Dubai Islands offers rare beachfront investment, blending luxury living, tourism, and growth potential in one of Dubai’s most ambitious coastal projects.

If you've been watching the Dubai real estate market lately, you've probably noticed a shift. The conversation isn't just about Downtown or Dubai Marina anymore. It's moving toward the water, specifically to the northern coastline. I remember looking at Palm Jumeirah years ago when it was just sand and ambitious blueprints. People who bought in then? Well, they're doing quite alright today. Dubai Islands feels a lot like that early Palm Jumeirah era, but perhaps with even better infrastructure planning from day one.

For investors looking ahead to 2026 and 2027, the window to get in at "ground floor" pricing is still open, though it's definitely closing faster than many anticipated. Let's take a deep dive into why Dubai Islands investment is dominating the portfolios of smart buyers right now.

The "Palm Jumeirah Effect" at a Fraction of the Cost

Let's talk numbers, because that's what really matters. History has a funny way of repeating itself in Dubai real estate. Investors who secured property on Palm Jumeirah in the early 2000s saw exponential returns as the master plan came to life. Dubai Islands offers a very similar ecosystem—pristine beaches, world-class marinas, and luxury resorts—but at a significantly lower entry point.

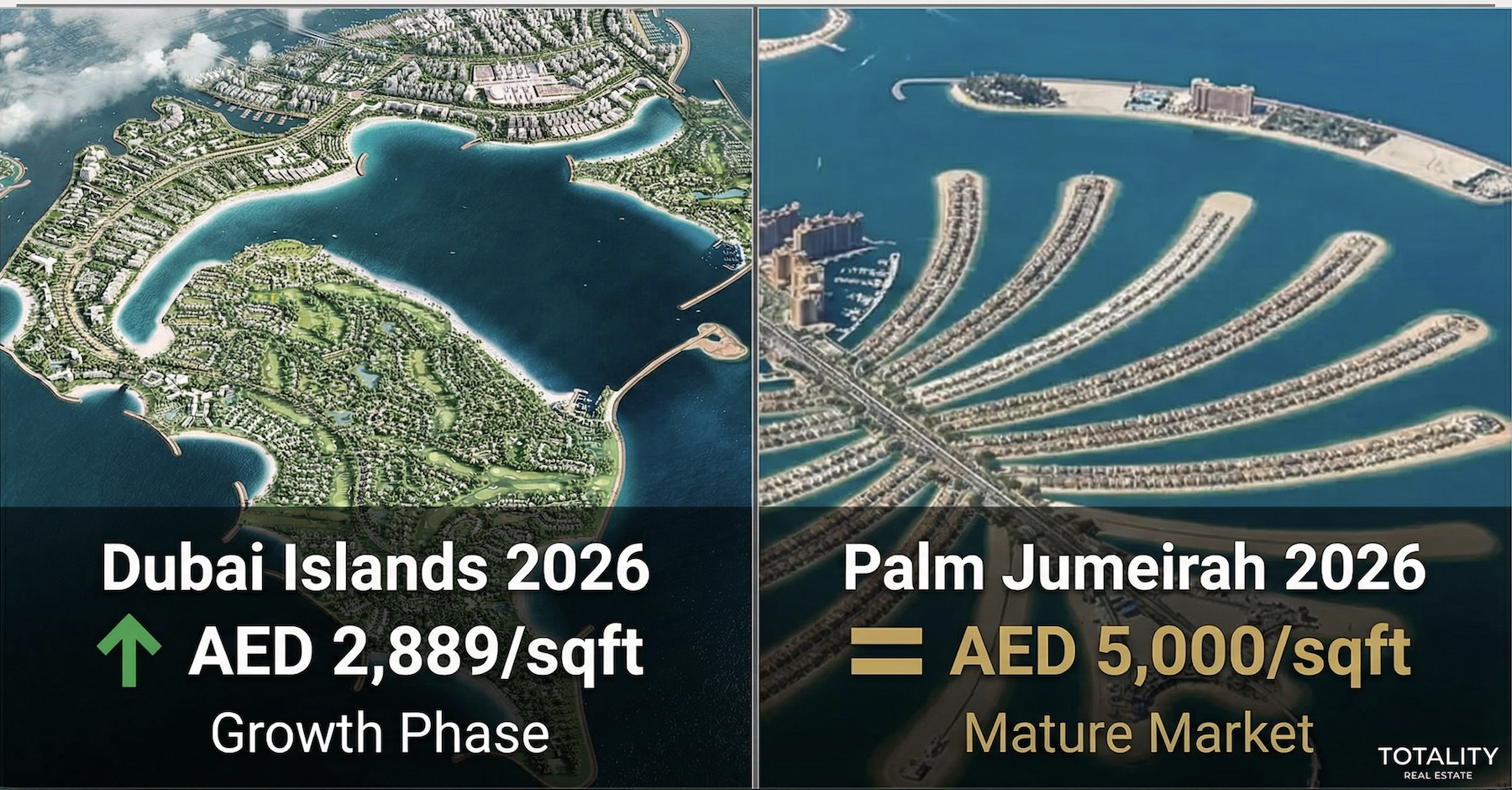

While Palm Jumeirah apartments are currently averaging well over AED 4,500 per square foot, premium off-plan units on Dubai Islands are trading between AED 1,850 and AED 2,889 per square foot, depending on the exact location and developer. In fact, recent transaction data from March 2026 shows sales hitting that AED 2,889 mark, which is a clear indicator that prices are already on the move.

This massive price gap suggests a very high ceiling for capital appreciation. As the infrastructure matures and more flagship resorts open their doors, property values are projected to surge, naturally narrowing the gap with established luxury waterfront communities. It's not a matter of if the prices will catch up, but when.

Key Investment Highlights for 2026

When you strip away the marketing brochures, what are you actually buying into? The fundamentals of Dubai Islands are incredibly strong.

Prime Location and Connectivity

This isn't some isolated project out in the desert. Dubai Islands is a massive 17-square-kilometer extension of Dubai's coastline, situated just off Deira. The connectivity is genuinely impressive. The new Infinity Bridge connects the islands directly to the mainland, slashing travel times. You are looking at just an 18-minute drive to Dubai International Airport and about 25 minutes to Downtown Dubai. Plus, a new bridge linking directly to Port Rashid is in the works, which will only strengthen the bond between this coastal retreat and the city's vibrant core.

The Master Developer: Nakheel

Confidence in the developer is everything when buying off-plan. Nakheel is the master developer behind this project. They are the same visionary minds that built Palm Jumeirah. They know how to build islands, they know how to manage marine infrastructure, and they have the full backing of the government's Dubai 2040 Urban Master Plan.

Infrastructure Built for the Future

The development isn't just residential towers; it's a fully integrated city. The master plan includes 9 marinas, executive golf courses, 37 planned resorts, and 20 kilometers of Blue Flag-certified beaches. Interestingly, 45% of the land is dedicated to parks and green spaces. This is a major shift in how waterfront communities are being designed today, prioritizing livability and family-friendly environments over sheer density.

Five Islands, Five Unique Lifestyles

Unlike standalone towers in crowded districts, Dubai Islands is divided into five distinct zones. This is brilliant from an investment perspective because it ensures diverse tenant demand—from short-term tourists to long-term expat families and ultra-high-net-worth individuals (UHNWIs).

Island A (Central Island): The Vibrant Hub

This is the commercial and entertainment core. If you want high foot traffic and vibrant energy, this is it. It features a massive mall, a heritage-style marina promenade with a traditional souk, and higher-density residential options. It's perfect for investors targeting young professionals or short-term holiday lets.

Island B (Shore Island): Exclusive Resort Living

Known for its exclusive environment, Island B is the "Resort & Community" heart. This is where you'll find flagship luxury projects like Rixos Dubai Islands and Bay Grove Residences. It offers resort-style living with direct, private beach access. Properties here are highly sought after by end-users and investors looking for premium rental yields.

Island D (Golf & Sports): The Wellness Destination

A dedicated wellness and recreation zone featuring executive golf courses with stunning sea views and sports academies. This island is designed for residents and visitors who want a healthy, active lifestyle without leaving the archipelago.

Island E (The Elite Estates): Ultra-Private Luxury

An ultra-private enclave for low-density luxury villas and VIP marina estates that will eventually rival Palm Jumeirah's "Billionaire's Row." Signature plots are available here for those looking to build custom mega-mansions.

Why Invest Now? The 2026 Advantage

Timing is everything in real estate. We are currently in what I like to call the "sweet spot" of the investment cycle for Dubai Islands. The infrastructure is visible—bridges are built, roads are paved, and the first hotels (like Hotel RIU and Centara Mirage) are already operational and welcoming guests. Yet, the prices have not yet peaked.

Off-Plan Opportunities and "Neo-Luxury"

The off-plan market here is thriving. Projects like HADO by Beyond in Dubai Islands are highlighting a new "neo-luxury" focus in the area—high-end finishes, smart home tech, and resort amenities, but without the ultra-premium price tag of established neighborhoods. Other notable launches, such as LuzOra by DIA Developments and Flora Bay Residences by Octa, are offering attractive entry points (starting around AED 1.7M for a 1-bedroom) with favorable payment plans extending into 2027.

Freehold Ownership and Golden Visas

A crucial point for international buyers: Dubai Islands is a designated Freehold Zone. This means investors of any nationality can own property here outright. Furthermore, with most starting prices for premium units sitting above the AED 2 million threshold, practically every property purchase qualifies the buyer for the 10-Year UAE Golden Visa. This grants long-term residency for you, your family, and even domestic staff, adding a massive layer of lifestyle security to your financial investment.

ROI and Rental Yield Projections

Let's get down to the brass tacks of why you're really reading this: the returns. The "early investor" advantage isn't just about waiting five years for capital gains; it's about generating strong, immediate yield as soon as the keys are handed over.

With 20 kilometers of new beachfront and over 30 planned hotels, the short-term rental demand (think Holiday Homes and Airbnb) is expected to boom. Tourists want to be near the water, and they want resort-style amenities. Conservative estimates place NET rental yields at 7% to 9% for well-managed waterfront units on Dubai Islands.

To put that in perspective, the citywide average for apartment gross yields hovers around 7.3%. When you benchmark this globally, it's even more impressive. Many coastal cities in Europe or North America struggle to deliver 3% to 5% gross. The supply of true beachfront land in Dubai is finite. As downtown areas become increasingly saturated and expensive, tenant demand is naturally shifting towards coastal communities that offer a "vacation lifestyle" at a more accessible price point.

The Data: Price Appreciation in Action

If you need proof that the market is already moving, look at the recent data. According to industry reports from early 2026, Dubai Islands saw a remarkable 10.7% price appreciation over the course of 2025 alone. This outpaces many of the mature, established zones in the city.

We are entering an infrastructure-led growth phase in Dubai. Smart investors are eyeing areas where major government spending is happening—specifically Dubai Islands in the north and Dubai South near the new airport. The scarcity of "brand new" ready stock on the water is driving this appreciation, and those buying off-plan today are locking in tomorrow's equity.

Dubai Islands Rental Yield vs. Global Waterfront Markets

| Location | Average Gross Rental Yield | Freehold for Foreigners | Tax on Rental Income |

| Dubai Islands (UAE) | 7% – 9% | Yes | 0% |

| Palm Jumeirah (UAE) | 4.5% – 5.5% | Yes | 0% |

| London (UK) | 3% – 4% | Yes | Up to 45% |

| Miami (USA) | 4% – 6% | Yes | Up to 37% |

| Côte d'Azur (France) | 2.5% – 3.5% | Yes | Up to 45% |

| Singapore | 3% – 4% | Yes (with ABSD) | Up to 22% |

Dubai Islands vs. Palm Jumeirah: A Direct Comparison

I get asked this question almost daily: "Should I buy a smaller unit on Palm Jumeirah or a larger, newer unit on Dubai Islands?" It's a fair question. Both are Nakheel master-developments, and both offer that iconic Dubai island lifestyle. But they serve very different investment strategies in 2026.

| Metric | Dubai Islands (2026) | Palm Jumeirah (2026) |

| Average Price (per sq. ft) | AED 1,850 – AED 2,889 | AED 4,500+ |

| Project Phase | Early / High Growth | Mature / Stabilized |

| Capital Appreciation Potential | Very High (70-130% catch-up potential) | Moderate (Steady, single-digit growth) |

| Rental Yields (Expected NET) | 7% – 9% | 4.5% – 5.5% |

| Property Age | Brand New / Off-Plan | Mostly 10-15 years old |

| Freehold Access | Yes (All Nationalities) | Yes (All Nationalities) |

| Golden Visa Eligible | Yes (AED 2M+) | Yes (AED 2M+) |

| Beachfront Length | 20 km (new, Blue Flag) | ~5 km (established) |

| Number of Marinas | 9 (planned) | 2 (existing) |

| Hotels & Resorts | 37 planned / 3 operational | 15+ operational |

The key difference here is optionality and growth phase. Palm Jumeirah gives you immediate choice across many price points and unit types, but you are paying a massive premium for the established brand name. The capital growth there has largely plateaued.

Dubai Islands, on the other hand, is in its aggressive growth phase. To match Palm Jumeirah's current pricing, Dubai Islands would need a 130% price increase. Even if it only catches up halfway, the ROI for early investors will be staggering. If your goal is wealth preservation, buy the Palm. If your goal is wealth creation, buy Dubai Islands.

What Are the Risks? (Because No Investment is Perfect)

I'd be doing you a disservice if I didn't mention the risks. Real estate isn't magic; it requires patience and strategy.

Development Timeline Risk. This is a massive, multi-phase project. While the core infrastructure is there, full-scale development will take another 5 to 8 years. If you buy an off-plan unit completing in 2027, you might be living (or renting) near active construction sites for a while. This can temporarily suppress rental rates in the very early years.

Macro Supply Pressure. Dubai anticipates a significant number of new units hitting the market by 2027. If population growth doesn't keep pace with this supply, we could see a softening in rental yields citywide.

Mitigation Strategy. However, waterfront properties have historically been highly resilient to supply shocks. There is always a premium on sea views. To mitigate these risks, my advice is simple: stick to reputable developers, ensure your funds are going into DLD-regulated escrow accounts, and plan to hold the asset for at least 3 to 5 years to ride out any short-term market fluctuations.

Investment Snapshot: What Can You Actually Buy?

So, what does the inventory actually look like right now? The options are surprisingly diverse, catering to different budgets and strategies.

| Property Type | Starting Price | Best For | Typical Payment Plan |

| 1-Bedroom Apartments | ~AED 1.7M – 1.9M | Yield-focused investors | 60/40 or 70/30 |

| 2 & 3-Bedroom Residences | ~AED 2.9M+ | Families, luxury holiday market | 60/40 post-handover |

| Townhouses & Villas | ~AED 4.0M – 11.4M | End-users, long-term value | 50/50 or 60/40 |

| Signature Plots (Island E) | Upon request | Ultra-wealthy, custom builds | Negotiable |

Projects like LuzOra and ARYA Residences are perfect for the yield-focused 1-bedroom strategy. They are relatively easy to rent out on the short-term market and require lower capital outlay. Meanwhile, a 4-bedroom villa on the water for under AED 12M is practically unheard of in other parts of Dubai today—making the townhouse and villa segment a genuine value play for families.

Frequently Asked Questions

Is Dubai Islands a good investment?

Yes. Dubai Islands is widely considered one of the most compelling investment opportunities in Dubai for 2026 and 2027. With off-plan prices averaging AED 1,850 to AED 2,889 per square foot—roughly 50% below Palm Jumeirah—and projected net rental yields of 7% to 9%, the area offers both capital appreciation potential and strong income generation. The 10.7% price appreciation recorded in 2025 is early evidence that the market is already moving.

Can a US citizen (or any foreigner) invest in Dubai Islands?

Absolutely. Dubai Islands is a designated Freehold Zone, meaning citizens of any nationality can purchase and own property outright with 100% ownership. There are no restrictions on foreign buyers, and the process is straightforward through the Dubai Land Department (DLD).

Do I qualify for a Golden Visa if I buy property in Dubai Islands?

Yes. Purchasing a property valued at AED 2 million or more qualifies you for the 10-Year UAE Golden Visa. Since most premium units on Dubai Islands exceed this threshold, practically every purchase here comes with Golden Visa eligibility for you and your family.

What is the difference between Dubai Islands and Deira Islands?

They are the same project. "Deira Islands" was the original name used during the early reclamation phase. In 2023, Nakheel officially rebranded the development as "Dubai Islands" to reflect its broader vision as a citywide destination rather than a Deira-specific project.

When will Dubai Islands be fully completed?

The development is being delivered in phases. The first wave of residential and hospitality projects (including Rixos Dubai Islands, Hotel RIU, and Centara Mirage) are already operational or nearing completion. Full build-out of all five islands is expected to continue through 2030 and beyond, with the most significant construction activity happening between 2026 and 2028.

What are the best areas to invest in Dubai in 2026?

While several areas offer strong returns, Dubai Islands and Dubai South are consistently cited by analysts as the top two investment zones for 2026 due to their infrastructure-led growth trajectories. For a broader look at the market, read our Dubai Real Estate Market Report.

The Final Verdict on Dubai Islands

Dubai Islands isn't just another coastal real estate project—it's a rare chance to invest early in the emirate's next urban icon. It offers secure legal ownership, attractive entry pricing, high-yield potential, and strategic tourism exposure.

As Dubai's city core reaches maturity and prices there push out the average investor, the next growth wave is already building offshore. The infrastructure is real, the developers are breaking ground, and the early data shows prices are already climbing. The time to ride that wave—before it breaks and prices align with the rest of the luxury market—is right now.

To explore specific off-plan properties and secure early allocations in this area, visit our Dubai Islands area guide, read our comparative analysis of Al Marjan Island vs. Dubai Islands, or check out our latest top investment areas for 2025.