Jacob & Co Residences bring branded luxury to Al Marjan Island, with prime pricing, investor appeal, and a location set to benefit from Wynn Resort’s arrival.

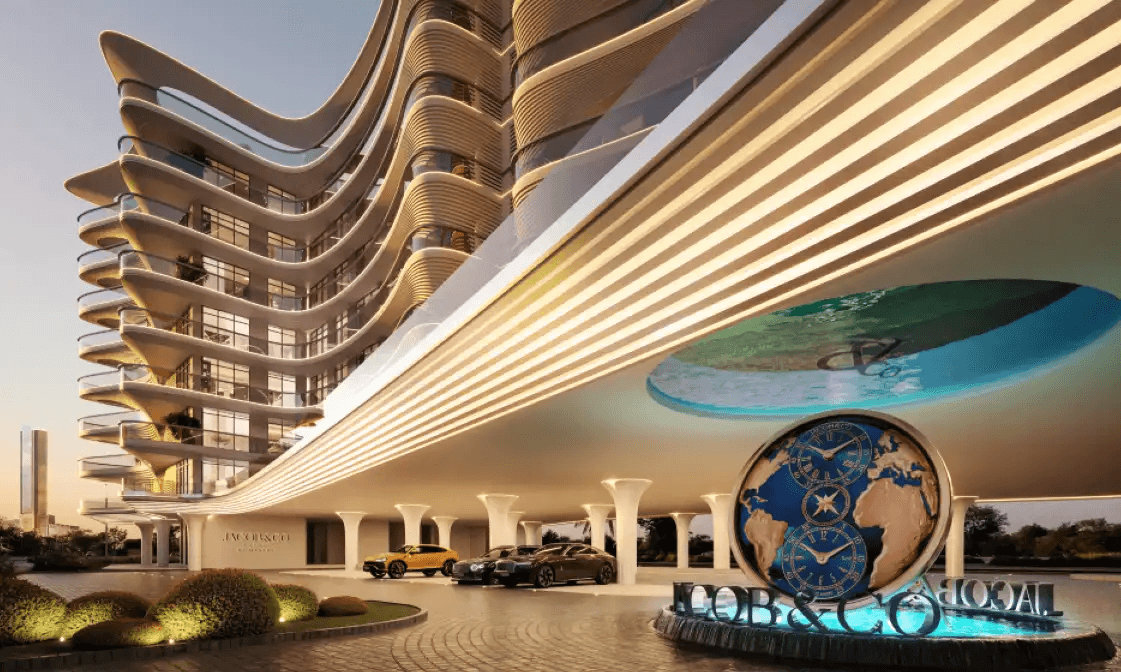

If you’ve watched Al Marjan Island quietly (well, not that quietly) evolve from a sun-splashed retreat into a branded-residence hotspot, this next move makes sense. In July 2025, Mantra Properties—an India-born developer known for design-led residential projects—announced a collaboration with the haute horology and jewellery house Jacob & Co. to bring Jacob & Co Residences to Ras Al Khaimah’s flagship island. The project is reportedly valued around AED 400 million and targets discerning end-users and investors who want something rarer than “beachfront.” They want narrative. A signature. Perhaps a little theatre.

Is that over-claiming? I don’t think so. Jacob & Co’s design vocabulary—precision, sparkle, an almost cinematic sense of detail—translates naturally into branded living. Early coverage confirms Mantra’s UAE debut and the brand’s first residential foray on Al Marjan, with launch news circulating mid-July 2025.

The gist so far: 1–2 (potentially 1–3) bedroom apartments oriented to sea views, high-end finishes, and access to amenities like a spa and beach club. Delivery? Targets have been discussed in the 2027–2028 window—final dates to be confirmed as the developer formalizes sales packs and construction milestones. Some third-party listings speculate Q2 2028; others position Q3 2027 as an initial target—reasonable, yet still indicative. We’ll treat handover timing as a range until official sales materials are published.

Why Al Marjan, why now?

Two words (well, one name): Wynn. The integrated resort—licensed for commercial gaming under the UAE’s national regulator—has a publicly stated opening trajectory in early 2027. This is not a minor catalyst; it’s a gravitational one. The Wynn Al Marjan Island project has continued to publish progress updates and positioning, including new ultraluxe components like Enclave. For RAK—and for branded residences within walking or short-drive proximity—this is the event that bends demand curves.

Personally, I think that matters even more for resale depth than for nightly STR rates (short-term rentals). Yes, tourism will spike around openings; yes, premium ADRs will materialize in pockets. But the enduring impact tends to be market narrative: more international eyeballs, more confidence, more anchor-brand gravity.

Positioning in a crowded (but exciting) branded market

Jacob & Co Residences arrives beside serious company. JW Marriott Residences Al Marjan is far along and widely marketed with a 70/30 plan and handover positioned for late 2027 (some portals previously framed Q4 2026; a number of official channels and sales partners now communicate end-2027). Ellington’s Costa Mare is also drawing attention, with starting prices for 1–3BRs referenced across portals and resales. Both set useful comparables for pricing bands and per-sq-ft logic.

Let’s be practical here. On Costa Mare, current asks (resale/primary mix) show a very wide range—from around AED 1.3M into the multi-million bracket depending on layout, view, and tower. Marketing pages often cite starting points in the AED 2.3M–5.5M+ range for 1–3BR. JW Marriott Residences commonly appears with from ~AED 2.75M (1BR) and a structured 70/30, with keys aligned to the broader 2027 Wynn calendar. It’s not hard to see where a Jacob & Co flagship could slot: upper tier of these brackets, likely commanding premiums for signature interiors, limited stacks, and front-row views—assuming the spec sheet is as curated as the brand suggests.

A candid note on branded premiums (and what to verify)

Branded residences are not all created equal. Some are deeply integrated—design standards, operating protocols, resident privileges—while others lean… logo-forward. The difference shows up in resale, service charges, and long-term owner satisfaction. If you’re considering Jacob & Co Residences, don’t just admire the renders. Press for specifics in the SPA: brand standards, use of trademarks in resales, FF&E specifications, after-sales support, and any owner benefits beyond the usual gym/spa. It’s a small extra step that often pays large dividends over a 5–7 year hold.

Online chatter in the region (forums, subreddits) has been increasingly sophisticated on this topic—friendly, but skeptical about “sticker” premiums that aren’t grounded in tangible resident benefits. It’s healthy skepticism. Use it.

Quick snapshot: where Jacob & Co could sit versus immediate peers

Project | Developer / Brand | Stated Handover* | Indicative Entry Prices** | Payment Plan (typical) | Notes |

|---|---|---|---|---|---|

Jacob & Co Residences | Mantra x Jacob & Co | 2027–2028 (to be finalized) | Upper-tier vs island peers | TBA | Signature branded positioning; first Jacob & Co residences on Al Marjan; Mantra’s UAE debut. |

JW Marriott Residences | WOW Resorts x JW Marriott | Q4 2027 guidance on key channels | From ~AED 2.75M (1BR, portal data) | 70/30 | 524 turnkey units; aligns to Wynn calendar; widely marketed. |

Costa Mare | Ellington | Q4 2028 (marketing pages) | 1BR from ~AED 2.3M; wide ask band active | 70/30 (varies) | Private beach positioning; multiple towers; asks vary sharply by view/stack. |

* Handovers and payment plans are developer/contract dependent. Verify in the SPA and latest release.

** Portal starting prices fluctuate with releases, floors, views, and resale inventory.

Investor lens: what’s realistic vs. what’s aspirational

It’s tempting to extrapolate a 6–8% gross yield just because “beachfront + Wynn.” In practice, hitting 5%+ on a AED 2M–3M purchase requires consistent high ADRs and occupancy, plus tight cost control (furnishing, utilities, operator fees, community charges). Some public threads have questioned whether the nightly rates assumed in broker decks are achievable year-round. Personally, I’d budget conservatively for Year-1/2 and re-rate after Wynn’s first high season—there’s often a calibration period. (We’ll run example math in the next section of this article—with conservative, base, and stretch cases.)

That said, the strategic bet here may be total return rather than yield alone: moderate income + brand-supported capital preservation (or growth) as the island’s ecosystem matures.

Design promise: Jacob & Co’s signature

The most compelling path for this project, in my view, is if Jacob & Co leans fully into its design DNA—geometric motifs, jewel-like lighting, tactile materials—so the residences feel like limited works, not interchangeable beachfront stock. Early coverage emphasizes a “fusion of haute horology with high-end real estate.” If that translates into honest materiality and distinctive public spaces (lobbies, lounges, spa), then premiums start to make sense.

Helpful Navigation

Al Marjan Island - Ras Al Khaimah (RAK)

Al Marjan Island, Ras Al Khaimah: Buyer & Investor Guide

Neighbourhood catalysts you should track

Wynn timeline: Keep an eye on construction markers and brand announcements (suite concepts, F&B partnerships). The GCGRA licensing backdrop and “early 2027” opening communications have been reiterated across official and media sources. This is the demand engine.

Competing supply: New towers across Al Marjan—some launching with aggressive price-per-sq-ft and glossy amenities. Oversupply is often cited anecdotally; the nuance is absorption vs deliveries around the Wynn opening and the 12–24 months following. (We’ll map a supply-timeline view later in this piece.)

Micro-checks before you reserve

I’ll admit, I’m cautious by nature, but on branded projects I get especially picky:

View corridors & stack logic: A “sea view” can mean many things. Stand in the exact stack line if possible; check for lateral obstructions and adjacent phase massings.

Service-charge estimates: Branded finishes often come with premium OPEX. Good to model a range.

Operator alignment: Who runs what—and how does the brand audit standards over time?

Resale practicality: Any restrictions on using the brand mark in your listing? Are there onboarding/transfer fees that spook second-buyers?

Payment calendar: Match your cash-flow to realistic construction cadence. 70/30 and 60/40 plans look tidy on slides; your bank account cares about dates.

Competitor intel at a glance (source-based notes)

JW Marriott Residences: Multiple channels currently show 70/30 with handover late 2027, in tune with the Wynn drumbeat. Several sales partners emphasize resort adjacency and turnkey delivery.

Costa Mare (Ellington): Marketing pages and portals reference 1BR from ~AED 2.3M and a 70/30 plan, with Q4 2028 handover guidance in some materials; live asks on portals range widely due to resales and premium stacks.

Suggested images to include (ready for your design team)

(These are concept prompts you—or your designer—can use to generate visuals or brief a 3D artist. I can also output them as production-ready image files if you want.)

Hero Concept: “Twilight view of a glass-and-stone beachfront residential tower on Al Marjan Island, subtle jewel-inspired façade lighting, calm Arabian Gulf, boardwalk palm silhouettes, understated luxury mood.”

Design Detail: “Close-up of a lobby vignette with gem-cut chandelier, polished marble, brushed metal accents, and a watch-mechanism motif subtly integrated into wall panelling.”

Market Context Map: “Minimalist map graphic of Al Marjan’s four islets, pinpoints for Jacob & Co Residences, JW Marriott Residences, and Wynn Al Marjan, with walking-time annotations.”

Competitor references (for readers who want source trails)

BeRightProperties overview (project page; handover note, unit ranges, highlights).

Al Marjan Island properties portal entries for Costa Mare (live ask ranges).

Ellington Costa Mare marketing page (starting prices, 70/30, handover Q4 2028).

JW Marriott Residences payment/handover comms (70/30; 2027 timing on key channels).

Wynn Al Marjan official and media updates (early 2027 opening; GCGRA licensing context).

Numbers That Matter: ROI Scenarios You Can Actually Sanity-Check

It’s easy to talk “Wynn halo” and forget the spreadsheet. Let’s keep it grounded with three yield scenarios for a notional 1-bed residence at AED 2,600,000 plus AED 100,000 for furnishing (total cost basis AED 2,700,000). Feel free to swap in your own rates and occupancy later.

Fixed annual cost placeholder (service charges, utilities, maintenance, insurance): AED 49,000 conservative/base; AED 55,000 stretch. This is illustrative; always verify with the latest community/OPEX guidance.

Conservative Case

Average nightly rate (ADR): AED 900

Occupancy: 55% (≈ 201 nights/year)

Gross rental revenue: AED 180,900 (= 900 × 201)

Management/Platform (20%): AED 36,180

Net before fixed costs: AED 144,720

Fixed costs: AED 49,000

Net Operating Income (NOI): AED 95,720

Yield on total basis (AED 2.7M): ≈ 3.55%

Base Case

ADR: AED 1,200

Occupancy: 62% (≈ 226 nights/year)

Gross rental revenue: AED 271,200

Management/Platform (20%): AED 54,240

Net before fixed costs: AED 216,960

Fixed costs: AED 49,000

NOI: AED 167,960

Yield on AED 2.7M: ≈ 6.22%

Stretch Case

ADR: AED 1,500

Occupancy: 70% (≈ 255 nights/year)

Gross rental revenue: AED 382,500

Management/Platform (20%): AED 76,500

Net before fixed costs: AED 306,000

Fixed costs: AED 55,000

NOI: AED 251,000

Yield on AED 2.7M: ≈ 9.30%

Takeaway: the “headline” 8–9% yields are doable but depend on sustained premium ADRs and occupancy after Wynn’s opening cadence settles. A pragmatic investor underwrites nearer 5–6% and lets upside surprise them.

Price-Per-Square-Foot (psf): Where Might Jacob & Co Land?

Sizes vary by stack and view, so think in bands, not absolutes. Here’s an illustrative comparison using typical 1BR footprints to sense-check positioning (verify against official floor plans and release sheets at reservation):

Scheme | Illustrative Size (1BR) | Illustrative Entry (AED) | Back-of-Envelope psf (AED) | Notes |

|---|---|---|---|---|

Jacob & Co Residences | 900 sq ft | 2,600,000 | ≈ 2,889 | Branded spec & limited stacks could push higher for prime sea-front lines. |

JW Marriott Residences | 950 sq ft | 2,750,000 | ≈ 2,895 | Broad, globally trusted flag; turnkey emphasis. |

Costa Mare (Ellington) | 850 sq ft | 2,300,000 | ≈ 2,706 | Private-beach, design-led; wide ask range by tower/view. |

I’m deliberately conservative on Jacob & Co’s psf; signature interiors and first-row views can (and often do) push the top stacks above the median.

Payment-Plan Stress Test (Cash-Flow in Plain Sight)

Many island launches present 70/30 (70% during construction; 30% on handover). For a AED 2,600,000 ticket:

Total 70% during construction: AED 1,820,000

30% on handover: AED 780,000

One workable cadence (illustrative, not contractual):

Milestone | % of Price | Amount (AED) | Running Total (AED) | Comment |

|---|---|---|---|---|

Booking (Launch Month) | 10% | 260,000 | 260,000 | Reservation + SPA processing |

6 months | 10% | 260,000 | 520,000 | Construction progress #1 |

12 months | 10% | 260,000 | 780,000 | Progress #2 |

18 months | 10% | 260,000 | 1,040,000 | Progress #3 |

24 months | 10% | 260,000 | 1,300,000 | Progress #4 |

30 months | 10% | 260,000 | 1,560,000 | Progress #5 |

36 months | 10% | 260,000 | 1,820,000 | Progress #6 (completes the 70%) |

Handover (Keys) | 30% | 780,000 | 2,600,000 | Final settlement + title |

Why this matters:

You can map these dates to expected income events (bonuses, asset maturities) and FX hedges if your base currency isn’t AED.

If handover is aligned with a Wynn high season, you may prefer immediate STR deployment. If it’s shoulder season, consider a short corporate let until winter ramps up.

End-User vs Investor: Two Different Purchase Logics

End-User / Second-Home

You’ll likely pay a premium for exact view/stacks, finishes, and a calmer floor plate.

Service charges matter less than daily lived experience: lobby design, spa quality, private club atmosphere, discreet valet.

Yield-Oriented Investor

You’re underwriting pricing power (view, layout efficiency) and OPEX predictability.

You’ll scrutinize brand entitlements in the SPA and resale practicalities (use of marks in listings, onboarding/transfer steps for a buyer).

Both profiles benefit from the Wynn gravitational pull—but in different ways: end-users get a richer ecosystem; investors get broader demand depth and, potentially, better resale velocity.

Due-Diligence Checklist (Save This Before You Wire a Reservation Fee)

Exact Stack & Corridor – Confirm sightlines today and any planned massings adjacent.

Handover Window – Treat dates as ranges; request delay clauses and remedies in writing.

Service-Charge Estimate – Model a range and stress test.

Brand Integration – List what’s brand-audited post-handover (not just during marketing).

Resale Mechanics – Use of brand name in ads; transfer fees; pre-approval steps.

Furnishing Scope – What’s included vs optional FF&E packages? Warranty terms?

STR/Corporate Let Rules – Operator approvals, minimum night rules, key-card policies.

Payment Calendar – Get the exact dates; align with personal cash flow.

Snagging Standards – Acceptance criteria, rectification timelines, escrow release triggers.

Exit Plan – If your thesis is capital appreciation around Wynn’s first two seasons, what’s Plan B if supply runs hot?

One More Friction-Removing Table: “Who Should Buy What?”

Buyer Profile | What to Prioritize | What to Down-Weight | Why It Works |

|---|---|---|---|

Yield-First Investor | Efficient 1BR with front-row view, simple fit-out | Ultra-large formats with high OPEX | Better rentability + tighter OPEX keeps yields closer to base case. |

Lifestyle/Second-Home | Signature stack, curated interiors, quiet floor plate | Micromanaging psf | You’re buying lived experience; resale will track brand + view quality. |

Hybrid (Use + Rent) | 1.5BR/large-1BR layouts, lockable owner storage | All-year STR dependence | Flex for school holidays or winters; rent shoulder seasons. |

Comparative Landscape (Zoomed Out, Calmly)

It helps to hold Jacob & Co Residences up against a few “magnet markets.” Not to declare winners—just to see where logic leads. I like simple, honest contrasts; a table keeps us grounded.

Al Marjan vs. Dubai Islands vs. Palm Jebel Ali (and a Dubai Core Baseline)

Dimension | Al Marjan Island (RAK) | Dubai Islands | Palm Jebel Ali | Dubai Core Baseline (Downtown/Marina) |

|---|---|---|---|---|

Core Draw | Casino-adjacent leisure ecosystem, growing branded stock, calmer pace | New masterplan w/ urban-beach vision, Dubai brand gravity | Trophy-scale villas + signature waterfront, big-luxury narrative | Established depth, transit, proven resale/liquidity |

Typical Buyer | Lifestyle + yield hybrids, second-home seekers | Early adopters betting on Dubai’s next shoreline | UHNWI/expats seeking trophy beachfront houses | Global mix; investors/end-users; deep rental markets |

Pricing (Indicative) | Lower entry than prime Dubai waterfronts; branded premiums exist | Mid to high (new-build Dubai); diverse bands emerging | Very high for prime plots and villas | Wide band; from mid to ultra-prime by tower/stack |

Yield Thesis | Tourism-led + Wynn halo; still maturing | Dubai demand depth but supply rollouts will matter | Capital preservation + prestige; yield secondary | Liquidity + rental depth; efficient 1BRs often shine |

Risk Flags | Supply bunching around 2027–2029; OPEX drift | Execution timelines, phasing of amenities | Ticket sizes; construction timelines | Competition is intense; premiums for iconic views |

Who Might Prefer It | Those who want beachfront narrative under Dubai prices | Buyers bullish on “new Dubai shoreline” story | Trophy/legacy buyers | Investors needing liquidity + track record |

Short version (very short): Al Marjan offers beachfront access and brand cachet at lower entry than Dubai’s headline shores, but you trade some of Dubai’s market depth for a developing ecosystem. For many, that’s a fair trade—if you’re patient and selective on stack/view.

Deeper Peer Matrix (Within Al Marjan)

Let’s put the immediate neighbors side-by-side in a bit more detail. These are indicative markers; your final decision should be based on the exact release you’re reviewing.

Project | Brand Position | Likely Buyer Fit | Layout Logic | Perceived Edge | Potential Friction |

|---|---|---|---|---|---|

Jacob & Co Residences | Haute luxury design, jewel-like interiors | End-users who value design curation; investors who bet on “brand rarity” | Compact to mid-size 1–2BRs (select 3BRs possible) | First-of-its-kind brand; interiors as a differentiator | Premiums must be justified in real finishes; service charge sensitivity |

JW Marriott Residences | Global hotel-residential flag, turnkey comfort | Investors seeking global brand and rental familiarity | Broad mix (1–3BR + larger formats) | Brand trust; hospitality playbook | Competition within same masterplan; homogeneity risk |

Costa Mare (Ellington) | Design-led beach living, lifestyle programs | Lifestyle-first buyers; aesthetically driven investors | Varied 1–3BR stacks; private beach | Ellington design pedigree; amenity curation | Ask bands vary widely; view dependency |

I find that when buyers walk the boardwalk and literally “feel” each façade, the preference gets obvious—sometimes in minutes. (It’s funny how quickly a lobby can decide a seven-figure choice.)

Sensitivity: psf, View, OPEX (Because Reality Moves)

A small shift in any variable changes the picture. Let’s model a simple psf sensitivity for a 1BR at 900 sq ft. Numbers are purely illustrative and meant to show direction.

psf (AED) | Price (AED) | Notes |

|---|---|---|

2,600 | 2,340,000 | Entry-level stacks, partial view, competitive release |

2,800 | 2,520,000 | Stronger view or better line, mid floor |

3,000 | 2,700,000 | Branded premium on favored stack |

3,200 | 2,880,000 | High floors + signature view axis |

3,400 | 3,060,000 | Top-stack scarcity; limited inventory |

Now OPEX sensitivity (annual), because service charges are the quiet lever:

Annual OPEX (AED) | NOI Impact (Base Case Revenue) | Yield on 2.7M |

|---|---|---|

42,000 | +7,000 vs our base | ≈ 6.48% |

49,000 | Baseline we used | ≈ 6.22% |

56,000 | −7,000 vs our base | ≈ 5.96% |

Small deltas matter. If you can secure a slightly better view without a big OPEX jump, that can be the smarter long-run choice.

Payment Plans: 70/30 vs 60/40 (Cash-Flow Calendars)

Some launches vary the structure. Here’s a side-by-side for a AED 2,600,000 ticket. Same 36-month construction horizon (illustrative).

A) 70/30

Month | % | AED | Running Total |

|---|---|---|---|

0 | 10 | 260,000 | 260,000 |

6 | 10 | 260,000 | 520,000 |

12 | 10 | 260,000 | 780,000 |

18 | 10 | 260,000 | 1,040,000 |

24 | 10 | 260,000 | 1,300,000 |

30 | 10 | 260,000 | 1,560,000 |

36 | 10 | 260,000 | 1,820,000 |

Handover | 30 | 780,000 | 2,600,000 |

Pros: Smaller handover shock if you’ve pre-saved the 30%; more installments can be easier to align with income.

Watch: Total paid before keys is higher (1.82M).

B) 60/40

Month | % | AED | Running Total |

|---|---|---|---|

0 | 10 | 260,000 | 260,000 |

9 | 10 | 260,000 | 520,000 |

18 | 10 | 260,000 | 780,000 |

27 | 10 | 260,000 | 1,040,000 |

36 | 20 | 520,000 | 1,560,000 |

Handover | 40 | 1,040,000 | 2,600,000 |

Pros: Lower cash-out during construction; higher liquidity until keys.

Watch: Bigger final cheque (40%); some buyers prefer to split that across finance and cash.

If your home currency isn’t AED, overlay an FX plan. Phased conversions (e.g., quarterly) can reduce timing risk versus one large lump-sum at handover.

Expanded FAQs

Q: What’s the real differentiator for Jacob & Co Residences?

A: The brand’s design language. If the finished product mirrors the gem-cut geometry and watchmaking precision the name implies, you’re buying something recognizably “Jacob & Co,” not generic beachfront.

Q: Are branded premiums worth it?

A: Sometimes absolutely… sometimes not. It depends on tangible elements—finish quality, lobby experience, private club feel, after-sales standards—not only a logo on the brochure.

Q: How should I think about yields here?

A: Underwrite 5–6% gross for Year 1–2, then re-rate after the Wynn opening settles and your operator optimizes occupancy. The upside exists; treat it as upside, not baseline.

Q: What unit sizes rent best?

A: Efficient 1BRs with compelling views are typically the rental workhorses. Large 2–3BRs can command premiums but face narrower tenant pools and higher OPEX.

Q: What about exit timing?

A: If your thesis includes the Wynn halo, consider holding through at least the first two high seasons post-opening. That’s when the narrative is the strongest for resale.

Q: Should I worry about supply?

A: Healthy caution helps. Track phased deliveries 2027–2029 and focus on scarcity factors (front-row stacks, corner lines, unobstructed axes). Scarce variables retain pricing power.

Where Jacob & Co Residences Actually Fit (My Calm Take)

If you remove the noise and just sit with it for a minute, Jacob & Co Residences on Al Marjan Island looks like a very specific kind of bet: design-led beachfront living with a recognizable brand signal, priced below Dubai’s most famous shores, yet close enough—in story and in flight time—to capture global attention once Wynn opens and the island reaches its next phase.

Will every unit make a landlord smile? Probably not. View corridors, stack scarcity, and OPEX control will separate “good” from “great.” But for end-users who care about the feel of a lobby, the quality of materials under hand, and the calm of waking to sea light—this is strongly compelling. For investors, it’s less about a guaranteed 9% and more about total return rooted in scarcity: front-row lines, brand differentiation, and timing around a major hospitality opening. If that sounds like your style of underwriting, then, yes, this one deserves a site visit.

Quick, honest takeaways

Best buyers: design-biased end-users; hybrid owners who’ll use the unit in peak seasons; investors who underwrite 5–6% and let upside be upside.

Key variable: view/stack scarcity. (It remains the quiet king.)

Timeline thinking: allow for a 2027–2029 maturation arc; judge again after two Wynn high seasons.

Actionable next step: shortlist 2–3 stacks, request draft SPA clauses for brand use and OPEX ranges, then walk the island in person.

Helpful Navigation

Al Marjan Island, Ras Al Khaimah: Buyer & Investor Guide

Al Marjan Island - Ras Al Khaimah (RAK)