Dubai South is rising fast — see why investors are eyeing the airport hub, Expo City, and 8 % yields under the 2040 Master Plan.

Dubai South is accelerating because it sits beside Al Maktoum International Airport (DWC) and Expo City—the city’s newest, sustainability-driven urban center. Massive airport expansion, the Route 2020 Metro to Expo, planned Etihad Rail passenger service, and new infrastructure spending are compounding benefits. Add free-zone advantages and relatively affordable entry prices, and you get a market with real rental yield potential and long-run appreciation—especially as Dubai’s 2040 plan concentrates growth around aviation and logistics hubs.

Quick note: I’ve walked this area more times than I can count—well, not literally every corner, but enough to notice the same pattern investors love: good bones now, bigger things loading.

Strategic location & connectivity

Next to a once-in-a-generation airport expansion

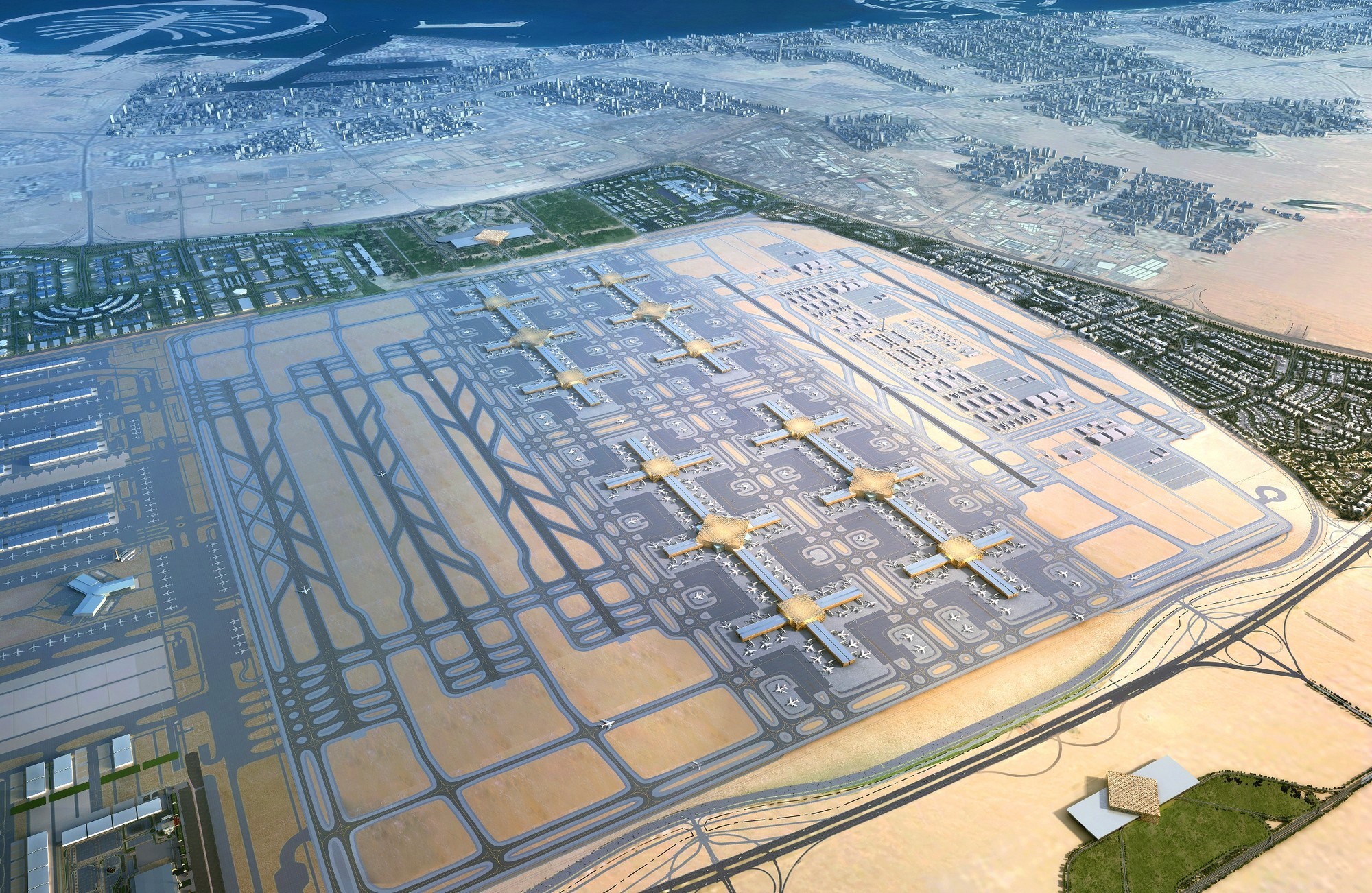

Dubai South borders Al Maktoum International Airport (DWC), the site of a Dhs 128 billion upgrade that will ultimately handle up to 260 million passengers and become the world’s largest airport by capacity. Officials have also indicated a staged migration of operations from DXB over the next decade. That scale—and the jobs and logistics that follow—tend to anchor housing demand in the surrounding districts.

Aviation’s role in Dubai’s economy is not theoretical; the emirate just posted record traffic through DXB and continues doubling down on aviation infrastructure as a growth engine—useful context when you’re underwriting five- to ten-year holds.

Expo City: from world expo to permanent 15-minute city

On Dubai South’s doorstep, Expo City has been repurposed as a sustainable mixed-use district (offices, residences, schools, R&D, retail). It brands itself “the new centre of Dubai’s future,” and—this matters—keeps the Expo legacy alive through an innovation-first master plan and a UAE-first Green Innovation District. If you believe in jobs-first demand, that’s your nucleus.

Metro now, national rail next

Dubai Metro (Route 2020): The Red Line extension already connects Dubai Marina/Sheikh Zayed Road to Expo City. Commute time is short and predictable—an underrated perk for tenants.

Etihad Rail (passenger): The UAE’s upcoming inter-emirate passenger service is tracking toward launch, with route plans showing a Dubai station near Jumeirah Golf Estates and a stop close to Al Maktoum Airport—a key adjacency for Dubai South workers and residents. Timelines evolve, but the direction of travel (literally) is clear.

Highways: Dubai South sits between Dubai and Abu Dhabi with direct access to Emirates Road (E611) and Sheikh Mohammed bin Zayed Road (E311). That “middle-corridor” geography keeps it relevant to cross-emirate commuters. (Drive times vary by hour; assume ±30–45 mins to Downtown in typical traffic.)

Resilience & citywide infra spend

Post-2024 storms, Dubai launched the Tasreef Dhs 30 billion rainwater drainage upgrade, with early phases focused on southern corridors including Expo/Jebel Ali/DWC—a helpful signal that the city is hardening infrastructure exactly where new growth is clustering. Investors sometimes overlook this, but resilience spending matters to long-term value.

Connectivity snapshot (indicative)

Link | Current Status | What it means for residents/investors |

|---|---|---|

Route 2020 Metro to Expo City | Operational | Predictable commutes; easier leasing to non-drivers |

Etihad Rail (passenger) | Announced / route revealed; phased rollout | Long-run, inter-emirate access; demand uplift near stations. |

DWC expansion | Approved; multi-year buildout | Jobs, logistics scale, air connectivity; structural demand driver. |

Tasreef drainage program | 2024–2033 | Citywide resilience; southern areas prioritized early. |

(Drive-time note: ~25–35 min to Dubai Marina, ~35–50 min to Downtown Dubai outside peak; always confirm at your viewing time.)

Economic & business advantages

Free-zone DNA (and why that matters for housing)

Dubai South and adjacent districts offer the classic UAE free-zone value stack: 100% foreign ownership, profit repatriation, customs/tax relief, and streamlined setup. Expo City itself markets flexible business hub packages and visas, drawing startups, SMEs, and corporate satellites. Talk to HR directors and you’ll hear a theme: when onboarding teams ramps up, nearby rentals fill up.

Jobs follow infrastructure; tenants follow jobs

Expo City’s shift from temporary event site to a permanent innovation campus (education, sustainability initiatives, R&D programs) supports stable white-collar employment on Dubai South’s doorstep. Pair that with the airport/logistics ecosystem, and you have a diversified tenant base—not just seasonal/short-term demand.

Investment potential: yields today, convexity tomorrow

No one can promise straight-line price growth—Fitch has even warned about a possible mid-cycle price correction as supply normalizes—but areas with low starting prices and big catalysts typically defend yields better in down years and compound faster in up cycles. Dubai South fits that playbook: affordable ticket sizes, improving transport, and institutional-grade anchors (airport, Expo City).

If you prefer imperfect honesty: yes, there can be construction views, dust, and occasional waits for retail to catch up. But that’s also where early-cycle returns usually live.

Residential growth & community fabric (what you feel on the ground)

You can already see the scaffolding of a complete neighborhood: new schools, parks, groceries, clinics, and mid-rise blocks that don’t try too hard. Multiple community guides point to affordability and space as the main attractions, with family-friendly public realm and pragmatic access to the city’s west and south corridors. It’s not Downtown Dubai—and that’s the point.

Where it stands against “brand-name” areas (quick take)

Price: Typically lower entry prices than Dubai Marina, Downtown, and even parts of Dubai Creek Harbour; that keeps gross yields competitive and widens your tenant pool. (Always check current AED/sqft per project.)

Quality of life: Quieter, greener, newer utilities; fewer bottlenecks; growing retail but not “complete” yet.

Volatility: Early-cycle districts can move faster—both ways. Smart underwriting uses conservative rent assumptions + a 3–4 year holding plan to let catalysts land.

Table: “Value vs. Convenience” (indicative, project-level due diligence required)

Factor | Dubai South | Dubai Marina | Downtown Dubai |

|---|---|---|---|

Typical entry price (1–2BR) | Lower | Higher | Higher |

Metro access | Route 2020 to Expo; buses | Red Line stations | Red Line stations |

Highway reach | E611/E311 | SZR | SZR/Al Khail |

Retail/amenities | Growing | Mature | Mature |

Yield profile | Often higher gross yields | Lower gross yields | Lower gross yields |

Who it suits | Value + growth investors; airport/Expo workers | Lifestyle/short-let | Professionals wanting center-city |

(We’ll add a price-per-sqft table by sub-community in the final pass; for now, this matrix keeps the strategy lens clear.)

Future-focused development: policy alignment means tailwinds

Dubai South sits neatly inside the Dubai 2040 Urban Master Plan, which concentrates growth around five urban centers and emphasizes transit-oriented, 20-minute-city living. Expo/Dubai South is a core node in that pattern, and you see it in everything from Metro/rail planning to citywide green and social infrastructure goals.

And while opinions differ on timing, the Etihad Rail network and broader mobility stack (integrations with Metro, buses, ride-hail) are being designed as a system—important for absorption beyond the first wave of buyers.

What this means for different buyer profiles (a quick, human read)

Yield-first buyers: Focus on 1–2BR units within walking/bus range of Expo Metro; favor layouts that rent easily (balconies, 1.5 baths).

Appreciation-first buyers: Track plots closest to future rail/airport interfaces; be early in phases with clear handover dates.

End-users with airport ties: Short commute, quieter blocks; check school runs and retail timelines honestly.

Short-let operators: Mind the STR licensing rules and seasonality; proximity to Expo events still matters.

Prices, Yields, Set-Up Notes, and Head-to-Head Comparisons

Pricing & yield snapshot (grounded, 2025 data)

I’ll keep this simple, then we can drill into sub-communities you care about.

Indicative averages (Q1–Q3 2025):

Area / Metric | Avg price psf (AED) | Notes on data | Typical gross yields* |

|---|---|---|---|

Dubai South (overall, a mix of projects) | ~1,019 | Q1-2025 resale report (apartments). | ~6–8% (project-dependent) |

Emaar South (sub-community within Dubai South) | ~1,437 (apartments) | Transaction analytics (rolling). | ~6.0–6.2% (2–3BRs avg.) |

Dubai Creek Harbour (benchmark, not adjacent) | ~2,388 (apartments) | Transaction analytics (rolling). | ~5–6% (mix) |

*Yields vary by bedroom mix, view, handover timing, and furnishing; see the caveats below.

Dubai South Q1-2025 resale average AED 1,019 psf (Totality Real Estate report)

Emaar South apartment ~AED 1,437 psf

Dubai Creek Harbour apartment ~AED 2,388 psf

For yields, Chestertons’ 2025 Emaar South guide pegs 2–3BR apartments ~6.2% gross; several brokerage round-ups show Dubai South ~6–8% depending on unit type; keep in mind asking vs achieved rents can differ.

As a tailwind, Hamptons’ March-2025 review flagged sharp YOY rent growth in Dubai South/Al Furjan on the back of infrastructure/metro effects.

Reality check: numbers move. Before you sign an SPA, we’ll pull fresh comps (last 90 days) and a rent roll for the exact stack/floor you’re targeting.

Why these numbers make sense (the “demand math” in a paragraph)

Airport expansion: DWC’s AED 128bn terminal program targets 150m+ pax in early phases, up to 260m later—plus five runways and ~400 gates. Jobs and logistics intensity tend to raise absorption in the immediate catchment.

Expo City as a permanent anchor: A free-zone, innovation-led, 15-minute city with school/work/retail and 180+ business services keeps weekday footfall local (and rents sticky).

Connectivity: Route 2020 Metro already runs to Expo; Etihad Rail (passenger) is advancing toward a Dubai alignment with proximity to DWC/Expo in the network plan—this is long-duration, but directionally potent.

Citywide resilience spend: The AED 30bn Tasreef drainage program focuses heavily on the southern corridor (Expo/Jebel Ali/DWC)—a quiet but meaningful risk reducer for investors.

Micro-map: Where the value clusters (quick take)

Walkable to Expo City / short bus-ride to Route-2020: Easiest to lease to non-drivers; studios/1BRs are the workhorses. (We’ll shortlist blocks with consistent 12-month occupancy.)

Golf-adjacent Emaar South (Urbana, Golf Views, etc.): Family renters; slightly higher psf, steadier tenant profiles; yields hold if you buy the right layouts.

South Bay / The Pulse corridors: Early-cycle pricing with community retail catching up; upside linked to DWC milestones.

Head-to-head: Dubai South vs Emaar South vs Dubai Creek Harbour

Factor | Dubai South (mixed) | Emaar South (inside Dubai South) | Dubai Creek Harbour |

|---|---|---|---|

Positioning | Value + growth near DWC/Expo | Master-planned, golf-adjacent, family-tilted | Premium waterfront, nearer to old CBD |

Avg apt. price/psf | ~AED 1,019 | ~AED 1,437 | ~AED 2,388 |

Tenant base | Aviation, logistics, Expo, SMEs | Families/expat professionals | Finance/creative sectors; mixed |

Transit | Route-2020 nearby; future rail | Same; car first, bus links | RTA road links; Metro at Creek stations |

Yield profile | 6–8% (by mix) | ~6% (2–3BR focus) | ~5–6% |

Risk | Construction cycles, retail lag | Lower volatility inside brand masterplan | Pricey entry; lower gross yields |

Sources: Pricing psf and yield references as above.

Free-zone & visa notes (for investors who want a base of operations)

If you plan to set up a business alongside property ownership (useful for visas and cash-flow ops), you have two adjacent free-zone options:

Dubai South Free Zone: 100% foreign ownership, streamlined licensing, visa services through Dubai South authority. (Corporate tax treatment depends on UAE FTA rules and whether income qualifies—get professional tax advice.)

Expo City Dubai Free Zone: Flexible business hub packages, freelance permits, short-term operation permits (1 day–12 months), and >180 services under the Expo City Dubai Authority.

(We can map license type ↔ visa quotas ↔ office size for you; Expo’s published guides are unusually clear.)

Risk & timing matrix (be picky on handovers)

Risk | What it looks like here | Mitigations |

|---|---|---|

Market cycle | Independent houses warn of a mid-cycle correction risk (Fitch floated ~-15% into 2026), especially as large new supply lands. | Favor rent-defensible units; model base rent -5% and extend your hold. |

Construction/retail lag | Patchy retail in pockets; dust and view changes during build-out. | Buy near existing schools/groceries; lock developer handover dates with penalties. |

Liquidity at exit | New supply can mute resale velocity. | Target sub-6% vacancy buildings and popular stacks; list with pro photos 60–90 days ahead. |

Speculative psf creep | Later phases can list too high vs comps. | Walk comps; insist on net-to-owner yield ≥ your hurdle at today’s rents. |

Transport timelines | National rail timing is phased. | Underwrite as option value; don’t rely on it to make a deal pencil. |

Unit-level checklist (so you don’t overpay for “new”)

Yield anatomy: Studios/1BRs near Route-2020 stations tend to lead gross yield; 2–3BRs in Emaar South often lead lease stability (Chestertons calls out 2–3BRs ~6%+).

Layouts: 1.5-bath 1BRs, balconies, and straight walls rent faster. Corner 2BRs with split bedrooms keep families.

Charges: Service-charge discipline matters in newer districts; verify AED/sqft and reserve-fund policy.

Noise/flight path: Check approach patterns to DWC as operations scale (protection zones exist, but do your evening site visit). Dubai Airports

Handover & snag: Demand snag report + defect liability timelines; in early cycles, a good PM saves your weekends.

Data table: today’s “value vs convenience” short-list (illustrative)

Sub-area | Why it’s on the radar | What to verify |

|---|---|---|

Expo-adjacent blocks | Walkability to Route-2020 station; weekday footfall. | Actual door-to-platform time; grocery/school distance. (RTA) |

Emaar South (Urbana, Golf Views, Parkside) | Brand, golf, family demand; mid-market rents; steady yields. | Latest psf vs. Bayut/Property Finder transactions. |

South Bay / The Pulse | Early pricing, lifestyle amenities planned. | Retail opening schedule; HOA budgets; service charges. |

Creek Harbour (benchmark) | Premium comp set; strong waterfront brand. | Psft premium vs. your yield target. |

Why this corridor has “optionality” (not just price)

Aviation anchor with clear, dated approvals (AED 128bn DWC program; 260m pax ultimate capacity).

Expo City permanence (free-zone, schools, R&D, campus feel).

Metro now; national rail later (treat as upside, not base case).

Resilience spend in precisely this catchment (Tasreef).

Additional Resources

Dubai 2040 Master Plan — Impact on Real Estate (why policy matters for Dubai South decisions).

https://totalityestates.com/blog/dubai-2040-master-plan-impact-on-real-estateOff-Plan in Dubai: Goldmine or Death Trap? (how to de-risk early-cycle buys).

https://totalityestates.com/blog/dubai-off-plan-properties-goldmine-or-death-trapDubai Property Manager: Compare Options (if you’ll lease units around DWC/Expo).

https://totalityestates.com/blog/dubai-property-managerHow Dubai Became the Most Liquid Property Market (exit strategy thinking).

https://totalityestates.com/blog/how-dubai-became-the-most-liquid-property-market-in-the-middle-east

Tiny caveat on tax: free-zones advertise attractive regimes, but UAE Corporate Tax rules apply at 0% only to qualifying income under FTA guidance; non-qualifying income can be taxed. Get bespoke advice before structuring.

The buying playbook (a bit obsessive, and very usable)

Step 1: Define your objective (and write it down).

Are you aiming for income (steady 6–8% gross in today’s conditions, give or take) or optionality (being early near an airport + innovation hub)? If you want both, fine—just rank them. It’s oddly helpful when you’re looking at two similar units and start second-guessing.

Step 2: Micro-map your commute and your tenant’s.

Walk from likely buildings to the Route 2020 station at Expo City (or your bus stop). Time it. Do it once in the heat. You’ll feel the difference between “marketable” and “actually easy.” End-users should also drive the school run at 7:30 a.m., not 11 a.m.

Step 3: Pull fresh comps, not headlines.

Ask for the last 90 days of transactions (same bed/bath, similar view/floor). If there aren’t enough, widen by ±10% in size and normalize to AED/psf. For rents, favor achieved leases over ambitious listings. The point isn’t to be perfect; it’s to be anchored.

Step 4: Underwrite with three numbers (and nothing cute).

Service charges: request the latest AED/psf and the reserve-fund policy.

Net-to-owner yield: model base rent -5%, vacancy 5–8%, and charges as quoted +10% buffer.

Exit liquidity: assume you’ll need 60–90 days to find the right buyer/tenant, then be pleasantly surprised if it’s faster.

Step 5: Choose the right layouts.

Investor lens: Studios and 1BR with 1.5 baths + balcony near transit generally lease fastest.

Family lens: 2BR split-bedroom plans in Emaar South with a clean rectangular living room and decent storage.

Avoid overly “creative” angles and deep interior bedrooms away from daylight.

Step 6: Handover timing and snagging.

If off-plan, get milestone schedules, longstop dates, and delay penalties in writing. On handover, hire a snagging company; ask for the defect liability period and escalation flow (developer → facilities → authority).

Step 7: Financing & fees (quick).

DLD transfer fee: commonly 4% (off-plan Oqood registration also ~4%; some developers offer partial rebates—read the fine print).

Mortgage? Factor valuation fees, processing, early-settlement rules. If you’ll rent, test DSCR with conservative rent.

STR vs long-let: check community bylaws and permit rules before you assume short-term is allowed (or wise).

Step 8: Property management (don’t be a hero).

Ask for SLA (response times), lease-up KPIs, and a fee schedule free of mystery “admin” lines. A good PM in a new district is worth more than clever Excel.

Imperfect truth: in growth corridors, your biggest edge is not a secret deal—it’s an honest model and the discipline to walk away when the numbers don’t clear your hurdle.

Short-term rental (STR) vs long-let: the back-of-napkin math

Illustrative only; plug your own numbers before acting.

Metric | STR (airport/Expo-adjacent 1BR) | Long-let (same unit) |

|---|---|---|

Assumed ADR | AED 350 | — |

Occupancy | 68% | — |

Gross monthly | ~AED 7,140 | AED 6,000 (annual lease ~72,000) |

Platform/PM fees | 20% (~1,428) | PM 5–7% (~350–420) |

Utilities/linen/etc. | AED 600 | Tenant-paid (usually) |

Service charges (alloc.) | AED 500 | AED 500 |

Net to owner (est.) | ~AED 4,612 | ~AED 5,080–5,150 |

Read: STR can outperform in event-heavy months, but it’s work. In steady periods, a clean long-let often wins on stress-free net. If you do STR, price in a true ops cost and the permit steps; if you do long-let, invest in durable furniture (or none) and better photos.

1BR vs 2BR: which travels better through cycles?

Lens | 1BR near Route 2020 | 2BR in Emaar South |

|---|---|---|

Tenant pool | Singles/couples, aviation staff, Expo/SME hires | Families, long-tenure professionals |

Yield tendency | Higher gross (faster lease-up) | Slightly lower gross, steadier net |

Void risk | Lower between March–Nov; watch summer | Low if priced right; some seasonality ignored |

Resale liquidity | Strong under AED 1.2m | Good if view/stack is right |

Who should buy | Income-first investors | End-users, stability-focused investors |

End-user vs investor: decision table

Question | If you answer “Yes” | Likely fit |

|---|---|---|

Is a short commute to DWC/Expo your #1 driver? | Yes | Expo-adjacent 1–2BR, walkable to bus/Metro |

Do you want schools and golf nearby? | Yes | Emaar South 2–3BR townhomes/apartments |

Is maximizing gross yield your main KPI? | Yes | Compact 1BR/large studio near transit |

Do you dislike construction views? | Yes | Pick delivered phases with mature landscaping |

Will you self-manage STR? | Yes | Budget real ops time or pick a pro operator |

Two quick buyer personas (because real life is messy)

The Aviation Couple

They both work shifts at DWC, hate driving. They’ll pay a small premium for a 10–15 minute door-to-platform commute and decent gym. They renew if noise is low and Wi-Fi is strong. Your winning unit? A 1BR with a balcony in a building that keeps its common areas spotless.The Remote-Work Family

One parent travels, one works from home. They want a 2BR with separate study nook near a school and green space. They’ll accept a longer drive to Downtown if weekends feel quiet. For them, Emaar South layouts with functional kitchens and storage simply… work.

On timing (a candid paragraph)

If you’re buying for 2025–2030, you’re buying into infrastructure, not after it. Prices can wobble while roads, rail, and retail mature. That’s normal. The risk isn’t that progress takes time; it’s paying a future price today. So, keep your bid tethered to today’s rent and the closest comps—and let the upside of DWC/Expo accrue as a bonus, not a requirement.

FAQs (practical, slightly informal)

Q1. Is Dubai South only interesting because of the airport?

Not only. The Expo City free-zone and the broader southern corridor investments make it more than a single-asset story. The airport is the spine; the jobs and schools are the muscles.

Q2. What’s a realistic gross yield for a 1BR near Expo today?

Case by case, but 6–8% gross is a common range if you buy right and keep costs in line. Always model a conservative rent and a small vacancy allowance.

Q3. Are service charges high in newer buildings?

They can be, which is why you ask for the latest budget and any reserve-fund details. A well-run building with attentive FM often justifies a slightly higher charge.

Q4. Does Etihad Rail timing matter to my buy decision?

Treat it as option value. Great if it lands sooner; your deal should still work without it.

Q5. Is short-term rental permitted everywhere there?

No. Check community bylaws and the latest STR permit rules before planning an Airbnb strategy.

Q6. What floors or stacks rent best?

Middle floors with pleasant, open views and balanced light. Super low floors next to construction can sit, and ultra-high floors with weird layouts sometimes underperform.

Q7. End-user here: will I feel “far” from the city?

Some days, yes. Other days, the lack of congestion feels like a small luxury. Metro + highways help; just be honest about your lifestyle.

Q8. Are developers offering fee rebates?

Occasionally—part DLD coverage, payment plans, or furnishing packs. Read every clause and compare the all-in.

Q9. Townhouse or apartment for long-term value?

Townhouses suit families and can hold value well; apartments close to transit usually win on liquidity.

Q10. What’s one mistake to avoid?

Basing your price on future connectivity rather than present rents and actual comps.

Developer & community roll-up (quick reference you can actually use)

This is the bit you (or we) can keep fresh monthly. It isn’t meant to be pretty; it’s meant to be useful.

Community / Cluster | Primary Developer / Authority | Typical Product | Positioning in One Line | Notable Hooks | Notes to Verify Each Month |

|---|---|---|---|---|---|

Emaar South (Urbana, Golf Views, Parkside…) | Emaar | Apts, townhomes | Family-tilted, golf-adjacent, steady demand | Brand pull, planned environment | Update avg psf, 1BR/2BR rent bands, service-charge ranges, new handovers |

South Bay (Dubai South) | Dubai South | Villas, townhouses, lagoon-centric | Early cycle + lifestyle amenities | Large masterplan depth | Track construction phases, retail openings, HOA budgets |

The Pulse / The Pulse Beachfront | Dubai South | Apts, townhouses | Value + improving amenity base | Expo/DWC proximity | Watch transit connectivity and retail occupancy percentages |

Expo City Residential (adjacent) | Expo City Dubai Authority | Apts, mixed-use | Innovation campus, 15-min city vibe | Route 2020 access, free-zone gravity | Verify permit/STR rules and school/clinic onboarding |

Logistics/Industrial Fringe (edges) | Mixed | Worker housing, value apts | Yield-first, more utilitarian | Employer demand | Check tenant profile shifts and void risk seasonality |

Note: on paper, these all look “close.” On a hot August afternoon, the ones within a true 10–15 minute door-to-platform of the Route 2020 station just feel easier to live in.

Mini price/psf & rent grid (built to be updated monthly)

Use this as your “at-a-glance” block. Keep the ranges honest; don’t force precision where it doesn’t exist yet. Numbers below are left blank by design—drop in last-90-day medians before publishing and refresh monthly.

Sub-area | Avg Sale psf (AED) | 1BR Monthly Rent (AED) | 2BR Monthly Rent (AED) | Indicative Gross Yield | Quick Take |

|---|---|---|---|---|---|

Emaar South (Apts) | [____] | [____] | [____] | [____]% | Family demand; steady lease-ups; brand premium |

Emaar South (THs) | [____] | — | — | [____]% (annualized) | End-user and long-hold investors; yard space sells itself |

The Pulse (Apts) | [____] | [____] | [____] | [____]% | Value + improving amenities; watch service charges |

South Bay (Villas/THs) | [____] | — | — | [____]% (annualized) | Lifestyle play; verify lagoon/phase timelines |

Expo City (Apts) | [____] | [____] | [____] | [____]% | Campus feel + Metro; check bylaws for STR |

Benchmark: Dubai Creek Harbour (Apts) | [____] | [____] | [____] | [____]% | Premium comp; lower gross, higher liquidity |

How to refresh this in 20 minutes, monthly:

Pull last-90-day transactions (same bed, ±10% size) → compute medians in AED/psf.

Cross-check asking vs achieved rents (talk to 2–3 managers).

Re-run yields on net-to-owner math (not brochure gloss).

Annotate anomalies (bulk deals, incentive-loaded SPAs).

Re-read any handover or infrastructure milestone that actually happened.

If you want, I can package this as a tiny Google-Sheet template with conditional formatting and a yield slider. (It makes the monthly refresh weirdly satisfying.)

For investors who want numbers now

Start Your Property Search → https://totalityestates.com/

Dubai Off-Plan: Goldmine or Death Trap? → https://totalityestates.com/blog/dubai-off-plan-properties-goldmine-or-death-trap

How Dubai Became the Most Liquid Market → https://totalityestates.com/blog/how-dubai-became-the-most-liquid-property-market-in-the-middle-east

Book a Consultation → (Use your /contact or Calendly URL here)

Block B — For landlords and end-users

Dubai Property Manager: Compare Options → https://totalityestates.com/blog/dubai-property-manager

Dubai 2040 Master Plan — Impact → https://totalityestates.com/blog/dubai-2040-master-plan-impact-on-real-estate

Buyer Upfront Costs & Fees → (Link to your calculator/article)

Register Your Interest (Dubai South) → (Landing page for this article’s CTA)

Tiny persuasion tip: mirror the reader’s intent in the button text. “Get My Yield Plan” converts better than “Submit.”

Conclusion

Dubai South is rising for reasons that don’t depend on hype: an airport expansion measured in runways and gates (not adjectives), a recycled world expo turned living district, and a city plan that keeps pushing jobs and infrastructure south and west. Is it perfect today? No. Some corners still feel unfinished; some views still look at cranes. And yet—this is how many of Dubai’s best stories started.

If you buy here, buy for what it is now (rents, commutes, schools), with the humility to treat future rail as bonus, not baseline. Keep your underwriting dull, your photos excellent, and your service-charge questions sharp. Do those unglamorous steps and you’ll give yourself room for the upside to arrive on its own schedule.

Yield-first:

Turn capital into cash flow. Get a 15-minute Dubai South yield plan (3 comps, today’s rent, net-to-owner math). [Book a free consultation →]