Dubai Investment Blog

Investor-focused articles on Dubai property strategy and execution

200+ articles for Dubai property investors and end-users. We cover market mechanics (DLD transactions, mortgage caps, RERA rules), strategy (off-plan vs ready, branded residence premiums, exit timing), and tactics (financing structuring, snagging, tenancy management). All articles are written by the advisory team — no SEO-farm content.

Most-read categories

Investment strategy, market analysis, off-plan due diligence, mortgages and financing, Golden Visa, area guides (long-form), tax and residency, sell-side strategy.

All Articles

213 articles on Dubai property strategy, market analysis and execution

Dubai Real Estate Market May 2026: A Shift Toward Maturation and End-User Utility

Dubai Real Estate Market · 2 Jun 2026

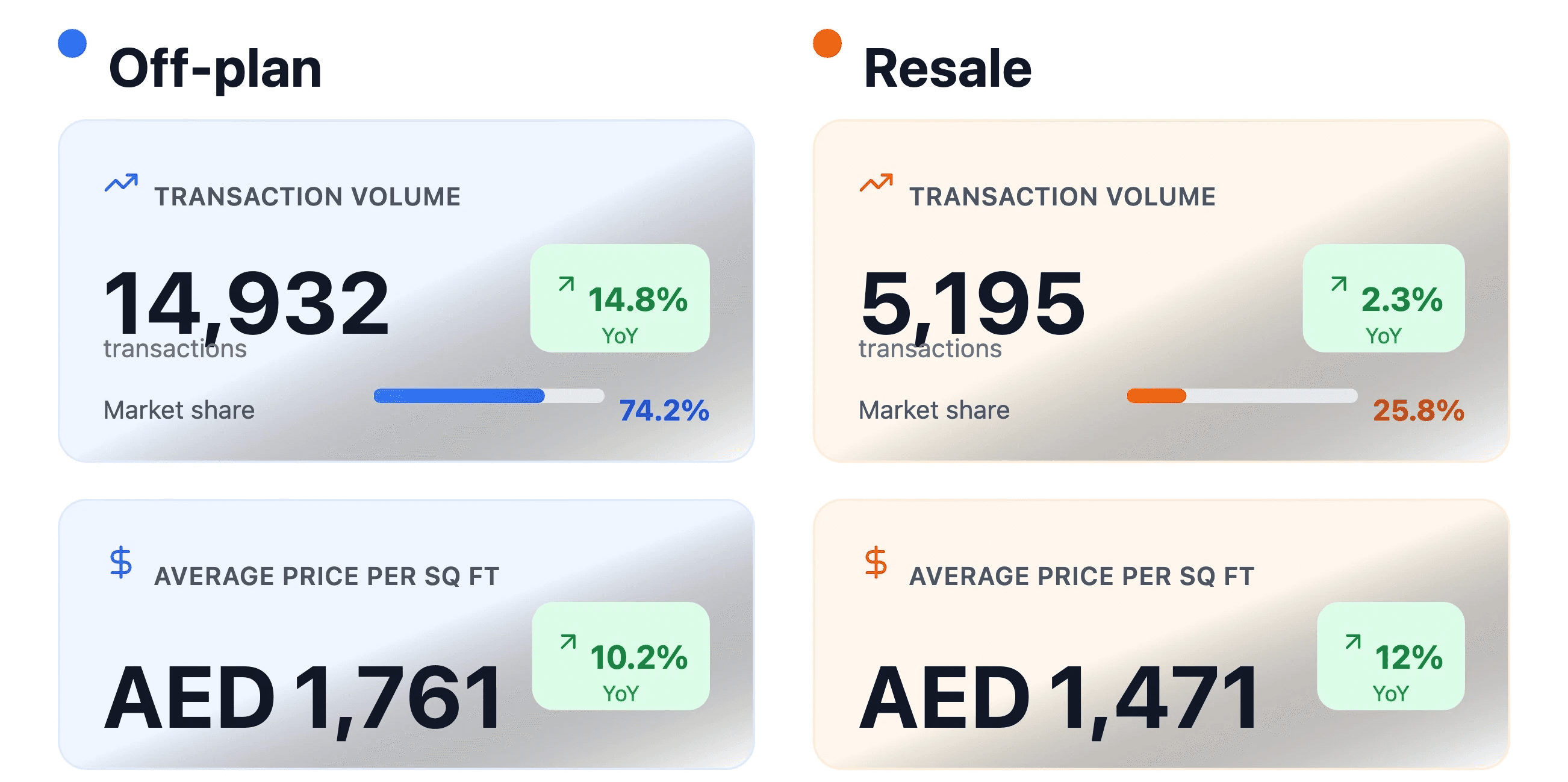

Dubai's May 2026 market: 10,281 transactions worth AED 28.9B. Volumes cooling, prices sticky at AED 1,650/sqft. The full data, project…

Why the UAE Attracts Global Capital

Investment Intelligence · 25 May 2026

The UAE pulls in global capital for reasons that are less about the skyline than people assume. Near-zero tax, real stability, a location…

The Ultimate Guide to Dubai Real Estate Investment, 2026

Dubai Real Estate · 15 May 2026

Dubai real estate investment in 2026 remains attractive for investors seeking rental income, capital appreciation, tax efficiency and UAE…

Dubai Off-Plan Properties: Goldmine or Death Trap?

Investment Insights · 14 May 2026

UK guide to Dubai off-plan: pricing, 60/40 plans, escrow protection, 5–7% yields, Golden Visa (AED 2M), key risks, timelines, and ROI tips.

Bugatti Residences Completion Date: Everything You Need to Know

Bugatti Residences · 7 May 2026

Bugatti Residences by Binghatti is currently targeting Q1 2027 completion. With 52.29% construction progress as of January 2026 according…

1 Bedroom Apartments for Sale Dubai Marina, Prices, Yields and Best Buildings for Investors

Dubai Marina Apartments · 5 May 2026

Investor guide to 1 bedroom apartments in Dubai Marina: real pricing across entry, mid-market, and premium tiers, top 5 buildings,…

Marina Gate Dubai: Investor Guide to Towers I, II & Jumeirah Living

Marina Gate · 5 May 2026

Investor guide to Marina Gate Dubai: tower-by-tower pricing across Marina Gate 1, 2 and Jumeirah Living, AED 3,090/sqft median, 7% yield,…

Apartments for Sale in Dubai Marina: Prices, Yields and Investment Guide

Communities · 4 May 2026

Dubai Marina apartment investor guide for 2026: pricing by unit type, top buildings, the buying process for foreign nationals, realistic…

Dubai Real Estate Market Overview April 2026: A Market Recovering After the Iran Conflict Reset

Market Report · 4 May 2026

Dubai recorded AED 68.56B in real estate transactions in April 2026, up 20% MoM despite regional tensions. A full breakdown of off-plan…

Waterfront Apartments Dubai: The Complete Investor's Guide for 2026

Waterfront apartments in Dubai · 2 May 2026

A 2026 investor's guide to Dubai's waterfront apartment market. District-by-district analysis of Marina, Emaar Beachfront, Creek Harbour,…

Dubai Townhouses: Your Ultimate Guide to Luxury Living and Investment in 2026

Dubai Real Estate · 1 May 2026

Townhouses in Dubai now range from AED 2M to AED 6.2M+. A practical 2026 guide to communities, foreign ownership rights, financing,…

How To Invest in Dubai Property With Only $50,000

Real Estate Investing · 28 Apr 2026

With $50,000 USD, roughly AED 183,000, you can invest in Dubai property in several practical ways. You could use real estate crowdfunding…

Bugatti Residences Floor Plans: Sky Mansions, Riviera Mansions, and Which Unit Is Best Value?

Bugatti Residences · 24 Apr 2026

Bugatti Residences by Binghatti in Business Bay, Dubai, offers 171 ultra-luxury Riviera Mansions and 11 Sky Mansion Penthouses, ranging…

Top 4 Real Estate Investment Areas in UAE

Real Estate Investment · 22 Apr 2026

The top 4 investment areas in the UAE right now are Dubai Islands, Dubai Maritime City, Al Marjan Island, and Yas Island. I think what…

Why Invest in Dubai Property, Complete Guide for Foreigners

Property Investment · 15 Apr 2026

Yes, foreigners can legally invest in Dubai property, but only in designated freehold areas. In those zones, non-UAE nationals can buy,…

Bugatti Residences vs. Lamborghini Dubai vs. Mercedes-Benz Places: The Ultimate Comparison

Automotive Branded Residences · 13 Apr 2026

The best automotive branded residence in Dubai for 2026 depends on what you actually want to buy. If you want the strongest trophy asset…

UAE or Switzerland for UHNW in 2026-2027?

Market Insight · 12 Apr 2026

The UAE suits UHNW investors focused on tax efficiency, residency, and growth. Switzerland suits those prioritizing wealth preservation,…

Dubai Property Market Report March 2026: Prices, Sales, Trends & Forecast

Market Report · 10 Apr 2026

The Dubai property market in March 2026 looked softer on a month-to-month basis, but the broader picture still points to a market that is…

Why Bugatti Residences can't compare to Mercedes-Benz Places?

Branded Residences · 4 Apr 2026

Bugatti Residences and Mercedes-Benz Places sit in the same branded luxury conversation, but they are not really the same type of bet.…

Top Real Estate Developers in the UAE (2025-2026)

Real Estate Developers · 3 Apr 2026

The top real estate developers in the UAE in 2025 and 2026 are Emaar Properties, Aldar Properties, Nakheel, Sobha Realty, Meraas, DAMAC…

UAE Real Estate Investment Guide 2026

UAE Real Estate · 2 Apr 2026

Yes, for strategic investors. While the early 2026 geopolitical tensions caused a temporary pause in speculative buying, the underlying…

Why Smart Money Invests in Dubai, Tax Efficiency, Yield, Safety, and Growth

Investing · 31 Mar 2026

Smart money, meaning family offices, high-net-worth individuals, entrepreneurs, and globally mobile investors, is drawn to Dubai because…

Best Residential Areas in Dubai: Top Communities by Lifestyle, Budget, and Investment Goals

Communities · 30 Mar 2026

The best residential areas in Dubai for 2026 usually come down to three things, lifestyle, budget, and daily practicality. Palm Jumeirah…

Bugatti Residences Amenities, Luxury Features in Business Bay Dubai

Branded Residences · 29 Mar 2026

Bugatti Residences by Binghatti in Business Bay offers a rare mix of branded ultra-luxury design and service-led living. Officially…

Dubai Islands vs Palm Jumeirah: Which Dubai Waterfront Area Is Better for Living and Investment?

Waterfront Communities · 28 Mar 2026

Palm Jumeirah is the more established, globally recognized waterfront address in Dubai, with a mature resale market, ready luxury stock,…

Buying Off-Plan Property in Dubai: A Strategic Guide for Investors

Off Plan · 26 Mar 2026

Buying off-plan property in Dubai involves securing a unit directly from a developer before completion, usually with a 10 to 25 percent…

Bugatti Residences Price Guide: How Much Does It Actually Cost?

Bugatti Residences · 25 Mar 2026

Bugatti Residences price in Dubai starts from around AED 19 million for Riviera Mansions and rises to AED 130 million+ for Sky Mansion…

Dubai Islands Master Plan: Complete Guide to the 5 Islands

Communities · 24 Mar 2026

The Dubai Islands master plan is a transformative 17 sq km waterfront mega-development by Nakheel, comprising five uniquely themed islands…

Ras Al Khaimah Real Estate Guide, Best Areas, Prices, ROI & Buying Tips

Ras Al Khaimah · 22 Mar 2026

Ras Al Khaimah, often shortened to RAK, is becoming one of the most watched real estate markets in the UAE because it offers a growing,…

The Rising Star of Dubai Real Estate: Why Investors Are Flocking to Dubai Islands

Investment Insights · 21 Mar 2026

Dubai Islands Real Estate Guide 2026 and Beyond: Why Investors Are Targeting This Waterfront Mega Project | Totality Estates

Dubai Islands: An Investment Deep Dive (2026-2027 Outlook)

Investment Insights · 21 Mar 2026

Dubai Islands offers rare beachfront investment, blending luxury living, tourism, and growth potential in one of Dubai’s most ambitious…

Comparative Investment Outlook: Al Marjan Island vs. Dubai Islands (2026-2030)

Investment Insights · 20 Mar 2026

When you're looking at the UAE's coastal real estate market right now, it's hard not to feel a bit overwhelmed by the sheer scale of…

Can You Buy Property in Dubai for $250K? Your Guide to Affordable Real Estate

Dubai Properties · 17 Mar 2026

Yes, you can absolutely buy property in Dubai for $250,000 (approximately AED 918,000), opening doors to studio or one-bedroom apartments.…

RAK Central in Ras Al Khaimah, Location, Master Plan, Investment Potential and 2026-2027 Update

Communities · 15 Mar 2026

RAK Central is a major mixed-use district in Ras Al Khaimah, planned by Marjan as a new urban heart for the emirate. Positioned along…

Mina Al Arab, Ras Al Khaimah Area Guide, Lifestyle, Property Types, Prices & Investment Insight

Communities · 12 Mar 2026

Mina Al Arab is a waterfront master-planned community in Ras Al Khaimah developed by RAK Properties. It is known for its beaches,…

Best Family Areas in Dubai to Live: Honest Guide for Parents Choosing the Right Community

Communities · 10 Mar 2026

If you’re searching for the *best family areas in Dubai to live* in 2026-2027, the strongest all-round choices are Dubai Hills Estate,…

Dubai Real Estate Market Report February 2026, Prices, Sales, Off-Plan Trends

Market Report · 8 Mar 2026

The Dubai real estate market in February 2026 kept moving at a level that still feels unusually high, even by Dubai standards. The market…

Townhouse Communities in Dubai, Best Areas for Families, Lifestyle, and Investment

Townhouse Communities · 7 Mar 2026

Dubai’s top townhouse communities really do sit on a spectrum, you can feel it the moment you drive in. Some are established and calm,…

Meydan Dubai, a Living Guide to the District that Keeps Surprising Investors

Communities · 5 Mar 2026

Meydan in Dubai is one of those places that sounds simple on paper, “a luxury mixed use district in Nad Al Sheba”, but then you spend an…

Top Communities to Buy Properties in Meydan

Communities · 3 Mar 2026

Meydan, set inside Mohammed Bin Rashid City (MBR City), keeps showing up on investor shortlists for a reason. It sits close to Downtown…

DIFC area guide, Dubai International Financial Centre

Communities · 26 Feb 2026

Dubai International Financial Centre, usually just called DIFC, is one of those places in Dubai that feels like it has its own gravity. It…

Bugatti Residences Information (Business Bay), what it is, what makes it different, and what to verify before you buy

Branded Luxury Residences · 26 Feb 2026

Bugatti Residences by Binghatti is a Bugatti branded, ultra luxury residential project in Business Bay, Dubai, marketed around a French…

Luxury Apartments for Sale in Dubai Creek Harbour

Luxury Apartments · 24 Feb 2026

Luxury apartments in Dubai can feel a bit noisy on paper because everything is “luxury” these days, but this area is one of the few that…

Dubai Maritime City Investment Guide for 2026 Buyers

Communities · 22 Feb 2026

Dubai Maritime City (DMC) is a massive 249-hectare man-made peninsula development. Positioned between Port Rashid and Drydocks World, it…

Off Plan Projects in Dubai (2026), what’s actually worth watching, and how to buy without getting sloppy

Off-Plan Properties · 19 Feb 2026

Dubai’s 2026 off plan market is leaning hard into high end, sustainability-led, and waterfront masterplans, mostly from the usual…

Why Family Offices Are Moving to Dubai

Family Office DIFC · 17 Feb 2026

Family offices are rapidly moving to Dubai to tap into a genuinely rare mix, a 0% personal tax environment, a high-end lifestyle that is…

Why invest in Emaar Beachfront?

Emaar Beachfront Community · 16 Feb 2026

Investing in Emaar Beachfront is attractive for a simple reason that sounds obvious, but still matters, it is one of the rare “central…

15 Things You Need to Know Before Buying Off Plan in Dubai in 2026

Off Plan Dubai · 14 Feb 2026

Buying off-plan in Dubai in 2026 needs a more cautious, data-driven approach than it did a couple of years ago, mostly because the market…

Living in Dubai as an American: The Truth No One Tells You (Pros and Cons)

Living in Dubai · 13 Feb 2026

Living in Dubai as an American can feel like a lifestyle upgrade, high safety, modern infrastructure, and no UAE personal income tax. But…

Rashid Yachts and Marina Real Estate, Guide for Buyers and Investors Who Actually Want Clarity

Communities · 11 Feb 2026

Rashid Yachts & Marina (sometimes still called Mina Rashid) is one of those Dubai waterfront communities that feels like it should be…

Emaar Beachfront Prices 2026, a realistic, numbers-first guide for investors

Luxury Beachfront Community · 10 Feb 2026

In 2026, Emaar Beachfront property prices are widely expected to keep pushing upward, with many buyers planning around a working band of…

Al Marjan Island Projects (Ras Al Khaimah), the investor guide to what is actually happening, and what to watch next

Market Insights · 8 Feb 2026

Al Marjan Island in Ras Al Khaimah is in that rare “before and after” moment. You can feel it. New launches keep appearing, branded names…

Al Marjan Island Real Estate Price & Yield Analysis 2025-2026

Investment Insights · 8 Feb 2026

Al Marjan Island is in a fast repricing phase going into 2026, largely because the Wynn resort pipeline is pulling attention, and supply…

List of Villa Communities in Dubai (2026), A Guide to Choosing the Right One

Villa Communities Dubai · 7 Feb 2026

Dubai offers a wide range of premier villa communities catering to luxury, family friendly, and more affordable lifestyles, with popular…

Dubai Property Fees and Charges (UAE Guide 2026), DLD Transfer Fee, Oqood, Mortgage Costs, Service Charges

Property Fees and Charges · 7 Feb 2026

Dubai property fees typically land around 7% to 10% of the purchase price once you add everything up, especially on a normal resale deal.…

Is MGM Coming to Dubai? The clearest update on the MGM Dubai project, what’s confirmed, what’s not, and why investors care

Market Insights · 5 Feb 2026

Yes, MGM is coming to Dubai, but not in the quick, headline-friendly way people tend to imagine.

Why My Dubai Property Is Not Selling and What You Can Actually Do About It

Market Insights · 5 Feb 2026

Dubai properties often struggle to sell for reasons that feel annoyingly simple in hindsight, overpricing, weak marketing, or a…

How to Buy Off-Plan Below Market Price (15% to 35% Discounts), The Distressed Deal Playbook for 2026

Distressed Deals · 5 Feb 2026

Buying off-plan property significantly below market price requires targeting “distressed” deals, units where the original buyer needs to…

Dubai Design District (d3) Overview

Communities · 4 Feb 2026

Dubai Design District, known as d3, is a premier, purpose built creative ecosystem in Dubai dedicated to design, fashion, art, and…

Why invest in Dubai Creek Harbour in 2026

Communities · 3 Feb 2026

Dubai Creek Harbour is a masterplanned waterfront district built by Emaar Properties, designed to feel like a complete piece of city, not…

Dubai Real Estate Market Overview, January 2026

Market Report · 2 Feb 2026

Dubai’s real estate market began January 2026 by setting historic records, reaching its highest ever monthly transaction value. The market…

HADO by Beyond in Dubai Islands, a Japanese inspired waterfront launch in SIØRA

Investment · 2 Feb 2026

If you have been tracking Dubai Islands for a while, HADO by Beyond is one of those launches that makes you pause. Not because it is loud,…

Hudayriyat Island real estate investment guide

Investment Guide · 1 Feb 2026

Al Hudayriyat Island is one of those places where the lifestyle story and the investment story are basically glued together. The island is…

Mercedes Benz City Dubai: Mercedes-Benz Places Binghatti City

Off-Plan Branded Residences · 30 Jan 2026

Mercedes-Benz City by Binghatti is being positioned as the world’s first Mercedes-Benz branded city, not just a single tower with a logo…

Why Are Billionaires Moving to Dubai?

Dubai Investment & Wealth Migration · 28 Jan 2026

Billionaires are moving to Dubai for a mix of reasons that are almost boring on paper, then weirdly powerful in real life. The headline is…

Best Off Plan Projects in Dubai to Buy in 2026, High Probability Upside Plays Toward Doubling by 2030

Off Plan Projects · 27 Jan 2026

Disclaimer: Market performance varies, this guide focuses on 2025-2026 launches and areas with strong catalysts, developer credibility,…

Buy Property in Dubai, A Practical Step-by-Step Guide for Foreign Buyers

Dubai Buyer Guide · 26 Jan 2026

Buying property in Dubai is, honestly, more straightforward than many people expect. Foreign nationals can purchase in designated freehold…

Why My Dubai Property Is Not Selling, The Real Problem Nobody Says Out Loud

Seller Resources · 25 Jan 2026

There’s a lot of content out there explaining why sellers struggle to resell on the secondary market. Most of it sounds reasonable. “The…

Thinking About Azizi Riviera? The Complete Community Guide, And the Hidden Resale Problem Owners Don’t See

Dubai Communities · 24 Jan 2026

Azizi Riviera is a large, French Riviera inspired waterfront community in Meydan (District 7), inside Mohammed Bin Rashid City (MBR City),…

Tilal Al Ghaf Dubai, the lagoon lifestyle community that keeps getting searched (and for good reason)

Dubai Communities · 21 Jan 2026

Tilal Al Ghaf is a large, family-focused mixed-use community by Majid Al Futtaim in Dubai, and it’s best known for resort-style living…

Best Luxury Branded Residences in Dubai: Where Savvy Investors Park Capital and Live in 7-Star Comfort

Luxury Residences in Dubai · 18 Nov 2025

Discover the best luxury branded residences in Dubai - Bvlgari, Royal Atlantis, W Residences, Bugatti, Six Senses and more - with…

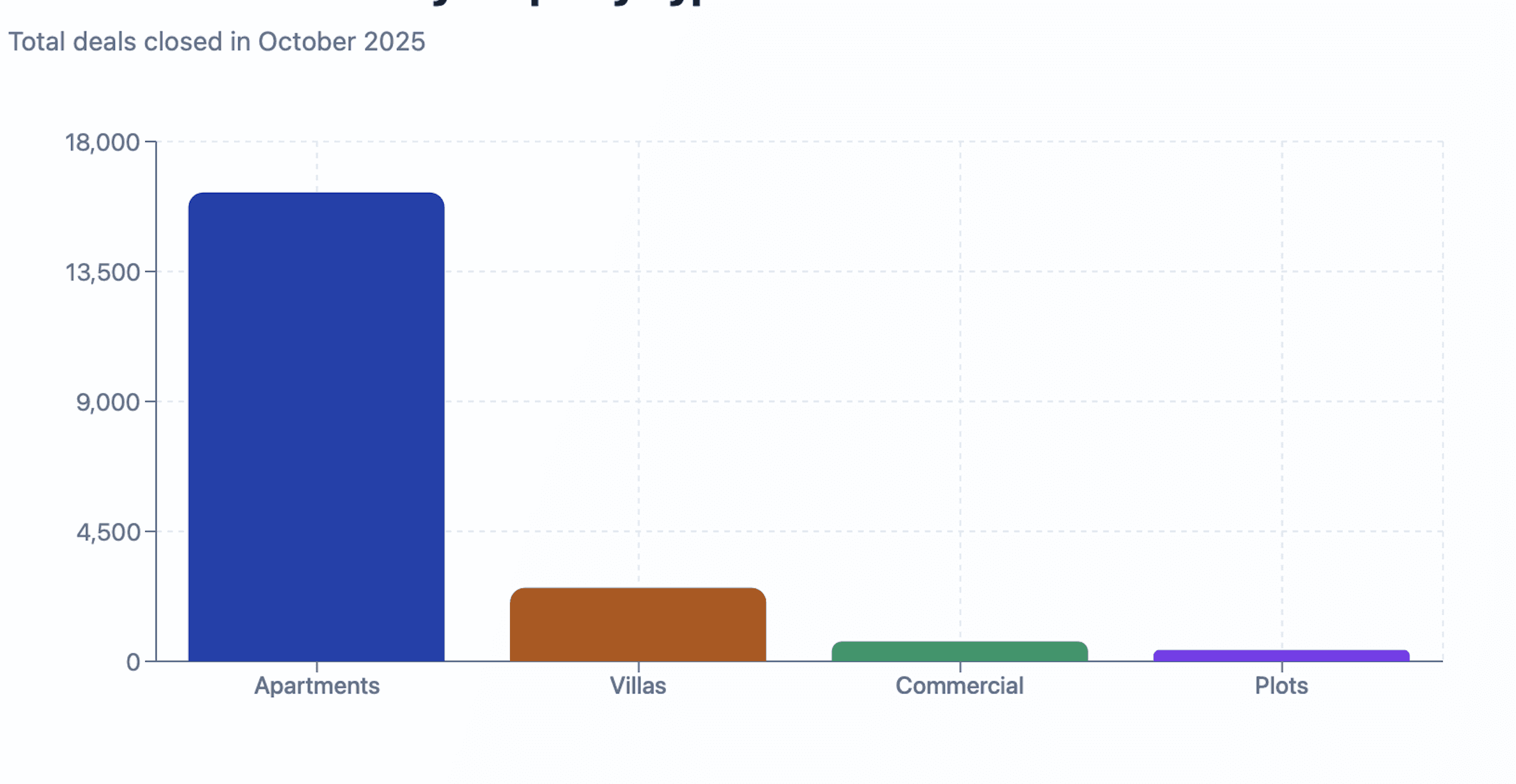

Dubai Sales Stats October 2025: AED 59B in Deals, 70% Off-Plan & Where Prices Are Really Moving

Investment Insights · 16 Nov 2025

Dubai sales stats October 2025: AED 59B in deals, 19,800+ transactions, 70% off-plan and rising rents. See which areas and property types…

Smart Investors Are Jumping from Canadian Real Estate to Dubai (Here’s Why)

Investment Insights · 14 Nov 2025

Discover why smart investors are jumping from Canadian real estate to Dubai for 7%+ rental yields, 0% tax, flexible plans and 10-year…

Why Dubai South Is on the Rise: Airport, Expo City & Smart ROI

Communities · 11 Nov 2025

Dubai South is rising fast — see why investors are eyeing the airport hub, Expo City, and 8 % yields under the 2040 Master Plan.

Most Affordable Areas to Buy in Dubai (2026 Guide)

Investment Insights · 9 Nov 2025

Most affordable places to buy in Dubai in 2026: compare prices, psf and yields; grab buyer checklists for International City, JVC, Dubai…

31 Above Dubai Maritime City: Waterfront Offices — Prices & Payment Plan

Projects · 7 Nov 2025

31 Above Dubai Maritime City: 116 waterfront offices from AED 3,400–3,500 psf. Prices, floor plates, payment plan, Q1 2029 handover.

How to Choose a Dubai Property Manager, a practical guide that actually helps

Investment Insights · 5 Nov 2025

To choose a reliable Dubai property manager, confirm a valid RERA license, check public reviews, I look for 4.5 stars or higher as a rule…

Dubai Rental Market 2025–2030: Trends, Yields & Smart Investment Insights

Market Reports · 5 Nov 2025

Dubai’s rental market 2025–2030: Balanced growth, steady yields, and key insights for investors, tenants, and landlords across top…

Dubai 2040 Master Plan Impact on Real Estate: Key Growth Areas & Investment Insights

Future & Innovation · 4 Nov 2025

Discover how the Dubai 2040 Master Plan will reshape real estate, boost property values, and create new investment opportunities across…

Le Blanc, Dubailand – A New Address in Dubai’s Fast-Growing Residential Corridor

Investment Insights · 2 Nov 2025

Discover Le Blanc in Dubailand — fully furnished off-plan apartments with flexible payment plans and 7–8 % projected rental yields.

Can Expats Get a Mortgage in Dubai?

Investment Insights · 29 Oct 2025

Yes, expats can get mortgages in Dubai with 20–30% down. Learn eligibility, LTV limits, and how to secure approval fast with Totality Real…

How Dubai Became the Most Liquid Property Market in the Middle East

Investment Insights · 23 Oct 2025

Discover why Dubai leads the Middle East in real estate liquidity — transparent laws, fast deals, and global investor confidence.

Address Harbour Point by Emaar - A Landmark of Luxury Living at the Tip of Dubai Creek Harbour’s Island District

Investment Insights · 18 Oct 2025

Discover why investors are choosing Address Harbour Point by Emaar. Luxury, location, and high ROI at Dubai Creek Harbour’s iconic…

Apartment for Rent in Peninsula, Business Bay

Investment Insights · 17 Oct 2025

Discover premium apartments for rent in Peninsula, Business Bay—modern living, Burj views, and prime Dubai investment potential.

DLD & RERA Roles Explained: A Practical Guide

Buying Guides · 15 Oct 2025

Clear guide to DLD vs RERA: titles, Oqood, escrow, Ejari, service charges, dispute routes, plus checklists and FAQs for buyers, sellers…

Apartments for Sale in Peninsula, Business Bay Dubai — Prices, Views & Buyer’s Guide

Buying Guides · 12 Oct 2025

Thinking of buying in Business Bay? Explore Peninsula Tower apartments—prices, layouts, Canal/Burj views, yields, and a step-by-step buyer…

Golden Visa Dubai: The Practical Guide for Investors, Talent & Families

Investment Insights · 11 Oct 2025

Golden Visa Dubai explained: eligibility, AED 2M property route, benefits, documents, fees & timelines. Step-by-step with official sources…

Apartments in Peninsula Tower, Business Bay (Dubai): a practical 2025 guide for buyers & renters

Projects · 8 Oct 2025

Apartments in Peninsula Tower, Business Bay: unit types, amenities, rent & yield math, plus an ROI calculator—your 2025 buyer & renter…

How Dubai Compares to London, New York, and Singapore

Investment Insights · 6 Oct 2025

Dubai vs London, New York & Singapore: higher yields, zero personal taxes on rent/gains, and a clear Golden Visa path. See pricing, nets,…

Dubai’s Most Exclusive Properties: Where Rarity Meets Remarkable Living

Investment Insights · 5 Oct 2025

Discover Dubai’s most exclusive homes—Palm, Emirates Hills, Jumeirah Bay, and more. See hotspots, brand residencies, and insider tips to…

Dubai Real Estate Market — September 2025 Deep Dive

Market Reports · 5 Oct 2025

Dubai real estate Sep 2025: 20,127 deals (+11.3% YoY), AED 54.3B (+21.2%), avg AED 1,689/sq ft; off-plan 74%. Top areas, yields, rents &…

Dubai Property Buying Process Step by Step

Buying Guides · 2 Oct 2025

Dubai property buying process, step by step—MoU, NOC, fees, mortgages, and title transfer. Practical tips to buy with confidence.

Freehold Areas in Dubai for Foreigners: The 2025 Guide

Investment Insights · 1 Oct 2025

Freehold areas in Dubai for foreigners: a 2025 guide to top districts, fees, mortgages, and off-plan vs ready—plus checklists and viewing…

Dubai Real Estate: October 2025 Outlook Events, Prices, Crypto & Practical Moves

Market Reports · 1 Oct 2025

Your Dubai real estate October 2025 brief: events, prices, yields, Golden Visa, and crypto payment pilots—actionable steps for smarter…

Al Marjan Island, Ras Al Khaimah: Buyer & Investor Guide

Market Reports · 29 Sept 2025

Al Marjan Island in Ras Al Khaimah—four coral-shaped islands, beach resorts, homes, and Wynn’s 2027 resort. Prices, lifestyle, access, and…

Top 13 Projects in Dubai (2025): What’s Real, What’s Next, and What’s Worth Your Time

Investment Insights · 26 Sept 2025

The most talked-about Dubai projects for 2025—icons, coastal living, and family communities—with timelines, buyer fits, and risk buffers.

Average Real Estate Cost in Dubai in 2025: A Practical Guide for Buyers & Investors.

Buying Guides · 26 Sept 2025

See 2025 Dubai property prices, yields, and fees. Area snapshots, price-per-ft² bands, and checklists to plan your next purchase.

Visa by Investment: Which Middle Eastern Property Markets Offer the Best Residency Incentives?

Legal Guides · 24 Sept 2025

From Dubai’s 10-year Golden Visa to Qatar, Saudi, and Bahrain’s programs, see which Middle Eastern property markets offer the strongest…

Property Investment Tour Dubai: A Real, On-the-Ground Guide 2025–2026

Investment Insights · 24 Sept 2025

See Dubai’s top investment districts with a guided, data-driven tour. Compare off-plan vs ready, understand yields, and explore Golden…

Dubai Property Market 2025: The Snapshot

Market Reports · 23 Sept 2025

Dubai real estate 2025 explained: what’s driving demand, where yields live, off-plan vs ready, and how to position if prices stabilize or…

Inside Dubai’s Luxury Property Boom: Where Global Capital is Flowing in 2025

Market Reports · 23 Sept 2025

From Palm Jumeirah villas to branded Downtown penthouses, Dubai’s luxury property boom is reshaping global investment trends. Discover the…

Dubai Off-Plan vs Ready Properties in 2026: Which Fits Your Timing, Yield, and Risk?

Buying Guides · 22 Sept 2025

Off-plan vs ready in Dubai for 2026: payment plans, yields, risks, and exit paths—clear tables, examples, and a simple decision flow.

Prime & Ultra‑Prime: Resilience or Repricing?

Market Reports · 21 Sept 2025

Ultra-prime villas on Palm and Jumeirah Bay show resilience, while mid-prime faces supply risks. Explore Knight Frank & Fitch forecasts.

Jumeirah Living Marina Gate: 2025, Data-First Reality Check

Projects · 20 Sept 2025

Data-first guide to JLMG in Dubai Marina—2025 prices, yields, fees, and comparisons. Book a private viewing with verified comps.

Dubai Real Estate Market Shape-Up (2025): Momentum, Maturity, and the Quiet Shift Toward Value

Investment Insights · 19 Sept 2025

Dubai real estate is maturing in 2025: rising prices, high liquidity, and “affordable luxury.” Get data-led picks, yields, and OPEX tips.

Dubai Real Estate Market Overview: August 2025

Market Reports · 18 Sept 2025

Dubai real estate hit AED 51.3B in August 2025 sales, with rising resales, strong mortgages, and steady price growth — solidifying its…

Supply, Delivery & Price Scenarios (2025–2028)

Market Reports · 16 Sept 2025

Dubai's property pipeline is shifting — slower handovers in 2025–26, major surge in 2027. Learn how timing and supply affect prices,…

Regulation & Visas: What US/UK Buyers Need to Know

Legal Guides · 15 Sept 2025

US and UK investors can qualify for Dubai’s 10-year Golden Visa with AED 2M+ property. Learn rules, equity requirements, and application…

Dubai Rent Prices & Yields 2026: A Cash-Flow Guide for Real-World Investors

Investment Insights · 14 Sept 2025

Planning to invest in Dubai rentals? See 2026 rent prices, yield ranges, net-of-costs math, and best areas to buy for steady cash flow and…

Dubai Islands to 2030, price forecast, yields, and the real risks investors should actually watch

Communities · 13 Sept 2025

Dubai Islands, formerly known as Deira Islands, is Nakheel’s big northern-coast swing, a five-island waterfront district that’s meant to…

Why Jumeirah Living Marina Gate Should Be at the Top of Your Dubai Real Estate Investment Wishlist

Projects · 12 Sept 2025

Discover why Jumeirah Living Marina Gate combines five-star service, premium location, and strong returns to stand out in Dubai’s property…

Jacob & Co Residences on Al Marjan Island: Ultra-Luxury With a Story and a Strategy

Projects · 11 Sept 2025

Jacob & Co Residences bring branded luxury to Al Marjan Island, with prime pricing, investor appeal, and a location set to benefit from…

Jumeirah Garden City: Market Overview and Development

Communities · 7 Sept 2025

Jumeirah Garden City is transforming into a central Dubai hub with new off-plan projects, competitive pricing, and strong long-term growth…

Al Marjan Island: The UAE’s Next Frontier for International Real Estate Investment

Future & Innovation · 3 Sept 2025

Al Marjan Island in Ras Al Khaimah is the UAE’s next hotspot for real estate. Early-entry pricing, Wynn Resort, and yields of 8–11% make…

The Top Townhouse Communities in Dubai: A Comprehensive Investment Guide

Communities · 1 Sept 2025

Discover the best townhouse communities in Dubai, from Arabian Ranches to Dubai Hills Estate, with pricing, features, and investment…

How to Sell Your Off-Plan Property in Dubai: A Comprehensive Guide

Buying Guides · 30 Aug 2025

Dubai’s off-plan market offers big resale potential. Discover how to price, market, and legally sell your property for strong ROI.

The Role of Architecture and Design in Dubai's Real Estate Appeal

Future & Innovation · 26 Aug 2025

From cultural heritage to futuristic skylines and sustainable smart cities, Dubai’s architecture makes it a global leader in real estate…

How to Finance Your Property Purchase in Dubai: Options and Tips

Buying Guides · 24 Aug 2025

From mortgages to developer plans, cash purchases, and Islamic financing. Discover the main options and smart tips to finance your Dubai…

The Impact of Global Economic Trends on Dubai's Real Estate Market

Market Reports · 22 Aug 2025

Dubai thrives amid global economic trends, offering investors stability, high yields, and safe-haven appeal despite shifts in trade,…

How to Choose the Right Real Estate Agent in Dubai

Buying Guides · 20 Aug 2025

Choosing the right real estate agent in Dubai is key to success. Learn how to find licensed, experienced, and transparent professionals…

How to Maximize Your ROI in Dubai's Real Estate Market

Investment Insights · 18 Aug 2025

Maximize your ROI in Dubai real estate with high yields, off-plan opportunities, rental strategies, and smart upgrades in one of the…

The Benefits of Owning a Property in Dubai

Investment Insights · 16 Aug 2025

From tax-free ownership to luxury living and strong ROI, discover why owning property in Dubai remains one of the smartest global…

Sustainable Living in Dubai: Eco-Friendly Properties and Their Benefits

Future & Innovation · 14 Aug 2025

From solar-powered homes to green mortgages, Dubai’s eco-friendly properties deliver lower bills, higher value, and align with global…

Therme Dubai: The World’s Tallest Wellbeing Resort Opening in 2028

Investment Insights · 12 Aug 2025

Therme Dubai sets a new standard for global wellness tourism, with thermal baths, spa care, fitness, and eco-living in the world’s tallest…

The Role of Technology in Dubai's Real Estate Market

Future & Innovation · 10 Aug 2025

Dubai leads in real estate innovation with AI, IoT, and digital platforms. Explore how technology drives transparency, growth, and…

Why Dubai is a Top Choice for International Real Estate Investors

Investment Insights · 8 Aug 2025

Dubai’s property market offers stability, global connectivity, and long-term growth. Explore why investors worldwide keep choosing Dubai…

Dubai's Commercial Real Estate: Opportunities and Insights

Investment Insights · 6 Aug 2025

Dubai leads the region in commercial real estate with strong demand, green buildings, and tech-driven projects. Discover key opportunities…

Legal Aspects of Buying Property in Dubai: What You Need to Know

Legal Guides · 4 Aug 2025

Buying property in Dubai? Learn the key legal aspects—freehold vs leasehold, registration, mortgages, and buyer protections to invest with…

Dubai's Real Estate Market is Booming: Key Factors

Investment Insights · 2 Aug 2025

Dubai’s real estate boom is driven by diversification, tax-free ownership, global demand, and world-class infrastructure—making it a top…

Dubai Real Estate Market Overview: July 2025

Market Reports · 1 Aug 2025

Dubai real estate hit AED 65B in July 2025, with record villa prices, strong rentals, and off-plan dominance driving investor confidence.

Investing in Dubai: The City's Most Promising Neighborhoods

Communities · 31 Jul 2025

From Downtown to Palm Jumeirah, discover Dubai’s most promising neighborhoods for real estate investment—luxury, strong yields, and…

How to Navigate the Dubai Real Estate Market as a First-Time Buyer

Buying Guides · 29 Jul 2025

First-time buying in Dubai? Learn how to navigate the market with confidence—covering locations, budgets, legal rules, and smart…

Dubai: The Ultimate Destination for Real Estate Investment

Investment Insights · 27 Jul 2025

Dubai real estate offers unmatched rental yields, zero taxes, and future-proof growth. Discover why the city remains a global investment…

In an Unstable World – Why is Investing in Dubai Real Estate a Safer Bet?

Investment Insights · 25 Jul 2025

In uncertain times, Dubai real estate offers rare stability, strong yields, zero taxes, and long-term growth—making it a smarter, safer…

Tracking ROI: How Dubai's Property Market Outpaces Regional Peers in Rental Yields

Market Reports · 24 Jul 2025

Dubai leads the Middle East in real estate ROI with top rental yields, low taxes, and strong demand. Discover why global investors keep…

Where Growth Concentrates Next: Dubai South, D33, and the 2040 Plan

Investment Insights · 23 Jul 2025

Dubai 2040 Plan and D33 agenda are reshaping real estate. Discover why Dubai South and airport expansion are key for long-term investors.

Dubai Real Estate Outlook: 2026 & Beyond (Investor Edition)

Market Reports · 21 Jul 2025

Explore Dubai’s 2026 property outlook—key trends, scenarios, and investor strategies shaping the market beyond speculation.

The Top 10 Luxury Property Neighborhoods in Dubai

Buying Guides · 18 Jul 2025

Explore Dubai’s top 10 luxury property neighborhoods, from Burj Khalifa to Palm Jumeirah. Discover high-end living, premium amenities, and…

Why Property Buyers Are Turning Their Attention to Al Marjan Island

Communities · 17 Jul 2025

Al Marjan Island in Ras Al Khaimah is emerging as a prime UAE investment hub with resorts, marinas & strong rental demand. Learn why now.

Dubai Real Estate Market Surges to Unprecedented Heights in Q2 2025

Investment Insights · 17 Jul 2025

Dubai real estate hits record AED 184.3B in Q2 2025 sales. Off-plan, luxury & mid-market thrive; strong investor demand drives growth. Ask…

The Step-by-Step Process of Buying Property in Dubai to Invest In

Buying Guides · 17 Jul 2025

Step-by-step guide to buying property in Dubai. Learn legal steps, fees, financing, visas & avoid mistakes. Ideal for international…

A New Path to Homeownership in Dubai: How the First-Time Buyer Initiative is Reshaping the City

Buying Guides · 15 Jul 2025

Discover Dubai’s First-Time Home Buyer Programme—making homeownership more accessible for residents with incentives, support, and policy…

Moving to Dubai - A Step-By-Step Guide

Legal Guides · 10 Jul 2025

A complete beginner’s guide to buying property in Dubai—visa tips, legal steps, and costs for foreign investors. Tax-free, safe, and easy…

UAE Unveils One‑Day Digital Mortgage Release and Central Bank Fee Reforms

Investment Insights · 6 Jul 2025

UAE speeds up mortgage release to 1 day, but new rules raise upfront costs as buyers can no longer include fees in home loan amounts.

Dubai Real Estate Market Overview: June 2025

Investment Insights · 4 Jul 2025

Dubai real estate hits AED 54.8B in June 2025 deals, with rising yields, villa prices, and crypto-backed sales fueling investor momentum.

Al Marjan Island: A Rising Investment Beacon in the Middle East

Investment Insights · 26 Jun 2025

Discover why Al Marjan Island in Ras Al Khaimah is emerging as the UAE's next real estate hotspot. Explore investment potential, risks,…

Common Mistakes to Avoid When Buying Property in Dubai

Buying Guides · 25 Jun 2025

Learn the top mistakes to avoid when buying property in Dubai. Get expert tips to protect your investment and make smart real estate…

What to Look for During a Property Viewing in Dubai

Buying Guides · 23 Jun 2025

What to Look for During a Property Viewing in Dubai: Full Checklist for Buyers & Investors | Totality Real Estate Guide

Al Marjan Island: The Next Investment Frontier in the UAE

Investment Insights · 21 Jun 2025

Al Marjan Island Investment Guide 2025: Real Estate, Wynn Casino, ROI Potential & UAE Freehold Opportunities for Foreign Investors in Ras…

Diversifying Your Real Estate Portfolio in Dubai: Where to Start

Investment Insights · 19 Jun 2025

Learn how to diversify your Dubai real estate portfolio across property types, locations, and market cycles to reduce risk and maximize…

Education in Dubai: A Comprehensive Guide for Families and Investors

Investment Insights · 18 Jun 2025

Discover how Dubai’s world-class education system boosts real estate investment. Explore schools, fees, top areas, and ROI in…

A Comprehensive Guide to Dubai Land Department (DLD) Charges and Their Impact on Real Estate Investment in the UAE

Investment Insights · 17 Jun 2025

Explore all Dubai Land Department (DLD) charges in this complete guide. Learn how fees impact property investment, ROI, and market…

Key Takeaways for Real Estate Investors

Investment Insights · 15 Jun 2025

Explore the best places to live in the UAE. Discover Dubai’s luxury market, top neighborhoods, investment benefits, tax perks, and…

Boom or Bust? Analyzing Dubai’s 2025 Real Estate Forecast

Market Reports · 13 Jun 2025

Dubai’s real estate market in 2025 shows strong fundamentals but rising complexity. Explore key trends, buyer shifts, pricing dynamics,…

Dubai Islands Real Estate: Price Trends, Potential, and Outlook 2025

Market Reports · 11 Jun 2025

Dubai Islands offers affordable luxury with off-plan prices rising in 2025. Discover why this emerging hotspot is redefining Dubai…

Why Canadians Are Turning to Dubai for Real Estate Investment

Investment Insights · 9 Jun 2025

For Canadian investors exploring global diversification: an overview of how Dubai's freehold market, regulation, and cross-border…

Dubai Real Estate Market Overview: May 2025

Market Reports · 6 Jun 2025

Dubai real estate hit AED 66.8B in May 2025, led by villa demand, off-plan sales, and crypto deals. Explore yields, trends, and what’s…

Top Reasons to Invest in Dubai Property in 2025: Insights for International Buyers

Investment Insights · 4 Jun 2025

Dubai real estate in 2025 is shifting toward smart, sustainable, human-centric development—reshaping how properties are built, valued, and…

Top 3 Investment Areas Favored by Totality Real Estate in 2025

Investment Insights · 2 Jun 2025

Discover the top 3 UAE investment hotspots for 2025—Dubai Islands, Jumeirah Gardens, and Al Marjan—offering high ROI, growth potential,…

Al Marjan Island: Your Gateway to Luxury Waterfront Living and Profitable Investments

Investment Insights · 27 May 2025

Al Marjan Island offers luxury waterfront living, strong rental yields, and major developments like Wynn, making it a top UAE investment…

The Most Luxurious Areas in Dubai: A Comprehensive Guide for Investors

Investment Insights · 19 May 2025

Explore Dubai’s most luxurious areas—from Palm Jumeirah to Emirates Hills. Discover top investment zones, yields, and elite living…

From Global Trends to Local Shifts: What’s Driving Dubai’s Property Market in 2025?

Market Reports · 15 May 2025

Discover how global trends—like inflation, remote work, and capital flight—are driving Dubai’s real estate boom in 2025. Learn where the…

Dubai Real Estate 2025: Navigating Growth, Trends, and Investor Opportunities

Market Reports · 12 May 2025

Explore Dubai real estate trends in 2025—from rising yields and smart homes to Golden Visas and top investment zones. Discover where…

The Dubai Rental Market in 2025: ROI Strategies and Shifting Tenant Demands

Investment Insights · 12 May 2025

Dubai’s 2025 rental market is evolving—discover ROI strategies, tenant trends, and top areas for long-term yield in a shifting investment…

Dubai Real Estate in 2025: A Global Investor’s Goldmine

Investment Insights · 10 May 2025

Dubai’s real estate market booms in 2025 with rising rents, 1,000 new residents daily & strong investor demand. Learn trends & key insights.

Dubai Real Estate Market Overview: April 2025

Market Reports · 5 May 2025

Dubai real estate hit AED 62.4B in April 2025—driven by off-plan sales, luxury demand, and crypto adoption. See why investors are rushing…

Dubai's Housing Demand Surges as Population Grows by 1,000 Daily

Market Reports · 17 Apr 2025

Dubai’s real estate market booms in 2025 with rising rents, 1,000 new residents daily & strong investor demand. Learn trends & key insights.

How to Invest in Dubai Real Estate Using Cryptocurrency: A Comprehensive Guide

Investment Insights · 16 Apr 2025

Learn how to buy Dubai real estate using crypto in 2025. Discover the benefits, risks, and exact steps for secure, blockchain-backed deals.

Dubai Real Estate in 2025: Is Now the Right Time to Invest?

Investment Insights · 14 Apr 2025

Dubai real estate in 2025 is booming—high returns, tax perks, and visa options make now a smart time to invest. Here’s why.

The 2025 UAE Golden Visa: Key Changes and What They Mean for You

Legal Guides · 11 Apr 2025

Golden Visa 2025: UAE eases rules for real estate investors, families & professionals—making long-term residency more accessible than…

Cryptocurrency Transactions in Dubai

Future & Innovation · 10 Apr 2025

Dubai Cryptocurrency Regulations 2025: Legal Framework, Tax Rules & Licensing Requirements for Crypto Transactions in the UAE

Dubai Real Estate Market Report: March 2025

Market Reports · 9 Apr 2025

Dubai’s real estate market surged in March 2025, with rising prices, high demand, and limited villa supply, reinforcing its global…

UAE Introduces Preferential Tax Regime In Bid to Lure Capital

Legal Guides · 8 Apr 2025

The UAE introduces corporate tax, DMTT, and incentives to boost R&D and high-value jobs, aligning with global standards and enhancing…

Investing in Dubai Real Estate: The Pain Points and How You Can Get Around Them

Investment Insights · 7 Apr 2025

Discover key challenges in Dubai's real estate market and learn how to overcome them with this essential investor checklist for smart,…

The Off-Plan Buying Process in Dubai

Buying Guides · 31 Mar 2025

Discover how to buy off-plan property in Dubai. Learn about payment plans, escrow, DLD waivers, risks, and strategies for smart investing.

Dubai Real Estate Market Overview: February 2025

Market Reports · 7 Mar 2025

Dubai's property market soared in Feb 2025 with rising prices, strong sales, and booming mortgages attracting global investors.

Dubai Rental Yields 2025–2026, A Practical Investor Guide

Dubai Rental Yields · 17 Feb 2025

Dubai rental yields, at least for now, sit in that rare space where the marketing line and the numbers actually line up. Most recent…

Dubai Real Estate Market Overview: January 2025

Market Reports · 31 Jan 2025

In January over 14,000 property sales were recorded - up 40% from the 10,000 transactions in January 2024.

Off-Plan vs. Ready Properties in Dubai: A Comparative Analysis

Investment Insights · 22 Jan 2025

Explore the key differences between off-plan & ready properties in Dubai. Compare prices, risks, returns & liquidity to make informed…

The Dubai Real Estate Market in December 2024

Market Reports · 31 Dec 2024

In December 2024, Dubai's real estate market continued its upward trajectory, reinforcing its status as a prime destination for investors.

Growth in the Dubai Real Estate Market in 2024

Market Reports · 30 Dec 2024

From improved roads and transport systems to new community developments, these projects are making the city even more appealing to buyers…

Why Investing in Dubai Real Estate is a Smart Move Based on 2024 Data

Investment Insights · 23 Dec 2024

Explore Dubai's booming real estate market with rising prices, high rental yields, diverse options, and tax-free benefits. Invest smartly…

Is 2025 a Good Year to Buy Property in Dubai? An In-Depth Market Analysis

Investment Insights · 20 Dec 2024

Explore why 2025 is the ideal year to invest in Dubai real estate. Discover growth trends, rental yields, prime areas, and lucrative…

The Dubai Land Department (DLD): A Key Pillar in Dubai’s Real Estate Market and Investor Appeal

Investment Insights · 16 Dec 2024

Discover why Dubai is a top destination for property investors worldwide. Learn about the Dubai Land Department’s role, tax-free benefits,…

A Comprehensive Guide to Buying Property in Dubai: Why Investors Worldwide Are Choosing The City

Investment Insights · 9 Dec 2024

Discover why Dubai is a top destination for real estate investors. Explore tax-free benefits, high rental yields, visa options, and prime…

Why Dubai is a Top Destination for Real Estate Investment: A Comprehensive Analysis

Investment Insights · 24 Nov 2024

Discover why Dubai is a global hotspot for real estate investment: tax-free environment, high rental yields, visa incentives, and…

Dubai Real Estate Market Overview: October 2024

Market Reports · 12 Nov 2024

Discover October 2024's best-selling real estate projects in Dubai, from high-value off-plan apartments and villas to ready-to-move homes.…

Flipping Properties in Dubai: Tips for Maximizing Profit

Investment Insights · 21 Oct 2024

Flipping properties in Dubai can be highly profitable if done strategically. Learn how to choose the right property, manage renovation…

Long-Term vs. Short-Term Rentals: Which is Better for Your Dubai Property?

Investment Insights · 19 Oct 2024

Discover the benefits and challenges of long-term vs short-term rentals in Dubai. Learn about income potential, management, and legal…

Dubai’s Freehold Property Laws (Foreign Ownership Guide for Investors)

Investment Insights · 18 Oct 2024

Dubai’s freehold property laws, primarily anchored in Law No. (7) of 2006 and the related designated-area rules, let foreign nationals and…

Dubai Real Estate Market Overview - September 2024

Market Reports · 15 Oct 2024

Explore Dubai's real estate market in September 2024 with 18,045 sales transactions, AED 44.6B total value, and 32.7% growth. Learn about…

Legal Requirements for Expats Buying Property in Dubai

Legal Guides · 6 Oct 2024

Discover the legal aspects of purchasing property in Dubai as an expat, including freehold vs. leasehold ownership, necessary documents,…

The Top 3 Benefits of Investing in Short-Term Rentals in Dubai

Investment Insights · 26 Sept 2024

Investing in short-term rentals in Dubai offers high returns, flexibility, and access to a growing market. Discover the benefits of…

Is Your Property Suitable for Short-Term Rentals in Dubai? A Comprehensive Guide for 2024

Investment Insights · 25 Sept 2024

Considering investing in short-term rentals in Dubai? Key factors like location, property type, legal compliance, and market demand are…

Affordable Property Hotspots in Dubai for 2024

Communities · 23 Sept 2024

Discover Dubai's top affordable property hotspots for 2024, including Dubai South, Dubailand, and JVC. Learn how strategic locations,…

Case Study: Investing in a Highly Profitable £118,000 Off-Plan Studio in Jumeirah Village Circle (JVC) with Flexible Payments

Investment Insights · 21 Sept 2024

Invest in a 40 sqm off-plan studio in Jumeirah Village Circle (JVC) for just £118,000 (AED 550,000) with a flexible 3-year payment plan.…

The Role of VARA in Regulating Digital Assets in Dubai

Future & Innovation · 19 Sept 2024

Dubai has established itself as a global leader in digital assets with the creation of the Virtual Assets Regulatory Authority (VARA).…

Understanding Dubai's Blockchain Strategy and Impact on Real Estate

Future & Innovation · 18 Sept 2024

Dubai's Blockchain Strategy, launched in 2016, is revolutionizing its real estate sector by enhancing transparency, security, and…

Top Free Zones in Dubai for Entrepreneurs: A Comprehensive Guide

Buying Guides · 17 Sept 2024

Dubai has become a global business hub, attracting entrepreneurs with its free zones offering tax exemptions, 100% foreign ownership, and…

5 Must-Know Factors for Investing in Off-Plan Villas for Sale in Dubai: Maximize Your Rental Yields Today

Investment Insights · 15 Sept 2024

Investing in off-plan villas in Dubai offers strong rental yields, flexible payment plans, and excellent ROI potential. Explore prime…

Comparing Dubai Real Estate Market Performance in August 2024: A Deep Dive into First-Sale and Off-Plan Transactions

Market Reports · 4 Sept 2024

Dubai’s real estate market continues to thrive, with August 2024 showcasing remarkable growth in first-sale and off-plan transactions.…

Exploring the Changes, in Dubai's Real Estate Market After Expo 2020

Investment Insights · 31 Aug 2024

Discover how Expo 2020 has reshaped Dubai's real estate market with new developments, shifting buyer demographics, and a focus on…

How Off-Plan Properties Compare to Ready Properties in Dubai

Investment Insights · 30 Aug 2024

Explore the key differences between off-plan and ready properties in Dubai's real estate market. Learn about pricing, customization,…

Dubai’s Best Luxury Off-Plan Developments for 2024

Projects · 29 Aug 2024

Explore Dubai's top luxury off-plan developments for 2024, offering prime locations, flexible payment plans, and high investment…

Dubai Property Market 2024: What Investors Need to Know

Investment Insights · 27 Aug 2024

Discover profitable opportunities in Dubai's real estate market for 2024. Stay updated on price trends, key sectors, and government…

Understanding Dubai Property Laws and Regulations

Legal Guides · 24 Aug 2024

Investing in Dubai's real estate market is gaining popularity among foreign investors because of the city's strong economic growth,…

Dubai Real Estate Market: Trends and Forecast for 2024

Market Reports · 23 Aug 2024

Discover Dubai's 2024 real estate trends and forecasts. Explore rising property prices, luxury demand, sustainable living, and government…

Comprehensive Guide to Dubai Real Estate Investment

Investment Insights · 22 Aug 2024

Explore Dubai's thriving real estate market in 2024. Learn about market trends, legal considerations, financing options, and strategies…

Dubai Real Estate Market Shines in July 2024: A Comprehensive Analysis

Market Reports · 20 Aug 2024

Dubai's real estate market saw impressive growth in July 2024 with a 45.5% increase in sales volume, reaching AED 50.1B. Apartment prices…

Sustainable Living: Eco-Friendly Villas and Green Communities in Dubai

Communities · 19 Aug 2024

Discover sustainable luxury living in Dubai's eco-friendly real estate developments. From green villas to energy-efficient communities,…

The Future of Dubai's Real Estate Market: Trends and Predictions for Off-Plan Properties

Market Reports · 24 Jul 2024

Explore the future of Dubai’s off-plan property market! Discover emerging trends, growing neighborhoods, and government policies shaping…

The Hottest Off-Plan Properties in Dubai for 2024: Top 5 Picks

Investment Insights · 8 Jul 2024

Discover Dubai's top off-plan properties for 2024, offering luxury living and high investment returns. From beachfront residences to golf…

The Most Sought-After Villa Communities in Dubai

Communities · 3 Jul 2024

A practical guide to Dubai’s top villa communities—Palm, Emirates Hills, JGE, Al Barari, Ranches, Dubai Hills—plus Oasis, Grand Polo, Palm…