional trophy addresses. In the publicly circulated February breakdowns, Al Yelayiss 1 led by sales value at roughly AED 5.38B, followed by Al Yelayiss 5, Me’Aisem Second, Business Bay, and then a fifth slot that varies by source, sometimes Palm Jumeirah, while your dashboard dataset places Dubai Islands in that top-value group. That variation is worth noting, actually, because it usually means different compilers are applying slightly different filters or grouping rules. The broader pattern, though, stays consistent, emerging growth corridors and branded or master-planned districts are absorbing serious capital.

Top 5 performing areas by sales value, February 2026

| Area | Sales Value |

|---|---|

| Al Yelayiss 1 | AED 5.5B |

| Al Yelayiss 5 | AED 2.4B |

| Business Bay | AED 2.3B |

| Me’Aisem Second | AED 2.27B |

| Dubai Islands | AED 2.2B |

Sales volume by price range, what kind of buyer dominated February?

Your source pack also shows something that I think investors should pay more attention to, the market is broad, but not evenly broad.

The AED 1M to AED 2M bracket represented the largest share of transaction volume in February 2026 at about 32%. Properties below AED 1M made up around 24%, while AED 2M to AED 3M accounted for 18%. The AED 3M to AED 5M and above AED 5M brackets each came in at roughly 13%. That distribution suggests the market is still being driven by the middle of the investment curve, not just the extreme luxury tier that gets all the headlines. And honestly, that is healthier. A market built only on mega-ticket transactions can look impressive and still be fragile. A market with real depth across the sub-AED 3M range usually has better durability.

Property sales volume by price range, February 2026

| Price Range | Share of Sales Volume |

|---|---|

| Below AED 1M | 24% |

| AED 1M to AED 2M | 32% |

| AED 2M to AED 3M | 18% |

| AED 3M to AED 5M | 13% |

| Above AED 5M | 13% |

That buyer mix also lines up with Dubai’s long-running sweet spot, efficient apartments, entry-to-mid-tier villas, and investment-led product in communities that are either newly launching or still pricing in future infrastructure. It is part of why off-plan keeps winning share. Developers are still bringing the clearest payment-plan story to the widest buyer pool.

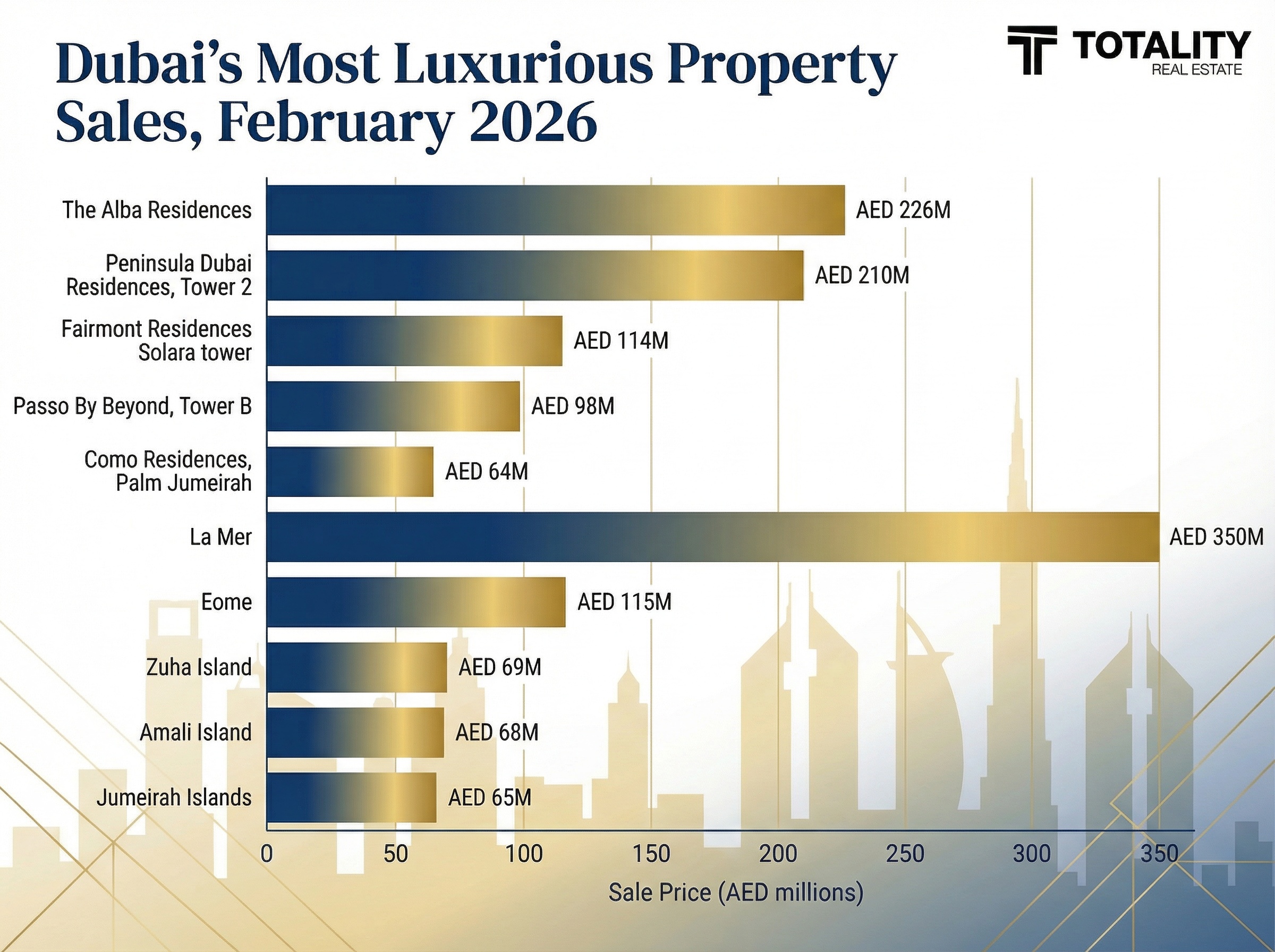

Dubai’s most luxurious property sales, the headline-grabbing end of the market

At the top end, February 2026 was still full of statement deals. Public February roundups and your own source list broadly align on the standout apartment and villa transactions, with The Alba Residences at Palm Jumeirah, Peninsula Dubai Residences Tower 2, Fairmont Residences Solara Tower, Passo by Beyond, and Como Residences among the most expensive apartment sales, while villa deals in La Mer, EOME, Zuha Island, Amali Island, and Jumeirah Islands dominated the villa side.

Top luxury apartment sales, February 2026

| Rank | Project | Price |

|---|---|---|

| 1 | The Alba Residences at Palm Jumeirah | AED 226M |

| 2 | Peninsula Dubai Residences, Tower 2 | AED 210M |

| 3 | Fairmont Residences Solara Tower, Downtown Dubai | AED 114M |

| 4 | Passo By Beyond, Tower B, Palm Jumeirah | AED 98M |

| 5 | Como Residences at Palm Jumeirah | AED 64M |

Top luxury villa sales, February 2026

| Rank | Area / Project | Price |

|---|---|---|

| 1 | La Mer | AED 350M |

| 2 | EOME | AED 115M |

| 3 | Zuha Island | AED 69M |

| 4 | Amali Island | AED 68M |

| 5 | Jumeirah Islands | AED 65M |

These numbers are eye-catching, obviously, but they also say something practical about the market. The ultra-luxury segment in Dubai is no longer a side story that occasionally spikes on a record sale. It has become a consistent branding engine for the city. Palm Jumeirah, Downtown, island living, boutique branded stock, all of that continues to shape how international capital perceives Dubai property. That does not mean every luxury asset is a good investment, not even close, but it does mean the city has built a pricing ceiling that keeps getting reset by a relatively small but very global buyer pool.

Best-selling projects, where the volume was strongest

February’s best-selling projects show the split between aspirational branding and actual deal flow. Public February summaries identify Maybach Six, Hado by Beyond, and Sierra by Iman among the best-selling apartment projects by volume and value, while villa activity was led by Damac Islands 2, Bahamas 1, Bahamas 2, and Maui.

Your more detailed project tables add even better depth, especially because they separate primary and resale.

Best-selling primary market apartments

| Project | Volume | Value | Median Price |

|---|---|---|---|

| Maybach 6, Tower B | 250 | AED 424.3M | AED 1.4M |

| Maybach 6, Tower A | 173 | AED 280.4M | AED 1.4M |

| Sierra By Iman | 167 | AED 247.4M | AED 1.3M |

| Paradise View 1 | 127 | AED 97M | AED 720K |

| Binghatti Vintage | 124 | AED 90.5M | AED 691K |

Best-selling primary market villas

| Project | Volume | Value | Median Price |

|---|---|---|---|

| Damac Islands 2, Bahamas 1 | 139 | AED 449.6M | AED 2.9M |

| Damac Islands 2, Bahamas 2 | 126 | AED 391.6M | AED 2.8M |

| Damac Islands 2, Maui | 120 | AED 439.6M | AED 2.9M |

| Salva The Heights | 120 | AED 1.0B | AED 8.4M |

| Serro 2 The Heights | 115 | AED 950.3M | AED 8.2M |

That spread is useful because it shows two versions of demand happening at once. One is value-led and volume-led, where sub-AED 1.5M apartments continue to trade strongly. The other is master-community villa demand, where buyers are willing to commit far more capital for larger-format stock, lifestyle positioning, or future family-use potential. It is not one market. It is several markets stacked together.

Resale market leaders, the completed stock story

The resale side is smaller than primary, but still very relevant, especially for investors who care about lease-up speed, real cash flow, and actual building performance instead of launch excitement.

Best-selling resale apartments

| Project | Volume | Value | Median Price |

|---|---|---|---|

| Ashjar | 47 | AED 94.8M | AED 2.0M |

| The Neighbourhood C1 | 46 | AED 92.8M | AED 1.9M |

| Sobha Creek Vistas Tower A | 31 | AED 32.9M | AED 997.7K |

| Peninsula Three | 26 | AED 50.2M | AED 1.9M |

| Peninsula Four | 25 | AED 68.8M | AED 2.1M |

Best-selling resale villas

| Project | Volume | Value | Median Price |

|---|---|---|---|

| Dubai World Central | 30 | AED 122M | AED 3.2M |

| Rukan 3 | 29 | AED 42.8M | AED 1.2M |

| District One West, Phase 1 | 13 | AED 206.2M | AED 14.2M |

| Aura | 13 | AED 69.1M | AED 5.2M |

| The Valley, Nara | 13 | AED 40.1M | AED 2.9M |

This is probably where more sophisticated buyers spend extra time. Resale does not always produce the loudest headlines, but it often gives clearer evidence of what the market is willing to absorb without developer incentives. And because cash still appears to dominate a large share of secondary activity, that segment can tell you a lot about real conviction.

Rental prices, and why this still matters for investors

Your February source set shows average annual asking rents around AED 73.9K for apartments, AED 183.8K for villas, and AED 75K for commercial, with apartments and villas both moving up month on month, while commercial rents softened. That is not a complete rental market study, of course, but it does reinforce the broader idea that end-user and tenant demand are still providing a floor under pricing. Combined with population growth and ongoing household formation, it helps explain why Dubai has not just been trading on speculative momentum alone. Dubai crossed 4 million residents in August 2025, and that expansion continues to feed underlying housing demand.

Market outlook for Dubai real estate after February 2026

The simplest way to read February 2026 is this, the Dubai property market is still expanding, but it is doing so with a little more texture than the headline numbers alone suggest.

Transaction volume cooled slightly from January. Sales value also came off the prior month. But the broader pattern still points upward. Public February coverage based on Dubai Land Department referenced data shows sales value up roughly 18.1% to 18.4% year on year, while total transactions rose about 5% YoY. At the same time, external reporting still shows the market heavily tilted toward off-plan, although the exact split varies by dataset. Some February summaries put off-plan near 62% of sales volume, while your source dashboard shows a stronger 67% share, which likely comes down to filtering and transaction classification. Either way, the conclusion is basically the same, primary market demand remains the dominant force.

That matters, because it shapes what kind of market this is.

It is not just a resale-driven recovery story anymore. It is not just a luxury-market headline cycle either. It is a developer-led, capital-rich, population-supported market where launch strategy, payment plans, infrastructure narratives, and district selection still carry unusual weight. Maybe more than some people want to admit.

At the same time, I would be careful with overly easy optimism. A strong market does not mean every project is strong. A rising city does not rescue weak layouts, inflated entry points, or poor developer execution. Dubai can reward buyers very well, but it also punishes lazy underwriting.

What February 2026 means for different buyer types

For investors

Investors should probably read February as a confirmation month, not a surprise month. The market did not suddenly break out, because it had already been strong. What February did was reinforce three things:

| Investor signal | What February 2026 suggests | Why it matters |

|---|---|---|

| Off-plan still leads | Primary market continues to absorb most volume and value | Project selection and payment-plan structure remain critical |

| Mid-market remains deep | AED 1M to AED 2M stock still drives a large share of demand | Liquidity is not limited to ultra-luxury buyers |

| Resale still matters | Ready stock remains a meaningful slice of value and volume | Cash flow, tenantability, and actual building quality still win |

The temptation in Dubai is often to chase what looks glamorous. But some of the most durable outcomes still come from ordinary things, efficient floor plans, realistic handover schedules, service-charge discipline, and areas where transport, retail, and daily convenience are catching up to pricing. That part is less exciting to post on social media, maybe, but it is usually where better investing lives.

For end users

February’s mortgage activity also matters for genuine occupiers. Public February reporting shows around 3,867 to 3,874 mortgage transactions with total mortgage value near AED 16.4B, which supports the argument that this is not purely a speculative cash market. There is still meaningful financed demand in the system, even with cash buyers remaining very active in the resale market.

For end users, that means two things at once. First, competition is real, especially in good communities and good buildings. Second, there is still room to buy intelligently, because not every area is pricing the same way and not every segment is moving with the same intensity.

For brokers and referral partners

This is the kind of month that tends to reward specificity. A generic “Dubai is booming” message will get attention, but not trust. A sharper message works better:

-

show where value concentrated

-

explain why off-plan is winning

-

separate investor stock from end-user stock

-

compare primary versus resale honestly

-

demonstrate what the numbers mean for cash flow, hold period, and resale liquidity

That is the kind of framing more serious buyers respond to.

The bigger structural support behind the market

A lot of the confidence around Dubai still comes back to one basic reality, more people are moving into the city, and that changes almost everything.

Dubai’s population crossed 4 million in August 2025, reaching 4,000,387 according to reporting that cited the Dubai Statistics Centre population clock. That is not just a symbolic milestone. It feeds rental demand, school demand, transport demand, office demand, and ultimately housing demand across multiple income bands. In practical terms, it gives the real estate market a deeper domestic base than a purely investor-led story would imply.

That does not mean supply risk disappears. It does not. But it does mean the conversation is more nuanced than “prices up because investors keep buying.” Population growth, household formation, and business activity are still part of the engine.

A balanced conclusion, not a sales pitch

So, was February 2026 a strong month for Dubai real estate?

Yes, clearly.

Was it a straight-line continuation of January’s intensity?

Not exactly.

And that is probably healthy. Markets that move in only one direction, too quickly, without pauses, tend to become fragile. February looked more like a market that is still strong, still liquid, still trusted, but beginning to show the normal rhythm of rotation between districts, price bands, and buyer profiles.

That is a better environment for serious analysis.

The headline takeaway is still positive. Dubai recorded a very high transaction count, a very high sales value, sustained off-plan dominance, active mortgage participation, and continued appetite in both investment districts and prime branded addresses. The more useful takeaway, though, is that project quality and location quality matter more now, not less. In a broad rising market, buyers can get away with average decisions. In a more selective version of the same market, the gap between good stock and merely marketable stock starts to widen.

I think that is where 2026 gets interesting.

FAQs

Is Dubai real estate still growing according to February 2026 market data?

Yes. February 2026 remained firmly above February 2025 on both sales value and transaction volume in public market summaries, even though month-on-month figures softened from January. That points more toward consolidation than a broad reversal.

What was the total sales value in Dubai in February 2026?

Your source pack shows AED 60.8 billion. Public February reports based on DLD-referenced figures commonly cite about AED 60.6 billion, so there is a small variation depending on source methodology.

Did off-plan or ready properties perform better in February 2026?

Off-plan clearly led the market. External February reporting places off-plan at about 62% of sales volume, while your internal dashboard shows 67%. Either way, primary sales remained the dominant segment.

Which Dubai areas performed best in February 2026?

Your dataset highlights Al Yelayiss 1, Al Yelayiss 5, Business Bay, Me’Aisem Second, and Dubai Islands among the top-value areas. Public February summaries also consistently place Al Yelayiss 1 and Business Bay among the strongest-performing districts.

What was the average Dubai property price per square foot in February 2026?

Based on your source material, the citywide average was about AED 1,740 per square foot, with a slight month-on-month dip but still solid year-on-year growth.

Are mortgages still active in Dubai’s property market?

Yes. Public February reporting shows roughly 3,867 mortgage transactions worth AED 16.43 billion, which indicates financed end-user demand is still part of the market, even in a city where cash remains highly influential.

Is Dubai real estate slowing down in 2026, or is February just a pause?

February looks more like a pause than a reversal. One widely cited February 2026 recap puts the market at 16,979 sales worth AED 60.8 billion, up 5.1% year on year in volume and 18.4% in value. Another DLD-based report shows 16,959 sales worth AED 60.6 billion, which is slightly different, but the direction is the same. Month on month, the market cooled a bit from January. Year on year, it was still clearly higher. That is not the profile of a market that has suddenly rolled over.

Are off-plan properties still outperforming ready homes in Dubai?

Yes, off-plan was still leading in February 2026. One market summary shows the primary market at 11,351 transactions worth AED 42.1 billion, compared with 5,628 resale deals worth AED 18.6 billion. A DLD-based article reports 10,526 off-plan transactions, or roughly 62% of total sales. So the exact share varies by source, but the larger conclusion does not really change, primary sales are still dominating the market.

Which Dubai areas were leading the market in February 2026?

The strongest names by sales value kept repeating across February coverage. Al Yelayiss 1 was the standout leader, followed by Al Yelayiss 5, Me’Aisem Second, and Business Bay. One February roundup also placed Palm Jumeirah in the top five by value. That mix is interesting because it shows demand splitting between emerging, master-planned growth corridors and established core districts with deeper liquidity.

Are mortgages still active, or is Dubai mostly a cash market now?

Mortgages are still very much part of the market. February 2026 coverage shows about 3,867 to 3,874 mortgage transactions with total mortgage value around AED 16.4 billion. At the same time, one February report said cash buyers made up more than two-thirds of resale activity. So the better answer is not “cash or mortgage.” It is both, with cash dominating parts of the secondary market while financed demand remains meaningful, especially for end users.

Is Dubai still a good real estate market for investors in 2026?

It still looks attractive, but it is no longer a market where almost everything rises together. The positive case is clear enough: Dubai’s population passed 4 million in August 2025, the rental sector recorded 1.38 million tenancy contracts in 2025, and DLD said rental contract value rose 17% year on year to AED 126.4 billion. Those are solid underlying demand signals. But the market is also becoming more selective, which means investors probably need better underwriting now than they did two years ago.

Are rents still supporting the investment case in Dubai?

Yes, and this is one of the more important support pillars. DLD said registered tenancy contracts in 2025 rose 6% in volume and 17% in value, while new tenancy contracts climbed more than 10%. That suggests the rental market is not just active, it is broad enough to support the sales market story. A strong ownership market with a weak rental market can get fragile. Dubai, at least on the official 2025 rental data, did not look weak on that front.

What should buyers verify before buying an off-plan property in Dubai?

The short answer is, more than the brochure. Dubai Land Department’s official FAQ says buyers can track project status by plot number, project number, or project name, including a project’s completion percentage and status. DLD’s open-data portal also lets users filter transactions by sales, mortgages, gifts, registration type, area, usage, and property type, and export data as CSV. That means buyers can check whether a project is active, how the area is trading, and whether the story around the asset is actually visible in the market.

Property Finder’s January 2026 buyer guide adds the practical layer: verify freehold status, make sure key documents such as the title deed or relevant paperwork are in place where applicable, budget for service charges and closing costs, and check the developer’s track record. For off-plan specifically, it explicitly says escrow verification is essential.

Can you get a mortgage for an off-plan property in Dubai?

Yes, but it is more limited than a mortgage on a ready property. DLD’s FAQ says real estate projects can be mortgaged if the mortgage amount is deposited into the project’s escrow account. Property Finder’s March 2026 guide says off-plan mortgages are available, but notes that financing is more selective, often with 50% loan-to-value as a working ceiling and not all banks participating. In practice, that means off-plan financing exists, but buyers should not assume it will be as flexible as financing a completed unit.

What are the biggest risks investors should watch in Dubai real estate in 2026?

The main risk is not that Dubai suddenly stops attracting capital. It is that supply, pricing, and project quality start to separate winners from weaker stock more aggressively. Fitch said in 2025 that Dubai prices could face a double-digit decline as new supply comes through, while Reuters reported in March 2026 that the market was facing a tougher test after regional security shocks hit investor sentiment. Those are not reasons to dismiss the market. They are reasons to be more selective about location, developer strength, and exit liquidity.

Can first-time buyers still find a way into the Dubai market?

Yes, especially if they stay realistic on budget and product type. Dubai Land Department’s First Time Home Buyer page says participating developers and banks may offer priority access to launches, preferential off-plan pricing, flexible payment plans, and better financing terms. That does not make the market cheap, obviously. But it does mean the path into the market is still being actively supported, particularly on the off-plan side.

How can buyers verify whether a Dubai market report is reliable?

A good rule is to cross-check any market summary against Dubai Land Department open data, look for whether the report clearly separates off-plan and ready transactions, and watch for small source discrepancies. February 2026 is a good example: some summaries cite 16,959 sales and AED 60.6 billion, while others use 16,979 sales and AED 60.8 billion. That does not automatically make one wrong, but it does mean serious buyers should prefer reports that show methodology, segmentation, and source transparency.

Conclusion

February 2026 confirmed that Dubai remains one of the most dynamic real estate markets in the world, but dynamic markets reward precision, not impulse. As the city grows, the gap between average assets and exceptional ones is becoming wider. The winners will not be the people who buy the loudest opportunity. They will be the ones who buy with clarity.

That is exactly where we operate.

While much of the market is built around selling projects, we are built around grading, verifying, and analyzing real estate opportunities through data and predictive analytics. Our role is not simply to show investors what is available. It is to help them understand what is likely to perform, what risks deserve more scrutiny, and where genuine long-term value is most likely to be created.

We believe the future of real estate advisory belongs to firms that think beyond transactions. Firms that treat property as a strategic asset class. Firms that help investors move from guesswork to evidence, from marketing to verification, and from short-term buying decisions to long-term wealth creation.

That is the space we are building in.

Not just another brokerage. Not just another source of listings. A more intelligent real estate company designed for investors who want to build wealth across generations with sharper insight, stronger discipline, and a clearer edge.